Savvy seniors are actively hacking the system to squeeze every possible dollar out of their fixed incomes. You might assume your post-work budget relies entirely on standard Social Security checks and a 401(k) withdrawal rate, but the most successful retirees employ aggressive optimization strategies to outpace inflation. Stretching retirement income requires a contrarian approach to housing, healthcare, and daily consumption. By rethinking your baseline expenses and exploiting little-known tax loopholes, you build a fortress around your wealth. This guide exposes the exact maneuvers financially bulletproof seniors use to manipulate their cash flow. Adopting these aggressive retiree strategies transforms a fragile nest egg into a lifetime of financial security.

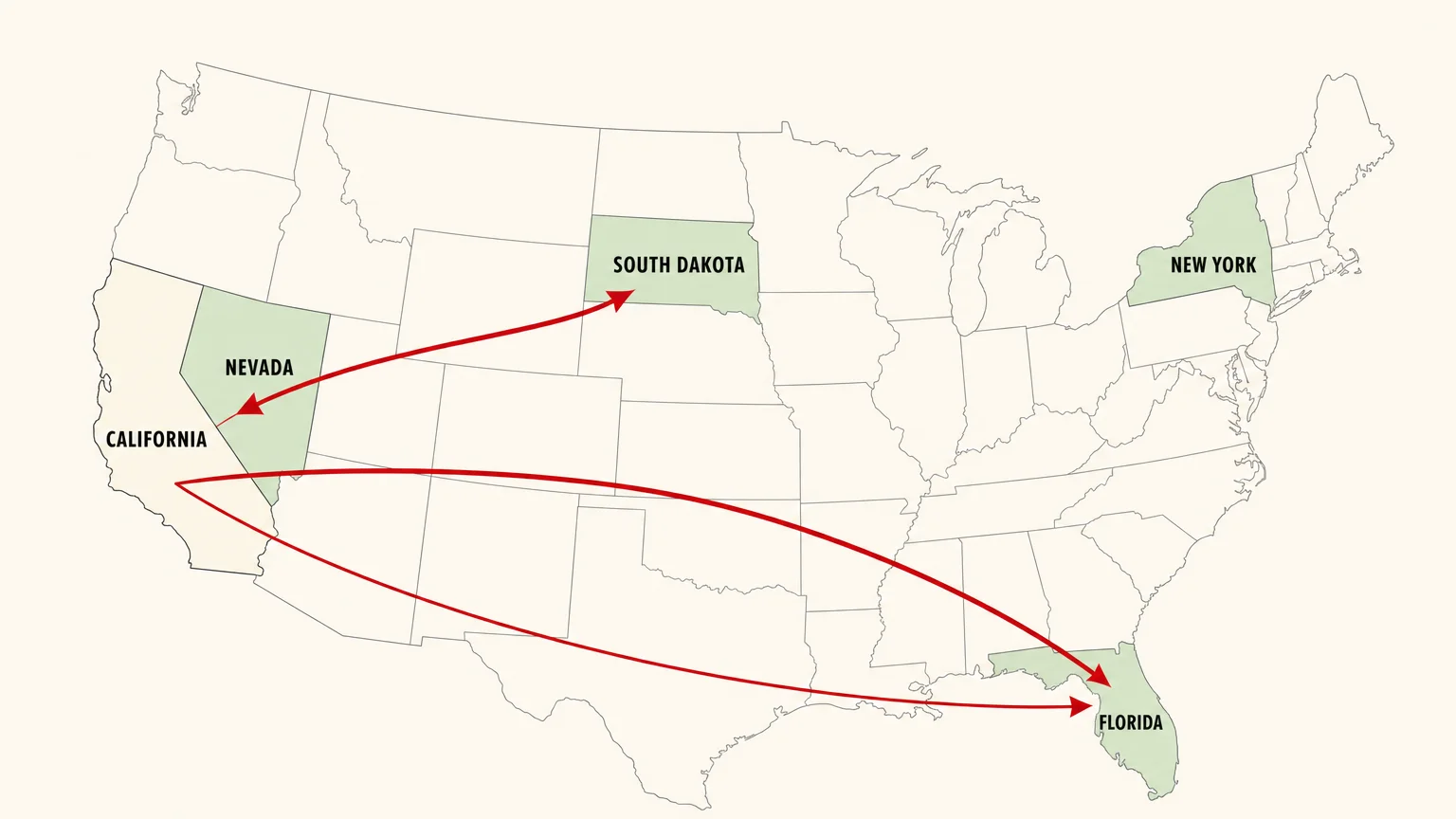

Let’s double check the states in the image: California, Nevada, South Dakota, New York, Florida.

