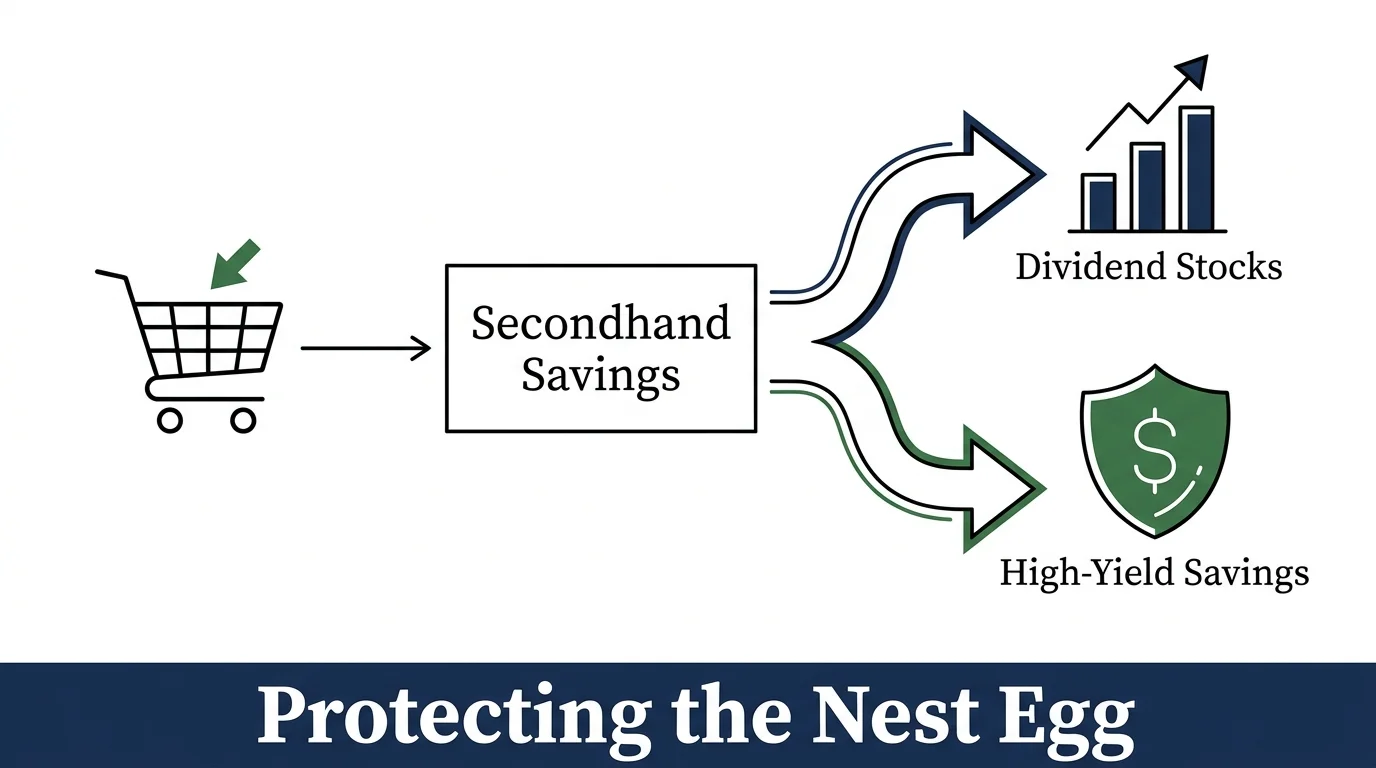

Entering retirement on a fixed income requires you to slash unnecessary expenses while maximizing your quality of life. Buying secondhand items provides an immediate shield against inflation, allowing you to keep thousands of dollars invested rather than losing them to retail markups. Thrift shopping retirees understand that brand-new goods lose substantial value the moment they leave the store; therefore, they actively seek high-quality used items to stretch their budgets. By adopting these frugal secondhand tips, you build a financial buffer that protects your nest egg from unexpected costs. Here are the twelve specific items smart seniors purchase used to preserve wealth and enjoy a comfortable lifestyle without compromising on quality.

