Introduction: A No-Nonsense Guide to Cutting Costs in Retirement

Managing money on a fixed income requires strategy, discipline, and a willingness to adapt. In 2026, the economic landscape remains challenging. Rising utility rates, climbing property taxes, and the ever-increasing cost of healthcare mean your retirement dollars must stretch further than ever before. If you rely primarily on Social Security or a fixed pension, you already know that passive budgeting no longer works. You need active, aggressive methods to retain your wealth and protect your standard of living.

The good news is that thousands of older Americans are taking back control of their finances. They are finding innovative ways to save money seniors can implement immediately without sacrificing their quality of life. Achieving financial stability in your later years does not mean sitting in the dark and eating rice and beans. It means identifying inefficiencies in your spending and eliminating them ruthlessly.

This guide breaks down 15 proven strategies designed specifically for retirees and those approaching retirement. From renegotiating rigid monthly bills to rethinking transportation and housing, these steps will show you how to plug the leaks in your financial ship. Implement these tactics to build a reliable buffer against inflation and secure your financial peace of mind.

Financial Habit #1: Renegotiating and Slashing Monthly Bills

Many people set up their internet, cellular, and utility services and never look at them again. Providers rely on this complacency to slowly inch your rates higher year after year. A bill that started at $60 a month can quietly creep up to $110 over three years. You must treat these monthly obligations as open negotiations.

Call your service providers annually. Inform them that your fixed income requires you to reduce expenses, and ask for their retention department. Retention representatives possess the authority to apply loyalty credits or move you to promotional tiers unavailable to the general public. If they refuse to lower your rate, be prepared to switch to a competitor. Securing a $40 monthly reduction on your internet and a $30 reduction on your cellular plan puts $840 back into your pocket every year.

