Living on a fixed income does not mean you must lower your quality of life to make ends meet. You can reclaim hundreds of dollars each month by eliminating hidden wealth-drainers and making strategic adjustments to your spending habits. Rising healthcare costs, inflation, and property taxes consistently threaten your savings, but proactive financial management puts you back in control. We outlined nine actionable strategies to cut monthly expenses seniors successfully use every single day. By applying these methods, you protect your nest egg and stretch every dollar further. When you actively budget retirement, your golden years remain comfortable, secure, and stress-free.

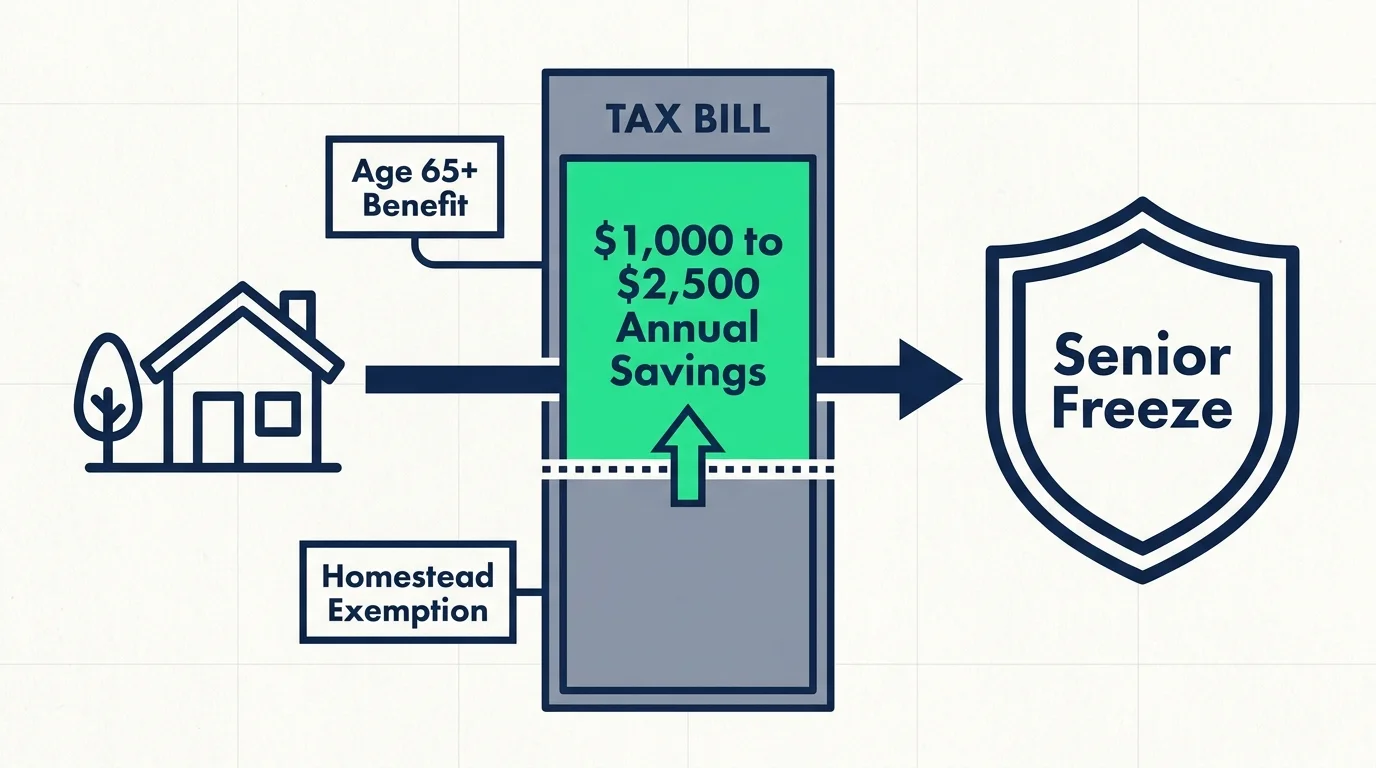

Financial Habit #1: Slashing Property Taxes Through Senior Exemptions

Property taxes represent one of the largest ongoing expenses for retirees who own their homes outright. Local municipalities consistently raise property assessments, which drives your tax bill higher every single year. You combat this automatic wealth drain by applying for age-based property tax exemptions. Many states and counties offer a senior freeze or a homestead exemption specifically designed to protect older residents from being priced out of their neighborhoods.