Financial Habit #1: Purchasing Pre-Owned Vehicles

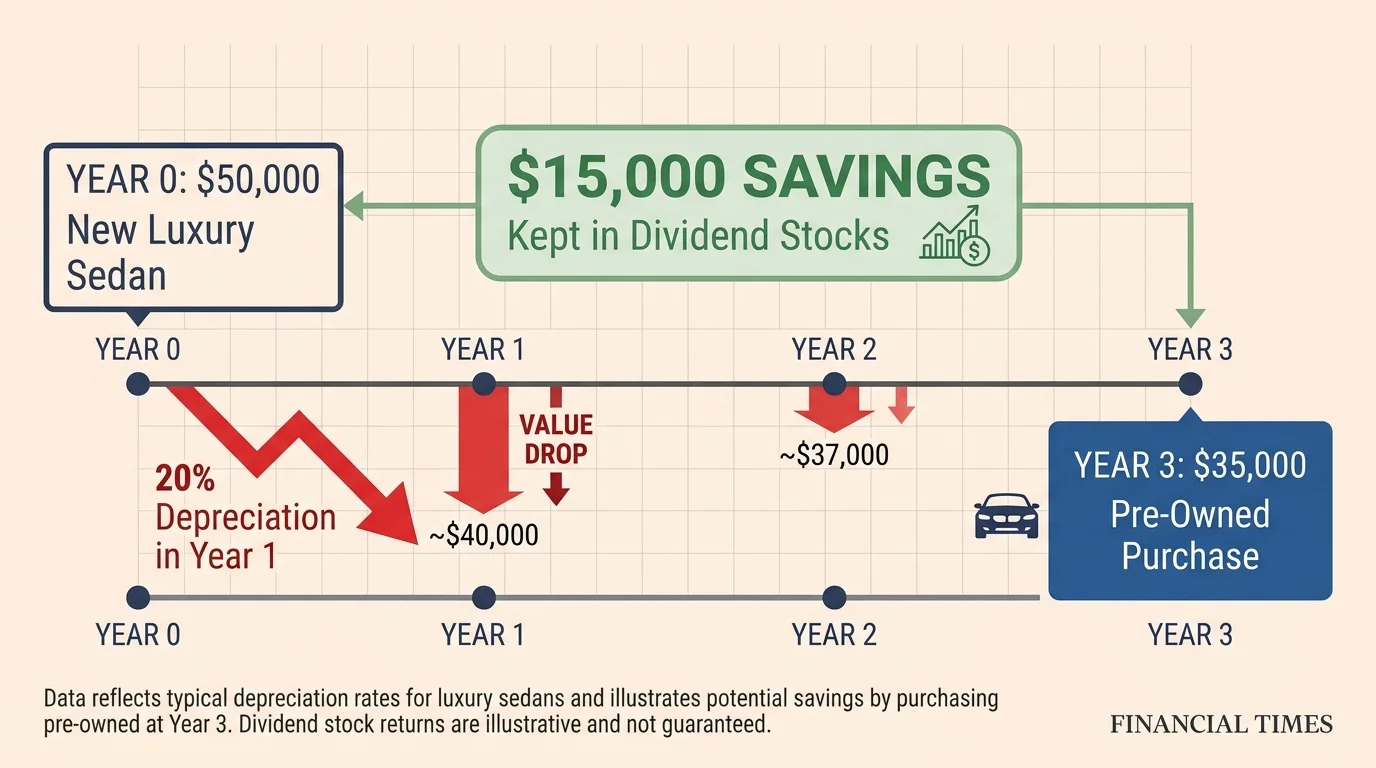

Automobile depreciation is the greatest wealth destroyer for people entering retirement. A brand-new car loses roughly twenty percent of its value in the first year alone, vanishing your hard-earned money into thin air. Frugal retirees recognize that purchasing a three-year-old vehicle yields the perfect balance of modern safety features, excellent mechanical reliability, and massive financial savings. Instead of financing a fifty-thousand-dollar luxury sedan at an inflated interest rate, you can secure a well-maintained off-lease equivalent for thirty-five thousand dollars. This strategy preserves fifteen thousand dollars of your capital; you can keep those funds invested in income-producing dividend stocks or high-yield savings accounts. By letting someone else absorb the brutal initial depreciation curve, you drastically reduce your monthly insurance premiums and your annual property taxes. The math is undeniable: avoiding new car dealerships is a cornerstone habit. To effectively save money used items like gently driven vehicles must become your priority.

Financial Habit #2: Sourcing Solid Wood Furniture

Retail furniture stores charge exorbitant markups for products often constructed from cheap particleboard, glues, and thin veneers. Conversely, antique shops, estate sales, and online marketplaces offer solid oak, mahogany, and maple pieces for a fraction of their original retail cost. In the growing movement to buy secondhand seniors are leading the charge by rescuing legacy pieces that possess unmatched durability. A sturdy, solid wood dining table or a dovetailed dresser will outlast anything purchased from a modern flat-pack retailer. A quality vintage credenza might cost two hundred dollars on the resale market, whereas a comparable new piece could easily exceed twelve hundred dollars. Older furniture boasts superior craftsmanship, featuring solid hardware and joints that stand the test of time. Furnishing your home with gently used, high-end pieces elevates your interior design while keeping thousands of dollars safely inside your bank account.

Financial Habit #3: Acquiring Refurbished Fitness Equipment