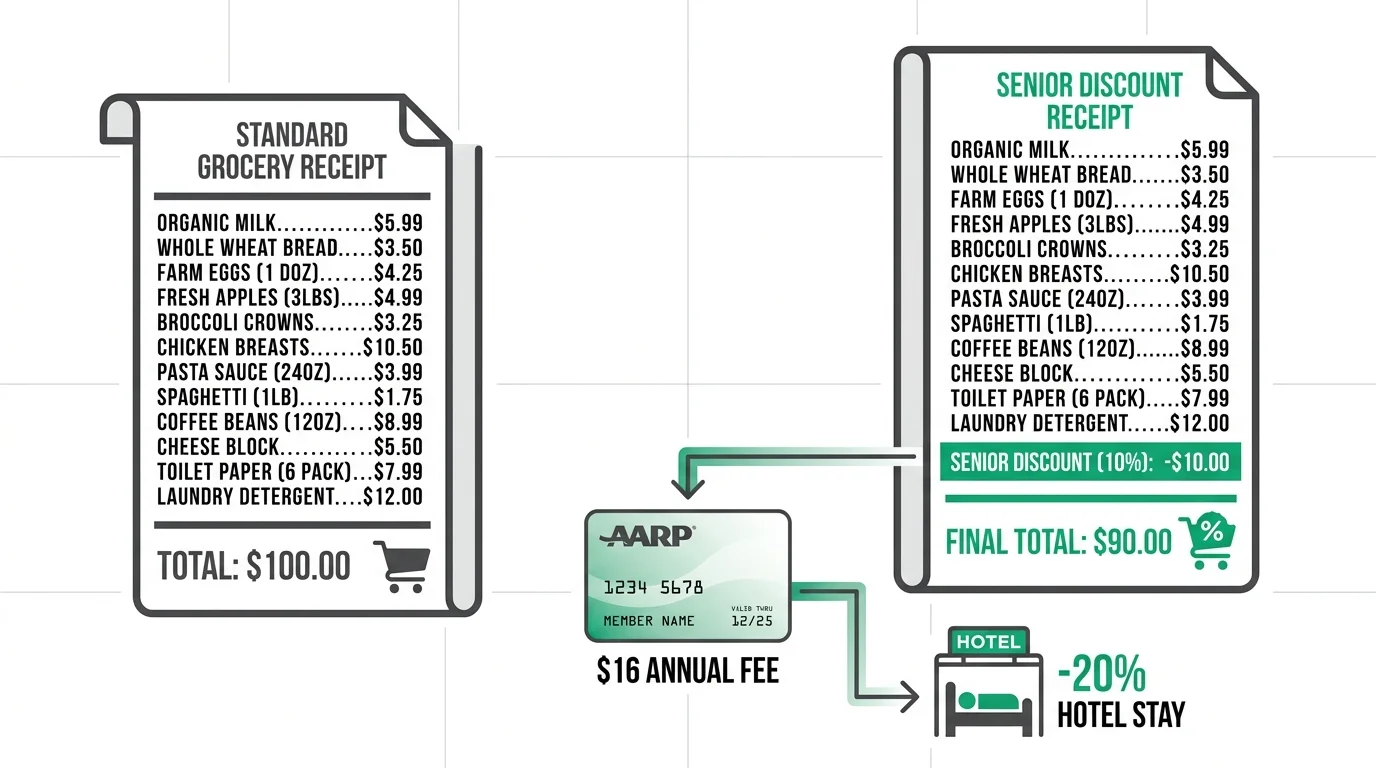

Financial Habit #2: Maximizing Age-Based Memberships and Discounts

Leaving age-based discounts on the table is the same as throwing cash in the trash. Grocery stores, auto repair shops, hotels, and retail outlets routinely offer specialized pricing for older customers; however, you almost always have to ask for it. Cashiers rarely apply these reductions automatically.

Familiarize yourself with the discount days at your local supermarkets. Planning your major grocery trips for a Tuesday or Wednesday to secure a 10% senior discount yields massive annual returns. Furthermore, leverage memberships like AARP for aggressive reductions on cellular plans, dining out, and travel accommodations. A $16 annual membership fee pays for itself after just one discounted hotel stay or an optimized phone bill. Demand the discounts you have earned through decades of participating in the economy.

Financial Habit #3: Implementing the Single-Car Strategy

Maintaining two vehicles in a retired household drains your capital with astonishing speed. According to automotive industry data, the true cost of owning a car—factoring in depreciation, insurance, registration, maintenance, and fuel—often exceeds $9,000 annually per vehicle. If you and your spouse no longer commute to separate jobs, a second car is a luxury masquerading as a necessity.

Sell the second vehicle and bank the proceeds. You immediately eliminate an entire column of recurring expenses from your budget. For the rare occasions when you need separate transportation, utilize a ride-share service or public transit. Spending $200 a year on occasional taxi rides represents a profound savings compared to spending thousands maintaining a metal box that spends 95% of its life sitting idle in your driveway.