Start by visiting your local county assessor office online or in person. You must typically prove your age and demonstrate that your income falls below a certain threshold. Once approved, this exemption locks your property taxable value in place or slashes the assessed value by a set percentage. For example, a senior living in a high-tax state could shave $1,000 to $2,500 off their annual tax bill just by filing a single form. You keep that money directly in your bank account instead of sending it to the county. Make this a priority as soon as you turn 65; these exemptions are rarely applied automatically.

Financial Habit #2: Conducting a Ruthless Subscription Audit

Modern spending habits rely heavily on recurring charges, which silently siphon money from your checking account month after month. Retirees often accumulate multiple streaming services, premium cable packages, magazine deliveries, and software subscriptions that they rarely use. Conducting a rigorous subscription audit immediately frees up cash flow without impacting your daily routine.

Print out your last three months of credit card and bank statements. Highlight every recurring charge. You will likely uncover gym memberships you stopped using, duplicate music services, or free trials that converted into paid subscriptions long ago. If you pay $150 a month for a premium cable bundle but only watch local news and classic movies, cut the cord. Switch to an over-the-air antenna for local channels and pick one affordable streaming service for $15 a month. This single adjustment saves you $1,620 over the course of a year. Redirect those recovered funds straight into your emergency savings or use them to cover rising grocery costs. By actively policing your recurring expenses, you stop paying for services that provide zero value to your life.