Many Americans start the new year by purchasing expensive treadmills, stationary bikes, and free weights, only to let them gather dust by March. Retirees focused on maintaining their physical health and financial wealth capitalize on this predictable cycle. They monitor online classifieds for barely used workout gear being sold by desperate homeowners trying to reclaim their garage space. A premium rowing machine that retails for fifteen hundred dollars frequently surfaces on the resale market for under four hundred dollars. When deciding to buy used 60+ shoppers easily build a comprehensive home gym without dipping into their retirement principal. Instead of paying a lofty monthly gym membership fee or financing a brand-new elliptical machine, you simply take advantage of another consumer’s abandoned fitness resolutions. Purchasing heavy cast-iron dumbbells or a sturdy weight bench secondhand guarantees the exact same physiological benefits as new equipment, minus the steep financial penalty.

Financial Habit #4: Securing Gently Used RVs and Travel Trailers

The dream of traveling the country during retirement often leads people to finance brand-new recreational vehicles at high interest rates. However, the RV market is notoriously saturated with lightly used models that have suffered brutal initial depreciation. A motorhome driven off the dealer lot loses thousands of dollars in value before it even reaches the first campground. Frugal retirees bypass the showroom completely, opting for units that are three to five years old. A travel trailer originally priced at forty thousand dollars can often be negotiated down to twenty-two thousand dollars by purchasing directly from a motivated private seller. This approach allows you to explore national parks and visit family across the country while maintaining a robust emergency fund. The money retained by purchasing a used camper can easily fund your fuel, campsite fees, and travel expenses for several years.

Financial Habit #5: Finding High-End Kitchen Appliances and Cookware

Equipping a kitchen with premium culinary tools does not require a trip to an upscale department store. Professional-grade cast-iron skillets, stainless steel pots, and heavy-duty stand mixers frequently appear at estate sales and local thrift shops. A vintage cast-iron pan, for example, often features a smoother cooking surface than modern equivalents and costs significantly less. High-quality stand mixers that retail for four hundred dollars routinely sell for under one hundred and fifty dollars when purchased pre-owned. These specific appliances are built with robust internal motors designed to last decades; therefore, buying them secondhand carries virtually no risk. By seeking out durable, legacy brands on the resale market, you elevate your home cooking experience and drastically cut down on your household expenses. You acquire lifetime kitchen tools for pennies on the dollar, leaving more room in your grocery budget for premium ingredients.