Yes, Florida and Nevada are highlighted in green (tax-friendly).

Tip 1: Relocating to Tax-Friendly Jurisdictions

Where you live dictates how much of your nest egg you actually keep. States like Florida, Nevada, and South Dakota charge zero state income tax; a critical advantage when you rely on fixed distributions. Furthermore, a growing number of states refuse to tax Social Security benefits, instantly boosting your net income without requiring you to earn an extra dime. Savvy seniors map out these tax havens and execute calculated moves across state lines to aggressively protect their wealth from government overreach.

Moving across the country might seem drastic; however, the math frequently justifies the hassle. Relocating from a high-tax state like New York or California to a favorable jurisdiction saves you tens of thousands of dollars over a decade. You must calculate the total tax burden, including property taxes and sales taxes, to ensure your new destination truly supports a budget-friendly retirement. For example, Texas features zero state income tax but levies aggressively high property taxes, which can obliterate your savings if you purchase a large home. Conversely, a state like Nevada balances no income tax with relatively moderate property tax rates. Cutting your tax bill is the fastest way to give yourself an instant raise.

Tip 2: Exploiting Medicare Advantage Allowances

You are likely leaving money on the table if you treat your health insurance strictly as a medical safety net. Modern Medicare Advantage plans frequently include hidden flex cards and over-the-counter allowances designed to pay for everyday necessities. Insurers embed these perks to attract enrollees, yet a shocking percentage of seniors never activate their benefits. These allowances directly cover groceries, dental copays, utility bills, and even non-prescription pharmacy items like vitamins and pain relievers.

Call your insurance provider immediately and demand a full breakdown of your unadvertised perks. Taking advantage of a grocery allowance frees up cash you can redirect toward other living expenses. Furthermore, standard Medicare severely lacks comprehensive dental, vision, and hearing coverage, forcing you to pay out of pocket. Savvy retirees utilize independent insurance brokers during the annual open enrollment period to compare hundreds of competing Medicare Advantage plans and find the richest secondary perks. Benefit maximization requires treating your health insurance policy like a prepaid debit card; drain every available cent before the annual expiration date to drastically reduce your out-of-pocket spending.

Tip 3: Executing Geographic Healthcare Arbitrage

The American healthcare system routinely bankrupts unprepared retirees. Proactive seniors circumvent this trap through geographic healthcare arbitrage. This strategy involves crossing international borders—often into Mexico or Canada—to purchase identical prescription medications and dental services at a fraction of the domestic price. Routine dental implants or expensive daily medications cost significantly less abroad, allowing you to stretch your benefits without sacrificing the quality of your care.

If traveling sounds unappealing, you can still execute domestic arbitrage. Online pharmacies and direct-to-consumer drug platforms, such as cost-plus pricing models, bypass traditional insurance middlemen to offer generic medications at wholesale prices. These platforms strip away the complex rebate games played by pharmacy benefit managers, resulting in transparent and incredibly low price tags. Compare your Medicare Part D copays against cash-pay prices on these alternative platforms. You will frequently discover that paying cash out-of-pocket costs drastically less than utilizing your premium insurance benefits. Protecting your wealth requires mercilessly auditing your medical expenses and refusing to accept retail pharmacy pricing.

Tip 4: House Hacking for Supplemental Cash Flow

Your primary residence likely represents your largest dormant asset. Instead of letting empty bedrooms gather dust, aggressive seniors embrace house hacking to generate reliable, passive income. Renting out a converted basement, a spare bedroom, or an accessory dwelling unit creates a steady stream of cash that directly subsidizes your mortgage and property taxes. This aggressive income strategy turns an expensive liability into a self-sustaining financial engine.