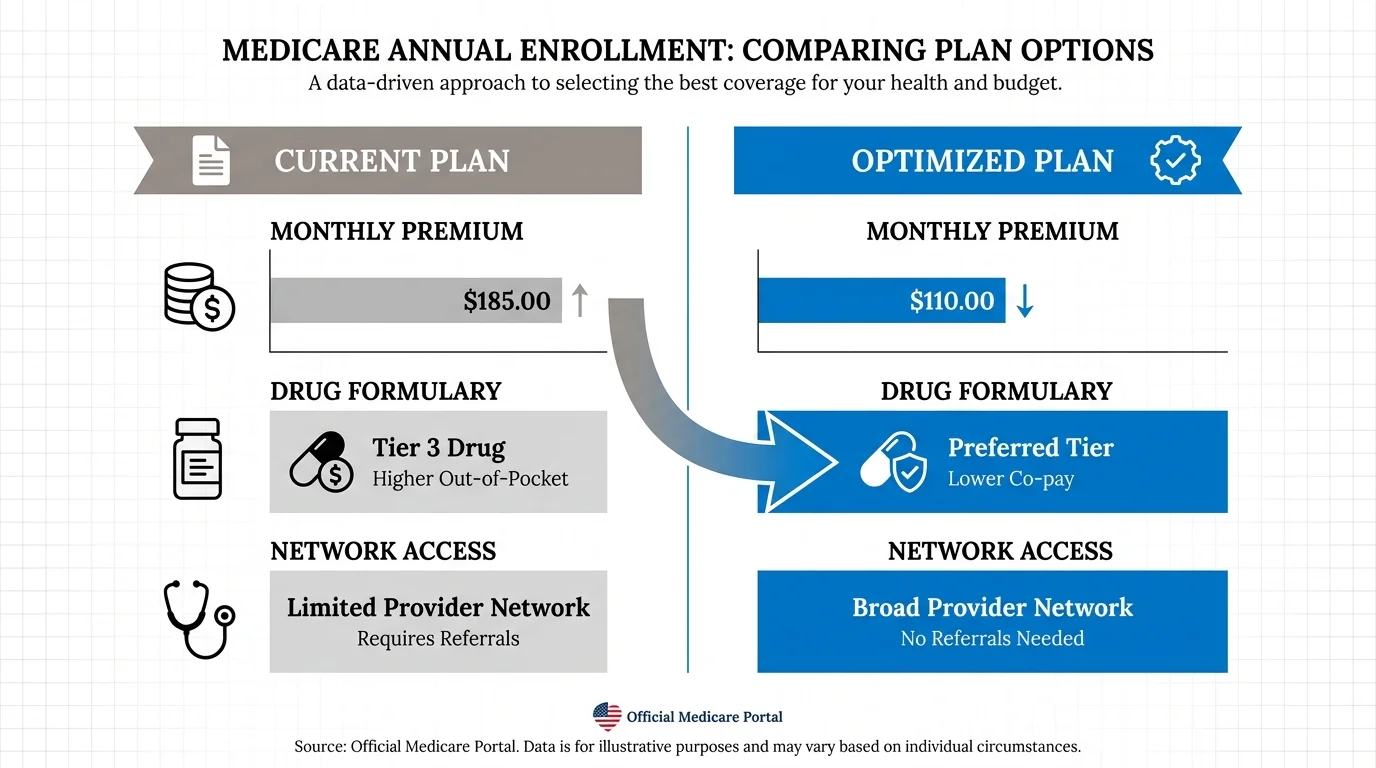

Financial Habit #3: Optimizing Medicare Plans Annually

Healthcare expenses devour fixed incomes faster than almost any other budget category. Far too many seniors stick with the exact same Medicare Advantage or Part D prescription drug plan year after year simply out of convenience. Insurance providers frequently alter their drug formularies, change network providers, and increase premium costs annually. Complacency with your medical coverage directly translates to wasted money.

Take full advantage of the Medicare Annual Enrollment Period every fall to aggressively compare plans. Your current provider might drop your essential blood pressure medication from their preferred tier, doubling your out-of-pocket cost at the pharmacy counter. By logging into the official government Medicare portal, you can input your specific prescriptions and preferred doctors to see which plan offers the lowest total out-of-pocket cost for the upcoming year. Switching to a better-optimized plan often saves seniors anywhere from $500 to $1,500 annually. Do not let loyalty to an insurance company cost you your hard-earned retirement funds. Reviewing your coverage takes just an hour of your time, but it guarantees you only pay for the exact medical coverage you actually need.

Financial Habit #4: Taking Advantage of Age-Based Discounts

Leaving money on the table is a cardinal sin of frugal living. When looking to reduce spending 60+ individuals often overlook the power of age-based discounts. Thousands of retailers, restaurants, and service providers offer exclusive pricing for seniors, but you must actively ask for these reductions—cashiers rarely apply them automatically. Leveraging these discounts requires absolutely no lifestyle changes but dramatically lowers your monthly spending footprint.

Start at the grocery store. Many regional supermarket chains host designated senior discount days, offering 5% to 10% off your entire cart. If you spend $400 a month on groceries, shopping exclusively on discount days saves you nearly $500 a year. Apply this same aggressive mindset to your auto insurance, cellular phone provider, and travel plans. Organizations like AARP provide access to discounted hotel rates, cheaper rental cars, and reduced dining tabs at participating national chains. Call your mobile phone provider and ask to be switched to their specific senior plan; major carriers often offer unlimited talk and text plans for individuals over 55 at a fraction of the standard rate. Asking a simple question at the register instantly shrinks your bills.

Financial Habit #5: Downsizing Your Transportation Costs

Maintaining multiple vehicles drains a massive portion of a retirement budget. Between insurance premiums, routine maintenance, expensive repairs, registration fees, and gasoline, owning a car costs the average American thousands of dollars annually. If you are no longer commuting to a full-time job every day, a two-car household rarely justifies the staggering expense.

Consider selling your secondary vehicle. The immediate cash influx from the sale pads your savings account, while the elimination of ongoing ownership costs drastically improves your monthly cash flow. If you and your spouse only drive to the grocery store, medical appointments, and social gatherings, coordinating schedules to share a single car presents a minor logistical hurdle with a massive financial payoff. For single seniors, selling your only car and relying on a combination of community transit, rideshare apps, and grocery delivery services often proves cheaper than outright vehicle ownership. Run the numbers on your specific transportation costs. Cutting a $1,200 annual insurance policy and avoiding a $600 set of new tires provides immense relief to a tight fixed income without restricting your mobility.

Financial Habit #6: Implementing Preventive Home Maintenance

Deferred maintenance destroys retirement budgets through catastrophic emergency repairs. Ignoring small issues around your house inevitably leads to massive bills that require you to tap into your principal investment accounts or take on high-interest credit card debt. Frugal seniors understand that spending a little money today on upkeep saves thousands of dollars tomorrow.