Financial Habit #6: Buying Secondhand Books and Media

Avid reading is a common and enriching retirement pastime, but purchasing brand-new hardcovers at retail prices quickly drains your entertainment budget. Smart seniors turn to local library sales, thrift stores, and online used book retailers to feed their reading habits without overspending. A pristine, newly released hardcover that costs thirty dollars at a major bookstore can often be acquired for two or three dollars just a few months later. Many retirees also exchange books with community groups or utilize neighborhood free libraries to cycle through new titles. Over the course of a year, choosing pre-owned books, DVDs, and physical media can easily save you over five hundred dollars. This simple behavioral shift satisfies your intellectual curiosity, keeps your mind sharp, and prevents your daily entertainment costs from quietly eroding your monthly cash flow.

Financial Habit #7: Hunting for Premium Gardening and Lawn Care Tools

Maintaining a beautiful landscape is both a rewarding hobby and a potential money pit if you insist on buying new equipment. Wheelbarrows, shovels, rakes, and hand trowels are virtually indestructible; paying a premium for a shiny new tool makes zero financial sense when older models feature superior forged steel and solid wood handles. Frugal retirees frequent garage sales and estate liquidations to purchase these high-quality implements for pocket change. Furthermore, powered equipment like lawnmowers and string trimmers are frequently sold for a fraction of their retail price by homeowners looking to clear out their sheds. A quick tune-up and a spark plug replacement can easily restore a fifty-dollar used mower to perfect working condition, saving you hundreds of dollars compared to a big-box store purchase. Your garden will thrive, and your wallet will remain full.

Financial Habit #8: Upgrading Wardrobes via Consignment and Thrift Shops

Transitioning into retirement often means shifting away from formal corporate attire toward comfortable, durable, and stylish everyday clothing. Rather than paying retail prices for premium brands, financially savvy retirees frequent upscale consignment boutiques and charity shops in affluent neighborhoods. These locations are goldmines for high-quality fabrics—such as cashmere sweaters, merino wool coats, and genuine leather shoes—offered at deep discounts. A designer winter jacket carrying a two-hundred-dollar price tag new might cost just twenty-five dollars on the secondhand rack. Thrift shopping retirees know that classic, well-made styles rarely change; therefore, building a timeless wardrobe from pre-owned racks keeps you looking sharp while radically reducing your clothing budget. Embracing this strategy prevents clothing depreciation from eating into the vital funds you need for healthcare, travel, and leisure activities.

Financial Habit #9: Adopting Pre-Owned Pets and Their Supplies

Welcoming a companion animal into your home brings immense joy and reduces stress during retirement, but pet ownership comes with steep upfront costs. Frugal retirees bypass expensive private breeders and instead adopt older dogs or cats from local animal shelters. This approach saves hundreds of dollars and usually includes initial vaccinations and necessary surgical procedures. Beyond the adoption itself, savvy seniors purchase pet accessories strictly on the secondhand market. Heavy-duty wire crates, travel carriers, elevated food bowls, and sturdy cat trees are abundantly available on community selling apps. A large dog crate that retails for one hundred and twenty dollars can routinely be picked up for twenty dollars from a neighbor whose puppy has outgrown it. Sterilizing these items with bleach and hot water ensures they are completely safe, keeping your pet happy and your household budget perfectly balanced.

Financial Habit #10: Seeking Out Refurbished Electronics and Tech Devices

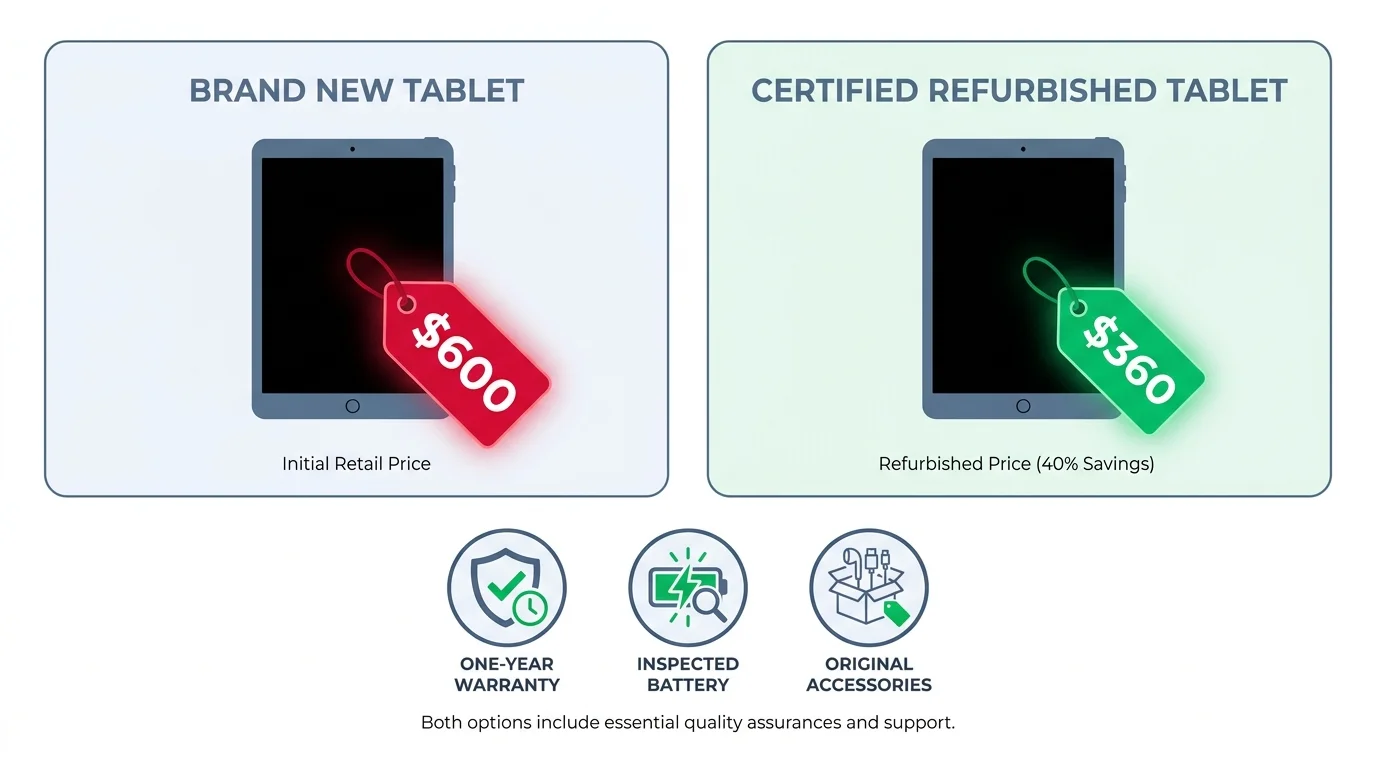

Staying connected with grandchildren, managing investment accounts, and streaming entertainment require reliable technology, but purchasing the latest flagship devices is a terrible financial move. Consumer electronics depreciate rapidly; a smartphone that costs one thousand dollars today will lose half its value within eighteen months. Retirees who want premium technology frequently purchase certified refurbished laptops, tablets, and smartphones directly from manufacturers or reputable tech vendors. These devices undergo rigorous testing, receive brand-new batteries, and come with substantial warranties that rival new products. A refurbished tablet offers the exact same browsing and video-calling capabilities as a brand-new model, yet leaves three hundred dollars securely in your pocket. By refusing to pay the early-adopter premium, you ensure your technology budget never compromises your long-term financial security.

Financial Habit #11: Purchasing Used Golf Clubs and Sporting Goods

Staying active on the golf course, pickleball court, or local bike trail is excellent for your physical and mental health. However, modern sporting goods carry massive retail markups. Manufacturers release slightly updated golf clubs every single year, convincing amateur players to upgrade and dump their perfectly functional gear on the resale market. Astute retirees capitalize on this trend by purchasing high-end, name-brand golf club sets that are only two or three years old. A titanium driver that initially retailed for five hundred dollars can often be found for one hundred and fifty dollars, exhibiting nothing more than minor cosmetic scuffs. The same financial principle applies to premium bicycles, tennis racquets, and fishing gear. You gain access to top-tier equipment that enhances your athletic performance without paying the exorbitant retail premium required just to peel the plastic off the grip.

Financial Habit #12: Procuring Vintage Musical Instruments

Many people decide to learn the piano, guitar, or violin during retirement, fulfilling a lifelong dream of mastering an instrument. However, beginner instruments purchased brand new are often poorly constructed, while professional models carry staggering price tags. The secondhand market is overflowing with beautifully crafted instruments sold by individuals who quickly abandoned their musical aspirations. Purchasing a used acoustic guitar allows you to acquire solid wood construction—which produces vastly superior resonance—for the price of a cheap, new laminate model. Furthermore, musical instruments tend to hold their value incredibly well on the resale market. If you decide playing is not for you after six months, you can easily resell the item for exactly what you paid. This makes exploring your musical talents a completely risk-free investment for your mind and your money.

The Big Picture: How This Affects Your Financial Future

Adopting the habit of buying secondhand fundamentally transforms your retirement trajectory. Every dollar you keep from the clutches of retail markup is a dollar that continues to compound in your investment portfolio or serve as a cash buffer against unexpected medical emergencies. The core philosophy here is not about depriving yourself; it is about aggressively optimizing the value of your currency. By sidestepping the steep depreciation curve associated with brand-new vehicles, high-end furniture, and consumer electronics, you retain maximum control over your wealth. You successfully uncouple your lifestyle from the relentless, exhausting cycle of modern consumerism. Over the span of a twenty-year retirement, these localized, daily choices to buy used rather than new will easily amount to hundreds of thousands of dollars in retained capital. Ultimately, disciplined frugality provides you with the ultimate luxury: absolute financial peace of mind.

Frequently Asked Questions

Is it actually safe to buy used electronics online?

Yes, provided you purchase from highly reputable sources. Always look for certified refurbished products sold directly by the manufacturer or through established vendors that offer a minimum ninety-day warranty and a clear return policy. Avoid buying complex electronics from anonymous sellers on local classifieds unless you can fully test the device’s screen, battery life, and charging ports before handing over your cash.

How do I negotiate the best price on secondhand furniture or appliances?

Research the fair market value of the exact item before you initiate contact. When you communicate with the seller, be polite but firm, and offer a specific dollar amount rather than asking for their lowest price. Bringing cash and offering to haul the heavy item away immediately gives you tremendous leverage to secure a twenty to thirty percent discount off their initial asking price.

Are there any specific items I should absolutely never buy used?

Yes. You should never purchase used safety equipment, such as bicycle helmets or car seats, because you cannot verify if their structural integrity has been compromised in a previous accident. Additionally, items like mattresses and upholstered furniture from questionable sources carry the risk of bedbugs, making the potential extermination costs far outweigh any initial savings you might achieve at the point of sale.

How much can a typical retiree realistically save by switching to secondhand goods?

While individual results vary based on your shopping habits, applying these principles strictly to major purchases—such as vehicles, RVs, and home furnishings—can easily save a household over ten thousand dollars annually. When you factor in the retained investment growth on those saved dollars over a two-decade retirement, the long-term financial impact easily stretches well into the six figures.

For official information on consumer finance and debt, consult the CFPB. Tax information is available from the IRS. For investment basics, refer to the U.S. SEC.

Disclaimer: This article provides informational content and personal opinions, not professional financial advice. Consult a certified financial advisor for guidance tailored to your specific situation.

Leave a Reply