You do not need to become a full-time, traditional landlord to succeed. If you live near a major hospital system, consider renting exclusively to traveling nurses. These healthcare professionals require furnished, short-term accommodations, undergo rigorous background checks, and earn substantial incomes. Alternatively, short-term rental platforms allow you to lease your space exclusively during high-demand weekends or local events, giving you total control over your privacy. Maximizing your property utility significantly accelerates your benefit maximization plan, ensuring your living situation pays you rather than draining your fixed income.

Tip 5: Stacking Unadvertised Age-Based Discounts

Forget the basic ten percent off at a local diner. The most impactful senior discounts hide buried in the fine print of major service contracts. Auto insurance providers offer substantial rate reductions for older drivers who complete fast, online defensive driving courses. Telecommunications companies maintain secretive, ultra-low-cost phone and internet tiers specifically reserved for seniors on fixed incomes. You must explicitly request these legacy tiers because sales representatives earn commissions by upselling, not by saving money for their customers.

Look beyond the private sector and leverage municipal and state resources specifically priced for senior citizens. Countless states offer lifetime passes to state parks and recreational facilities for a negligible one-time fee. Treat your age as a VIP discount card for every recurring bill in your household. Call your internet provider, your cell phone carrier, and your home security company to demand a senior-specific rate structure. If they refuse, threaten to cancel and switch to a competitor. These corporations desperately want to retain your business and will frequently slash your monthly bill to prevent customer churn.