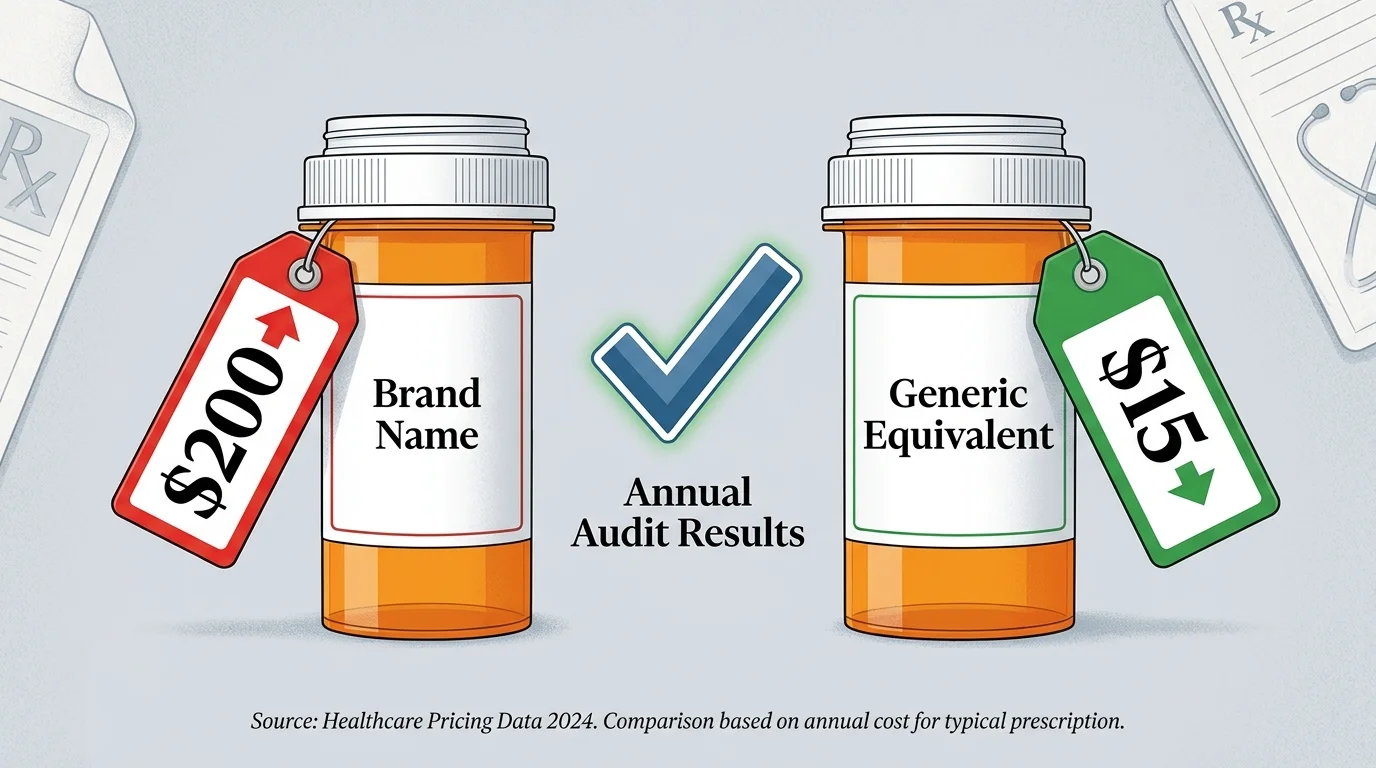

Financial Habit #4: Auditing Prescription Drug Plans Annually

Healthcare costs consistently rank as the highest threat to a secure retirement. Within that category, prescription medications drain accounts faster than almost any other expense. Relying on the exact same Medicare Part D plan year after year is a dangerous financial mistake. Insurance providers constantly alter their formularies, meaning a tier-one drug this year might become a tier-three drug next year.

During the open enrollment period, review your current medication list against the available plans in your area. Additionally, compare your insurance co-pays against cash-discount programs like GoodRx or cost-plus online pharmacies. Sometimes purchasing a generic medication outside of your insurance network is drastically cheaper than processing it through your provider. Taking two hours every November to research your options can literally save you thousands of dollars over the following twelve months.

Financial Habit #5: Moving Cash into High-Yield Savings Accounts

Traditional brick-and-mortar banks routinely pay abysmal interest rates on savings accounts—often hovering around 0.01%. Leaving a $50,000 emergency fund in an account with that rate generates a mere $5 over an entire year. Meanwhile, inflation actively erodes the purchasing power of that cash. This is the opposite of smart savings.

Move your liquid assets into an FDIC-insured high-yield savings account (HYSA) offered by reputable online banks. These institutions operate with lower overhead and pass the higher yields directly to you. An account offering a 4.5% annual percentage yield turns that same $50,000 into $2,250 in passive income per year. You take zero additional market risk and secure a meaningful return simply by changing where your money sits.

Financial Habit #6: Cutting the Cable Cord for Good

The traditional cable bundle is an obsolete and bloated expense. Paying $150 to $200 a month for hundreds of channels you never watch makes zero sense when you operate on a strict budget. Streaming technology has advanced entirely past the need for hardware rentals, broadcast fees, and regional sports surcharges.