Create a strict seasonal maintenance schedule for your home. Pay a licensed professional $100 to inspect and tune up your HVAC system before the peak summer heat or winter freeze. This small investment extends the life of your unit and prevents a sudden $6,000 replacement bill. Clean your gutters twice a year to prevent water damage to your foundation, which costs tens of thousands of dollars to fix. Check the caulking around your windows and doors to seal drafts, simultaneously protecting your wood frames from rot and lowering your monthly heating and cooling bills. Replacing a fifty-cent washer in a dripping faucet immediately stops water waste. Taking proactive care of your property guarantees your home remains a secure asset rather than an unpredictable financial liability.

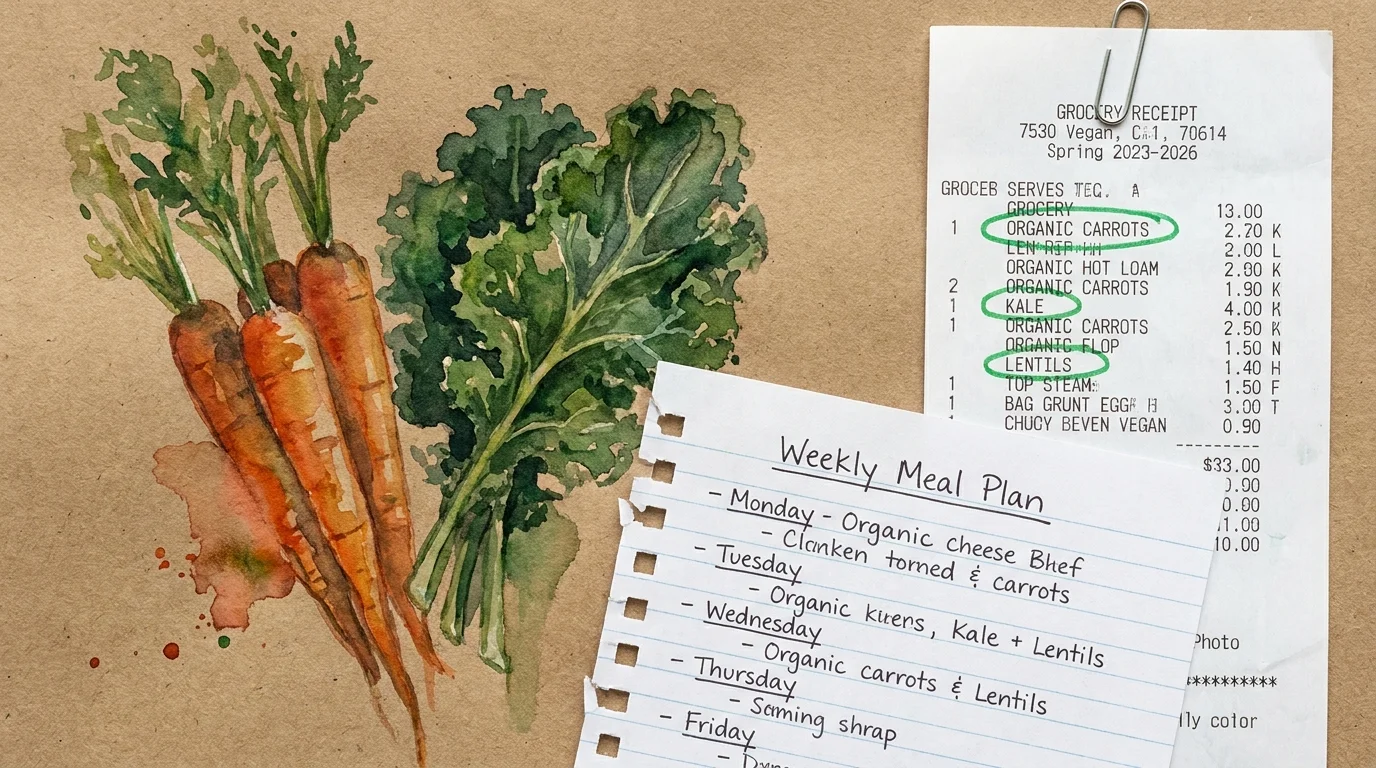

Financial Habit #7: Rethinking Grocery Shopping and Meal Planning

Food inflation forces many retirees to rethink how they fill their pantries. Wandering through the grocery store without a strategy guarantees impulse purchases and blown budgets. Applying these frugal senior tips slashes your food expenses by enforcing rigid meal planning habits and shifting your purchasing behaviors toward high-value ingredients.