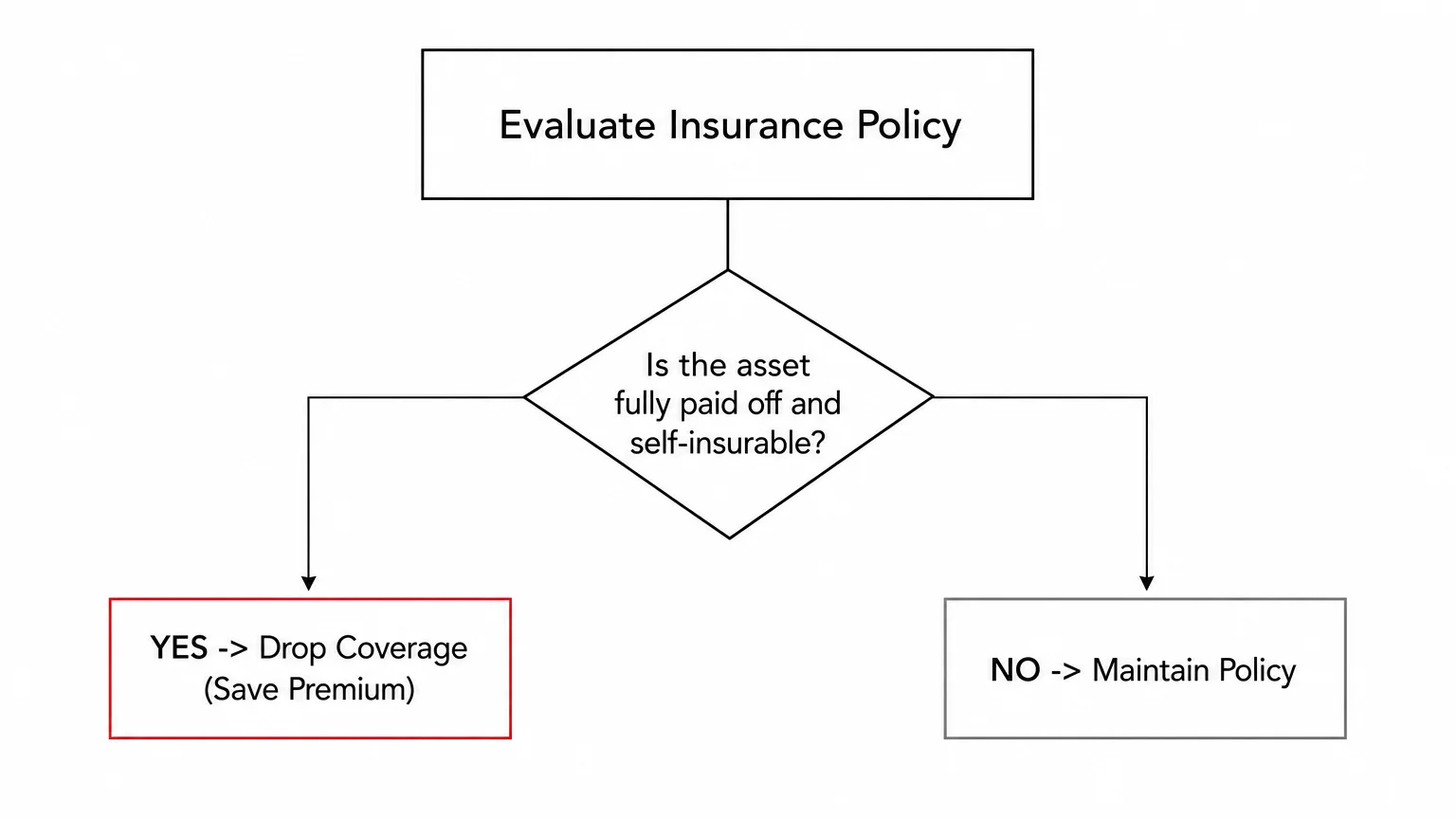

Tip 6: Dropping Unnecessary Insurance Policies

Fear drives many seniors to maintain insurance coverage they outgrew decades ago. Continuing to pay premiums on a massive whole life insurance policy makes zero financial sense once your children achieve financial independence and your mortgage vanishes. Your retirement savings now serve as your self-funded life insurance. Canceling obsolete policies instantly injects hundreds of dollars back into your monthly budget, providing immediate relief from unnecessary overhead.

Evaluate every insurance contract you currently hold. Drop collision coverage on an ancient vehicle that holds little actual cash value. Instead of holding useless policies, redirect a small fraction of those premium dollars into a robust umbrella liability policy, which costs significantly less and actually protects your existing assets from devastating lawsuits. Reassess your home insurance deductibles; raising your deductible lowers your monthly premium and forces you to self-insure minor repairs. Trimming the fat from your insurance portfolio ensures you stop enriching massive conglomerates and start keeping more of your hard-earned benefits.