Cancel your legacy cable provider and invest in a basic high-speed internet connection. Combine that connection with a digital antenna for local broadcast networks and one or two targeted streaming services. You can easily replicate your favorite news, sports, and entertainment programming for less than $40 a month. Trimming a $180 cable bill down to $40 saves you $1,680 every single year. That cash covers weeks of groceries or funds a comfortable emergency reserve.

Financial Habit #7: Securing Senior Property Tax Freezes

Rising property values might look good on a net-worth statement, but they trigger brutal increases in your annual property tax bills. For those practicing budgeting 60+ strategies, a sudden $2,000 jump in property taxes can completely derail an entire year of financial planning. Fortunately, many states and local municipalities offer property tax freezes or substantial exemptions specifically for older residents.

These exemptions are almost never automatic. You must contact your county tax assessor’s office, prove your age, verify your primary residence status, and sometimes demonstrate that your income falls below a certain threshold. Once approved, your home’s assessed value for tax purposes locks into place. Over a decade, this single administrative task protects tens of thousands of dollars from government collection.

Financial Habit #8: Stopping Financial Support for Adult Children

A major threat to long-term wealth preservation is ongoing financial support for capable adult children. Paying your 32-year-old daughter’s cell phone bill or funding your son’s car payments puts your own security in jeopardy. You cannot take out a loan to fund your retirement; your children have decades of earning potential to borrow and pay for their needs.

Set firm financial boundaries. Redirecting $400 a month back into your own accounts provides a critical buffer against future medical expenses or long-term care needs. Have an honest conversation about your fixed income constraints and phase out this financial support over a brief period. Protecting your nest egg is not selfish; it is a mandatory step to ensure you do not become a financial burden to your children later in life.

Financial Habit #9: Utilizing Strategic Cash-Back Credit Cards

If you possess the discipline to pay your balance in full every single month, using a debit card or cash is a missed opportunity. Credit card issuers offer highly lucrative cash-back rewards programs that effectively serve as a permanent discount on your daily living expenses.

Identify a no-annual-fee credit card that offers robust cash back on your highest spending categories, such as 5% back on groceries or 3% back on gasoline. Route all your regular spending through this card, and set up an automatic payment to clear the statement balance before any interest accrues. Earning $500 a year in cash back just for buying the food and fuel you were going to buy anyway requires no extra labor and bolsters your bottom line.

Financial Habit #10: Downsizing the Family Home

Maintaining a large family home long after the children have moved out forces you to pay for empty space. A four-bedroom house requires massive amounts of energy to heat and cool. It demands expensive roof repairs, constant lawn maintenance, and high insurance premiums. Your home should serve your current lifestyle, not act as a museum to the past.

Selling your large property and downsizing to a modern, energy-efficient townhouse or a smaller single-story home dramatically reduces your baseline living costs. You slash your utility bills, eliminate burdensome maintenance chores, and often walk away with a substantial lump sum of home equity to bolster your investment portfolios. This transition transforms a stagnant physical asset into liquid capital that actively funds your retirement.

Financial Habit #11: Transitioning to Preventative Healthcare

Reactive healthcare bankrupts families. Waiting until a minor ache develops into a catastrophic condition guarantees expensive emergency room visits, complex surgeries, and extended hospital stays. Smart financial management requires you to leverage every preventative tool at your disposal.

Medicare covers comprehensive annual wellness visits, various cancer screenings, and vital vaccinations at no out-of-pocket cost to you. Schedule these appointments religiously. Catching high blood pressure, elevated blood sugar, or early-stage illness prevents the astronomical bills associated with severe medical interventions. Keeping your body healthy is the ultimate strategy to keep your bank accounts full.

Financial Habit #12: Traveling During Off-Peak Windows

One of the greatest benefits of leaving the workforce is gaining total control over your schedule. You no longer have to request vacation time during the most expensive, crowded times of the year. Standard vacation periods—like mid-summer and winter holidays—feature maximum surge pricing for flights, hotels, and rental cars.