Start by building your weekly meal plan strictly around the front-page deals in your local supermarket circular. If chicken thighs and seasonal root vegetables are on sale, those ingredients form the foundation of your dinners. Stop paying a premium for convenience; pre-cut vegetables and marinated meats carry ridiculous markups. Buy whole foods and spend ten extra minutes doing the prep work yourself. Additionally, shift your focus away from expensive name brands. Store-brand staples like rice, beans, canned tomatoes, and spices offer the exact same nutritional profile and taste quality for 30% to 50% less money. Investing in a small chest freezer allows you to buy meat in bulk when prices hit rock bottom. Controlling your kitchen habits easily shaves $100 or more off your grocery bill every single month without compromising your diet.

Financial Habit #8: Utilizing Free Community and Library Resources

Retirement provides you with an abundance of free time, but filling that time does not need to drain your bank account. Many seniors fall into the trap of spending heavily on expensive hobbies, new books, and premium entertainment. You can easily cut these discretionary expenses to zero by fully utilizing local community resources.

Your local public library functions as the ultimate wealth-building tool. Beyond free physical books, modern libraries provide digital access to audiobooks, premium magazines, streaming movies, and online courses directly to your tablet or smartphone. If you currently spend $30 a month buying new hardcovers or maintaining an audiobook subscription, a free library card keeps $360 a year in your wallet. Furthermore, local community centers and parks departments frequently offer free or heavily subsidized activities tailored specifically for residents over sixty. You can find yoga classes, computer literacy workshops, and social clubs that cost absolutely nothing. Cancel your expensive commercial gym membership and utilize these neighborhood alternatives. Staying active and entertained on a fixed income requires resourcefulness, not a thick wallet.