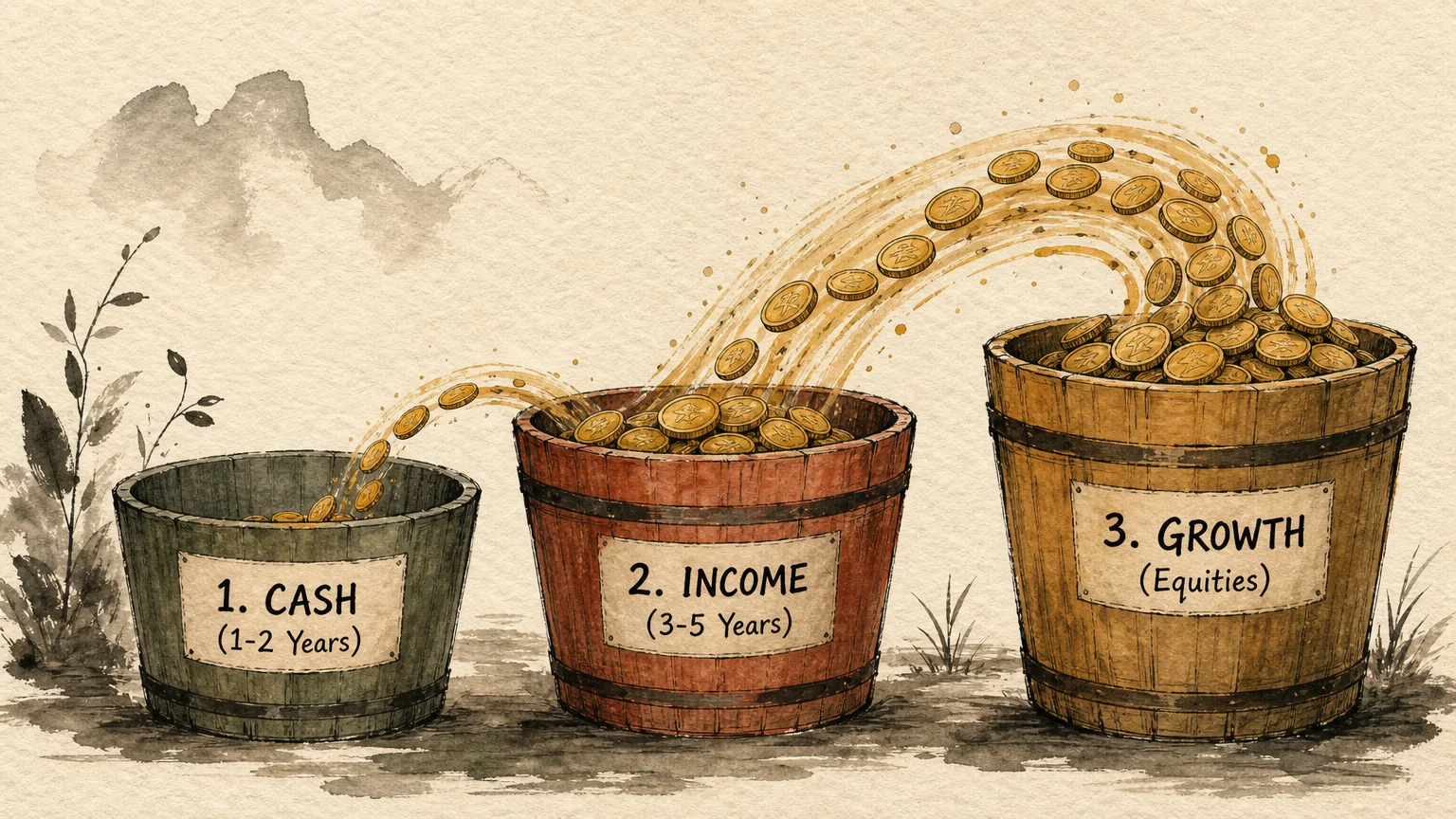

Tip 7: Utilizing the Cash Bucket Strategy

Market volatility terrifies retirees who rely on portfolio withdrawals to survive. You eliminate this panic by implementing a strict cash bucket strategy. You structure your assets by keeping one to two years of living expenses entirely in liquid, high-yield savings accounts or short-term certificates of deposit. This immediate cash buffer guarantees you can pay your bills even if the stock market crashes tomorrow.

A fully optimized bucket strategy utilizes three distinct tiers. The first bucket holds your immediate cash reserves. The second bucket contains intermediate investments like high-grade municipal bonds or certificates of deposit that mature in three to seven years. The third bucket holds your growth-oriented equities meant to sit untouched for a decade or more. When you isolate your immediate spending needs from market fluctuations, you never have to sell stocks at a steep loss just to buy groceries. Managing your liquidity ensures you stretch your benefits efficiently without letting Wall Street dictate your monthly standard of living.

Tip 8: Ruthless Grocery App Optimization

Supermarket inflation destroys fixed incomes faster than almost any other economic force. Traditional coupon clipping barely makes a dent, but mastering modern grocery application algorithms unlocks massive savings. Supermarkets track your purchasing habits and issue high-value, personalized digital coupons designed to keep you loyal to their brand. You can stack these digital store offers with third-party cash-back applications—which scan your receipts and deposit actual cash into your bank account—to double or triple your savings on essential items.

Successful grocery optimization demands treating your shopping trip like a tactical mission. Build your weekly menu strictly around loss leaders—heavily discounted items stores use to lure you through the doors. Buy non-perishable staples in bulk only when you can combine a massive sale price with a digital rebate. By weaponizing your smartphone at the checkout counter, you effectively reclaim thousands of dollars annually, drastically easing the burden on your monthly Social Security check. You cannot control global supply chains, but you absolutely control how aggressively you exploit grocery pricing algorithms.