Embrace frugal tips retirement travelers use constantly: book your trips during the shoulder seasons. Traveling to Europe in late September or visiting the Caribbean in early May allows you to experience prime destinations for a fraction of the cost. Airlines and resorts desperately slash prices during these periods to maintain occupancy. You secure a premium experience while saving 40% to 50% compared to peak-season tourists.

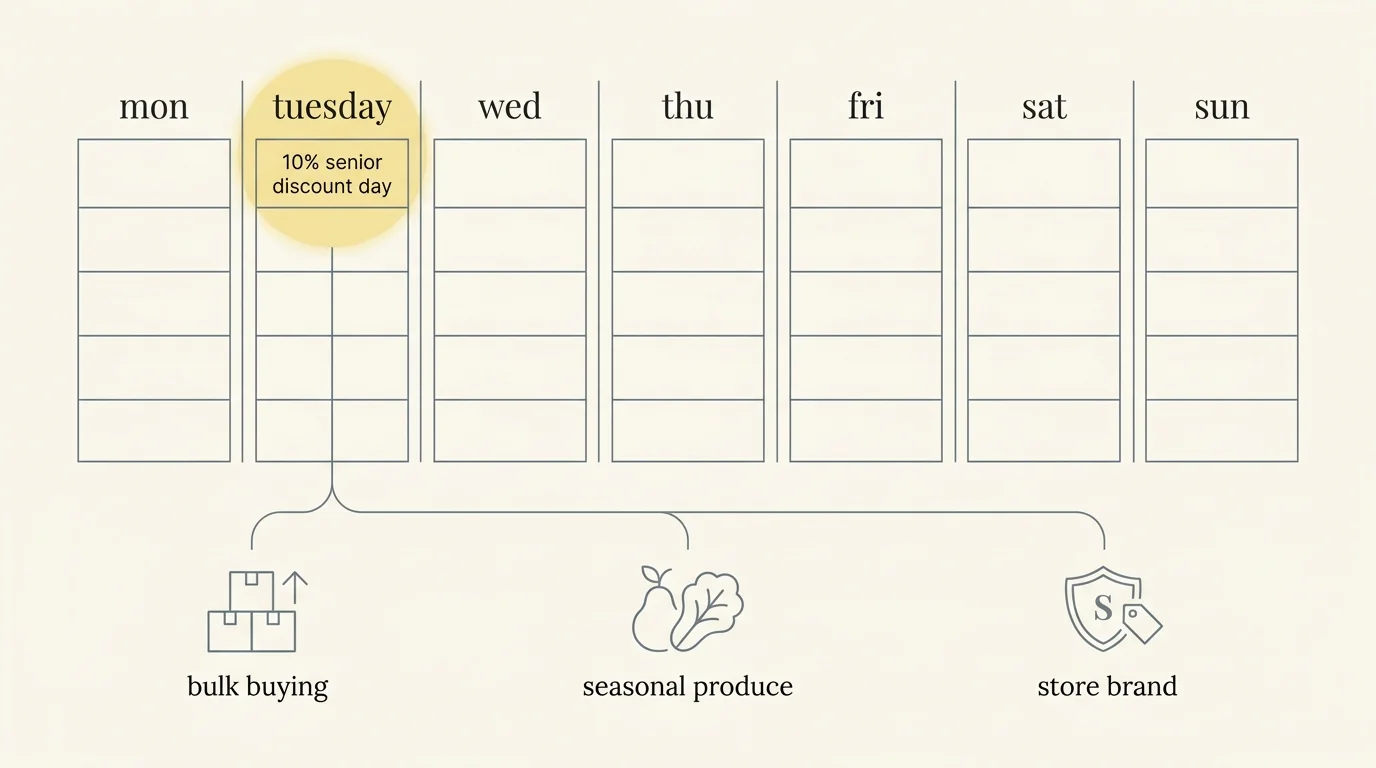

Financial Habit #13: Mastering Strategic Grocery Shopping

The supermarket is a battleground where poorly prepared shoppers lose significant amounts of wealth. Wandering the aisles without a list and purchasing premium name brands inflates your weekly food bill needlessly. In many cases, you are paying a 30% premium strictly for the colorful packaging and the television marketing budget of a brand-name product.