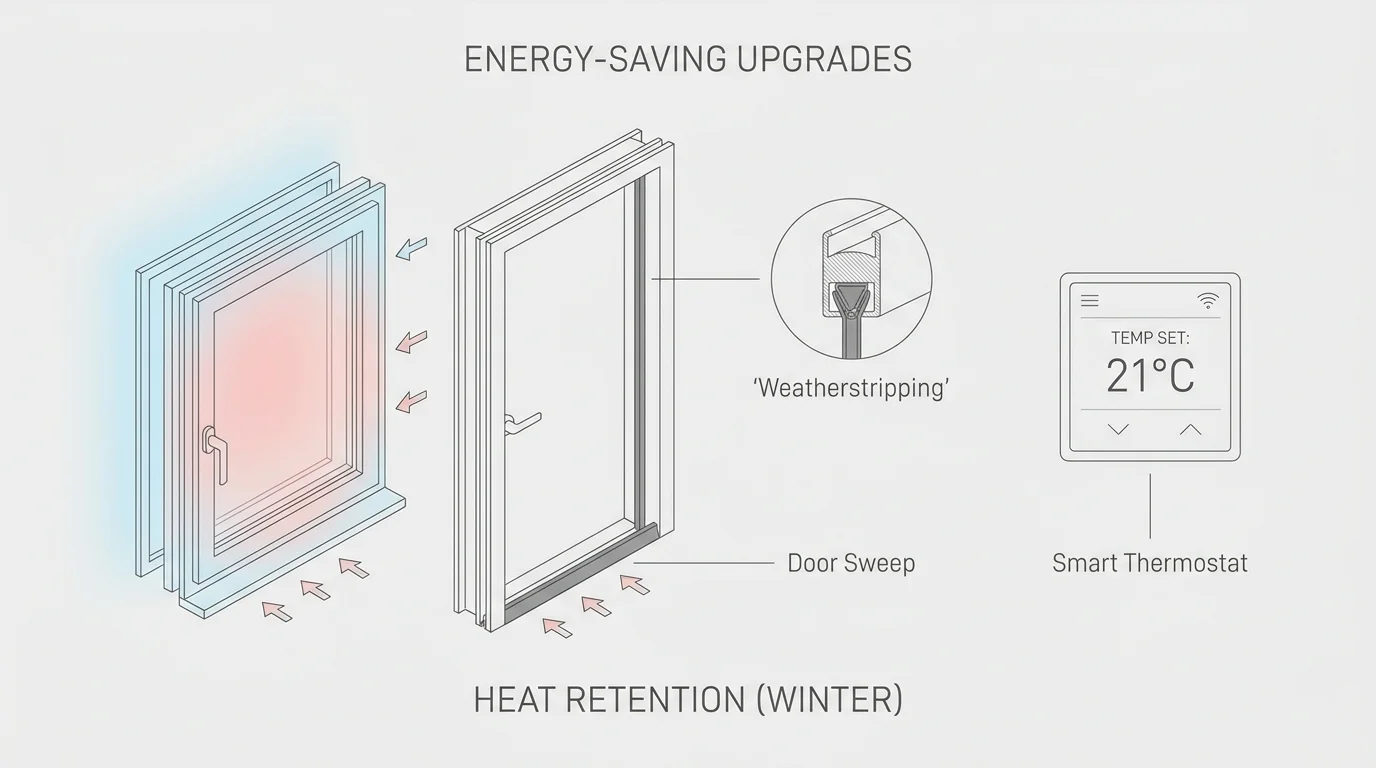

Financial Habit #9: Reducing Energy Consumption With Home Efficiency Upgrades

Utility bills fluctuate wildly with the seasons, making them incredibly difficult to budget for on a fixed income. Seniors who take control of their energy consumption immediately stabilize their monthly cash flow. You do not need to install a massive array of expensive solar panels to see a dramatic reduction in your electricity and gas costs.

Start by requesting a free home energy audit from your local utility provider. Many power companies send technicians to your house at no cost to identify exact areas where you waste energy. They often provide free LED lightbulbs, low-flow showerheads, and weather-stripping just for participating. Replace your old thermostat with a programmable model. Setting the temperature to automatically adjust while you sleep or leave the house cuts your heating and cooling costs by up to 10% annually. Lower the temperature on your water heater to 120 degrees to save on continuous heating costs without sacrificing a hot shower. Unplug parasitic appliances like coffee makers and spare televisions when not in use. These minor behavioral shifts compound into significant monthly savings.

The Big Picture: How This Affects Your Financial Future

Trimming excess fat from your monthly budget is not about living a life of deprivation. It is a proactive strategy to defend your financial independence and ensure your savings last as long as you do. When you live on a fixed income, every dollar you recover from a wasteful subscription, a missed discount, or an inefficient utility bill acts as a direct injection of cash into your future security. If you want to save without sacrifice, you must spend your money with intention rather than habit.

By implementing these nine strategies, you easily free up hundreds of dollars each month. You can deploy this newly available capital to build a robust emergency fund, aggressively pay down any remaining debt, or invest in experiences that truly bring you joy. Mastering your retirement budget removes the constant anxiety of living paycheck to paycheck on Social Security. You worked hard for decades to build your nest egg. Diligent expense management guarantees you remain in total control of your financial destiny, allowing you to enjoy a comfortable, dignified, and stress-free retirement.

Frequently Asked Questions

How do I negotiate my monthly bills if I live on a fixed income?

Call your service providers directly and ask to speak with the retention department. State clearly that you live on a fixed income and need to reduce your expenses. Ask if they offer senior discounts, loyalty promotions, or stripped-down service tiers. Providers for internet, cellular service, and cable would rather lower your bill than lose you to a competitor.

Does cutting expenses mean I have to stop traveling or enjoying hobbies?

Absolutely not. Frugality prioritizes your spending toward the things you love by ruthlessly cutting costs on the things you do not care about. By saving money on property taxes, utilities, and groceries, you generate the exact funds needed to finance your travel plans and hobbies without pulling extra money from your retirement portfolio.

What is the fastest way to reduce my spending without feeling deprived?

The fastest strategy is eliminating invisible expenses. Cancel unused subscriptions, call your auto insurance broker to shop for lower rates, and switch to a cheaper mobile phone plan. Because these changes do not alter your daily routine or consumption habits, you instantly improve your cash flow without feeling any sense of deprivation.

How often should I review my retirement budget?

You should conduct a comprehensive budget review every six months. Inflation rates, utility costs, and insurance premiums constantly fluctuate. A biannual review ensures you catch creeping expenses early. Additionally, review your healthcare coverage once a year during the open enrollment period to guarantee your medical costs remain optimized.

For official information on consumer finance and debt, consult the CFPB. Tax information is available from the IRS. For investment basics, refer to the U.S. SEC.

Disclaimer: This article provides informational content and personal opinions, not professional financial advice. Consult a certified financial advisor for guidance tailored to your specific situation.

Leave a Reply