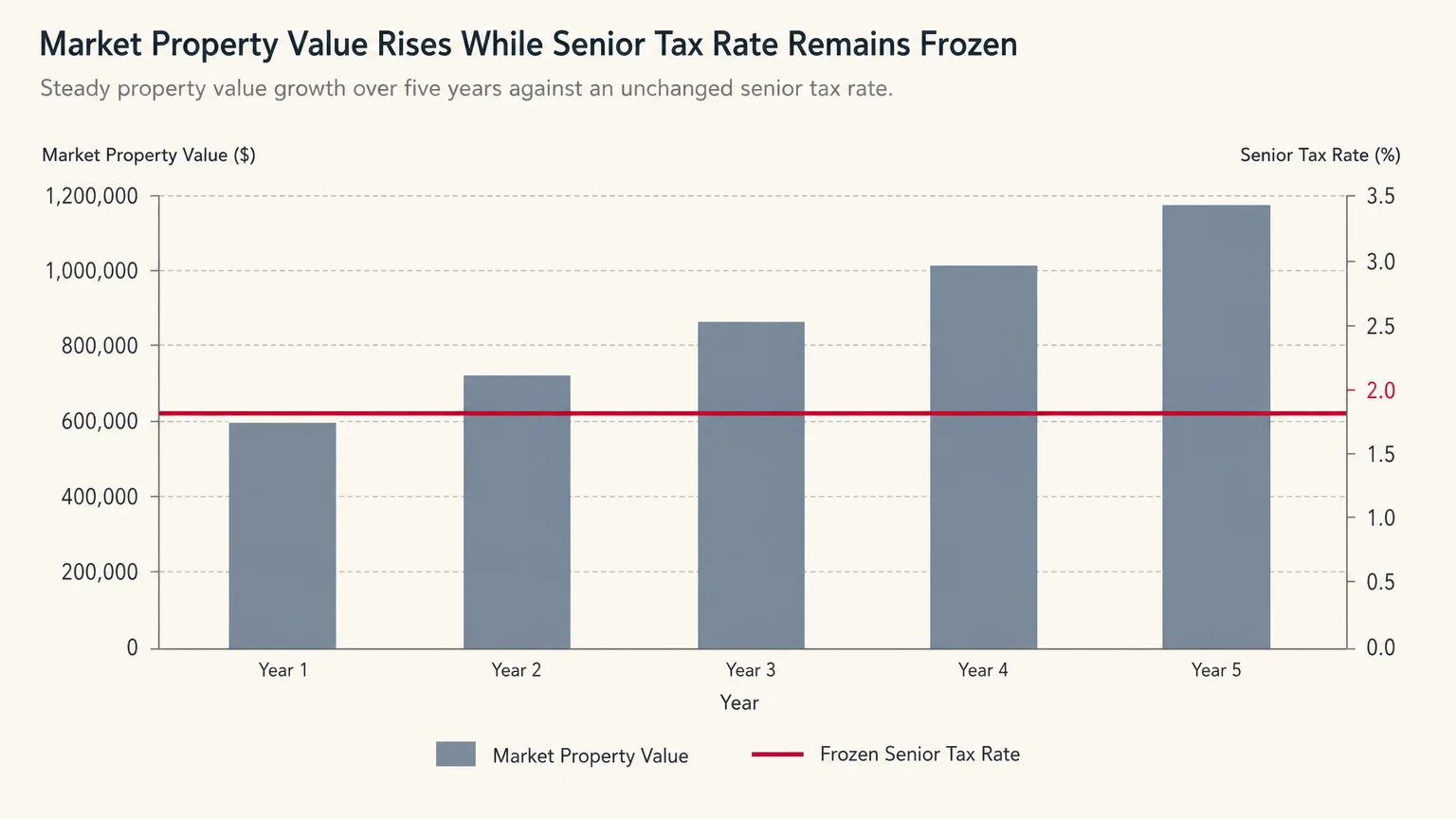

Tip 9: Securing Municipal Property Tax Freezes

Property taxes relentlessly climb upward, silently threatening your ability to age in place. However, countless municipalities offer powerful property tax exemptions, deferrals, and freezes specifically tailored for senior citizens. These programs lock your property tax rate at a historical baseline or slash your assessed home value, effectively shielding you from future municipal tax hikes. Local governments rarely advertise these lifelines; you must proactively hunt them down at your county assessor’s office.