Switch to generic store brands for your pantry staples, canned goods, and cleaning supplies. The FDA requires generic food products to meet the same safety and nutritional standards as their premium counterparts. Combine this habit with strict meal planning to eliminate food waste. Buying only what you intend to eat, and eating everything you buy, prevents hundreds of dollars of spoiled food from ending up in the garbage bin.

Financial Habit #14: Shopping Insurance Premiums Relentlessly

Insurance companies utilize algorithms specifically designed to maximize profits from loyal customers. This practice, known as price optimization, means that the longer you stay with a homeowner or auto insurance provider, the higher your premiums will gradually climb. Customer loyalty in the insurance industry is financially punished, not rewarded.

Every two years, contact an independent insurance broker. Unlike captive agents who only sell one brand, independent brokers shop your policies across dozens of competing carriers. Let them find the exact same coverage for a lower price. Consistently rotating your insurance providers based on the best available rate keeps your premiums grounded and prevents you from subsidizing corporate profit margins.

Financial Habit #15: Eradicating High-Interest Consumer Debt

Carrying credit card debt into retirement is a financial emergency. When credit card interest rates hover between 20% and 30%, the math turns highly destructive. The interest charges compound rapidly, consuming the cash you desperately need for daily survival and forcing you to pull more heavily from your limited retirement accounts.

Deploy aggressive tactics to eliminate this debt. Utilize the avalanche method: make minimum payments on all accounts while funneling every available spare dollar toward the card with the highest interest rate. Once that card is clear, roll the payment amount to the next highest rate. Consider low-interest balance transfer offers to pause the bleeding while you pay down the principal. Debt freedom is the absolute cornerstone of financial stability.

The Big Picture: How This Affects Your Financial Future

Implementing these habits shifts you from a passive consumer to an active manager of your wealth. Saving $50 on groceries, $100 on insurance, and $140 on cable might seem like isolated victories, but they compound. Freeing up $500 to $1,000 every single month drastically alters the trajectory of your retirement. It removes the daily stress of wondering if your money will last.

When you aggressively reduce expenses, you lower the amount of capital you must withdraw from your retirement accounts. This keeps your principal balance higher, allowing it to generate more growth over time. You create a powerful financial fortress that protects you against medical emergencies, staggering inflation, and market downturns. Financial discipline does not restrict your freedom; it absolutely guarantees it.

Frequently Asked Questions

How do I combat inflation when my pension never increases?

If your income is strictly capped, your only lever of control is the outflow of your cash. You must relentlessly audit your bank statements every 90 days. Target variable expenses like energy usage, dining out, and grocery choices. By utilizing the 15 strategies listed above, you manufacture your own financial breathing room to offset the rising costs of goods and services.

Is it really worth the hassle to change banks for a high-yield savings account?

Yes. The process takes less than 30 minutes online. If you hold $25,000 in a traditional bank earning nothing, moving it to an account earning 4.5% generates over $1,100 in free cash annually. That is a massive return for half an hour of administrative work. Stop letting legacy banks profit off your idle cash.

How can I enjoy my retirement while being so frugal?

Being frugal is not about depriving yourself of joy; it is about eliminating waste. Paying $150 for a cable package you barely use does not bring you joy. When you eliminate these structural inefficiencies, you redirect that money toward things that actually matter—like funding travel, spending time with family, or pursuing hobbies. Frugality buys you the ultimate luxury: complete peace of mind.

For official information on consumer finance and debt, consult the CFPB. Tax information is available from the IRS. For investment basics, refer to the U.S. SEC.

Disclaimer: This article provides informational content and personal opinions, not professional financial advice. Consult a certified financial advisor for guidance tailored to your specific situation.

Leave a Reply