Qualifying for a property tax freeze typically requires meeting specific age and income thresholds. Even if you slightly exceed the standard income limits, investigate alternative exemptions related to medical expenses or veteran status. If your local government does not offer a blanket freeze, you must aggressively challenge your annual property tax assessment. Assessed values frequently lag behind real-world market conditions, resulting in artificially inflated tax bills. Securing this municipal protection ensures your housing costs remain predictable and manageable throughout your entire retirement.

Tip 10: Leveraging State-Sponsored Utility Assistance

Skyrocketing winter heating bills and summer air conditioning costs frequently wreck a tightly managed budget. Many seniors suffer in uncomfortable temperatures simply to avoid a massive utility bill, totally unaware that heavily funded assistance programs exist to shoulder the burden. The Low Income Home Energy Assistance Program—commonly known as LIHEAP—provides direct cash grants to offset residential energy costs. You do not need to live in abject poverty to qualify; the income thresholds easily accommodate many typical fixed-income households.

Beyond federal grants, utility companies run internal hardship and senior assistance programs. You can apply for medical baseline allowances if you require electricity to run vital medical equipment like CPAP machines. Furthermore, request a transition to time-of-use billing if your utility provider offers it. By shifting your heavy energy consumption to off-peak nighttime hours, you pay a drastically reduced rate per kilowatt-hour. Additionally, state-sponsored weatherization programs will send contractors to your home to install free insulation, seal leaky windows, and upgrade inefficient appliances. Aggressively applying for these grants permanently reduces your monthly carrying costs.

The Bottom Line: What This Means for Your Wallet

Surviving on a fixed income does not mean accepting financial defeat. You command total control over your expenses, your tax liabilities, and your approach to daily consumption. Stretching retirement income requires abandoning the passive mindset of simply cashing your Social Security check and hoping for the best. Instead, you must aggressively audit every dollar leaving your bank account and ruthlessly optimize your fixed overhead.

The tactics outlined here represent the exact playbook financially secure seniors use to outmaneuver inflation. Whether you pursue extreme measures like geographic healthcare arbitrage or straightforward fixes like dropping obsolete insurance policies, every action directly compounds your wealth. You must view your retirement budget as a dynamic, living system that demands constant refinement. By implementing these benefit maximization techniques today, you ensure your savings will outlast you, providing total freedom and unshakeable peace of mind for decades to come.

Frequently Asked Questions

Can I really stop paying state taxes on my Social Security income?

Yes, depending entirely on where you maintain your primary residence. A vast majority of states do not tax Social Security distributions at all. Even states that do levy a tax frequently offer generous exemptions based on your adjusted gross income. You must consult your state’s department of revenue to verify your specific tax obligations and explore potential exemptions before deciding to relocate.

Will using a cash bucket strategy protect me from inflation?

The cash bucket itself does not beat inflation; it serves as a defensive shield against sequence of returns risk. By keeping one to two years of expenses in cash or short-term instruments, you avoid selling your equities during a market crash. The remaining components in your portfolio remain invested in the stock market to generate the growth necessary to outpace inflation over the long haul.

How do I find out if my Medicare Advantage plan includes flex cards or allowances?

You need to call the customer service number located directly on the back of your insurance card. Do not rely on generic promotional materials. Demand a comprehensive explanation of your specific policy’s over-the-counter allowances, transportation vouchers, and grocery benefits. Because plans change annually, you must perform this audit every single year during the open enrollment period to ensure you maximize your benefits.

Are online prescription platforms safe for purchasing my medications?

Legitimate direct-to-consumer pharmacies operate safely and legally within the United States, utilizing domestic supply chains to deliver generic medications directly to your door. You must verify that the pharmacy requires a valid prescription from your doctor and maintains proper state licensing. By utilizing these transparent pricing models, you bypass the massive, hidden markups routinely applied by traditional retail pharmacies.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply