Most retirees leave thousands of dollars on the table by relying solely on Social Security and traditional investment withdrawals for their retirement cash flow. You can unlock substantial alternative income by tapping into financial vehicles and physical assets you already own but probably ignore. Maximizing your retiree finances requires aggressive income diversification that goes far beyond stock dividends and basic pension plans. Financial advisors frequently push standard brokerage accounts, but true financial independence often hides in tax-advantaged loopholes and underutilized property. Once you stop treating your post-work years like a rigid mathematical formula and start viewing them as a flexible business strategy, you will discover multiple streams of passive retirement income quietly waiting in your background.

Tip #1: The Stealth Power of Health Savings Accounts

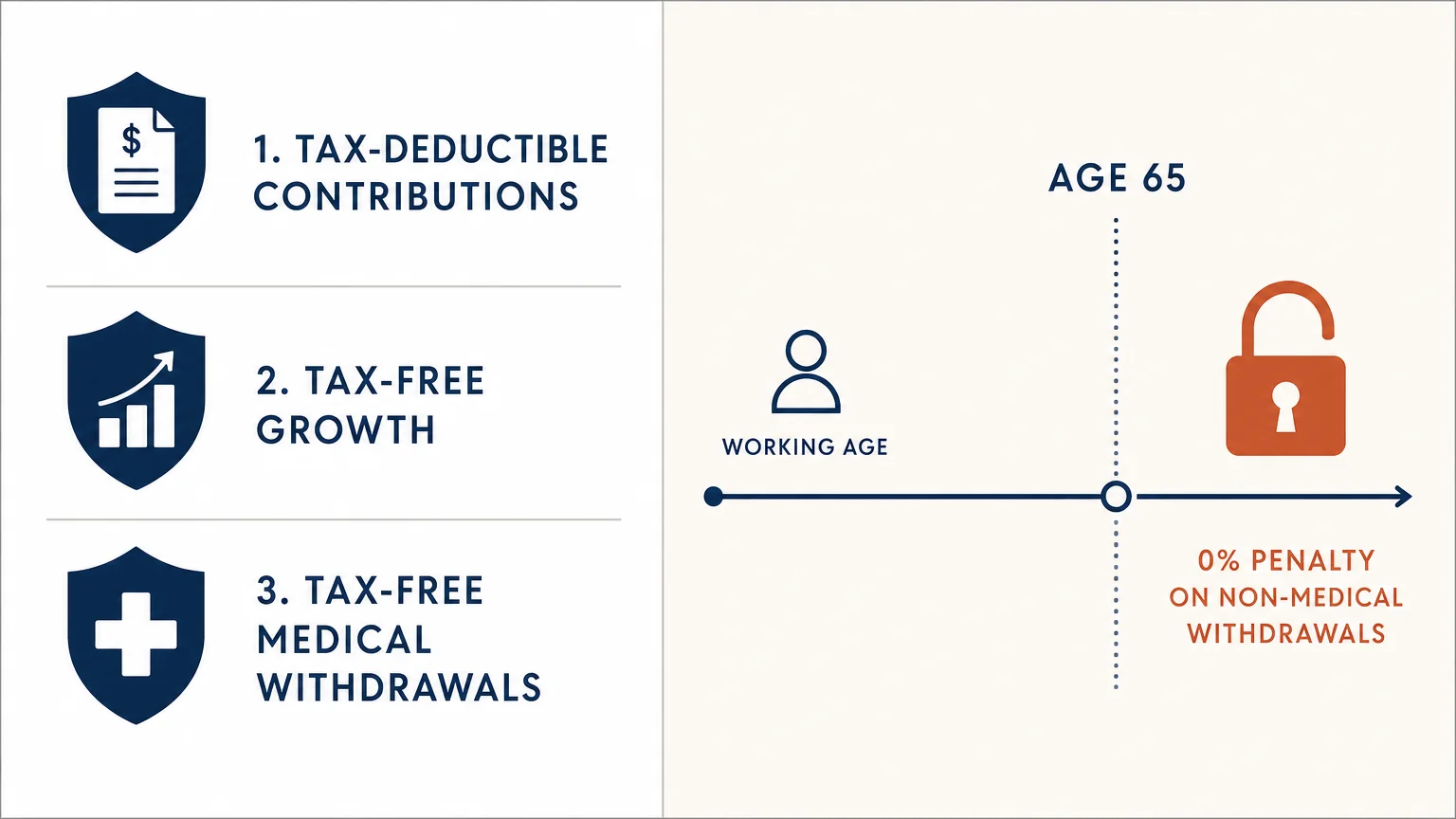

Health Savings Accounts (HSAs) are frequently viewed as basic checking accounts meant strictly for covering routine copays and prescription costs. You must discard this limiting mindset immediately. An HSA operates as the ultimate tax-advantaged account available in the American financial system, boasting a rare triple-tax advantage: your contributions are tax-deductible, your investment growth is tax-free, and your medical withdrawals are completely tax-free. However, the real secret for generating reliable alternative income activates the moment you turn sixty-five.

At age sixty-five, the rigid rules governing your HSA fundamentally shift in your favor. You gain the ability to withdraw your invested funds for absolutely any non-medical reason without triggering the steep twenty percent federal penalty. If you need to pull money out to purchase a reliable vehicle, fund a home renovation, or simply pay for weekly groceries, you only pay regular income tax on the distribution. This structural change forces the account to function exactly like a traditional IRA, providing you with a massive, secondary pool of pretax retirement cash flow that most people entirely overlook.

The ultimate strategy involves keeping meticulous digital records of your out-of-pocket medical receipts throughout your working life. The Internal Revenue Service does not impose a strict timeframe for reimbursing yourself for past medical expenses. You can pay your hospital bills with standard cash today, let your HSA investments compound exponentially in the stock market for two decades, and then claim a massive, lump-sum tax-free reimbursement whenever you want. Cashing in twenty years of saved receipts creates an immediate, untaxed windfall right when your retiree finances need a vital defense against inflation.

Tip #2: Renting Out Underutilized Property and Storage Space

You likely walk past highly lucrative real estate assets every single day without realizing their raw profit potential. The modern sharing economy has evolved far beyond renting out your spare bedroom to noisy weekend tourists. Today, specialized peer-to-peer storage platforms empower you to generate steady passive retirement income by casually leasing out the empty space in your garage, your wide driveway, or your unused side yard.

Commercial storage facilities relentlessly charge outrageous monthly fees, and everyday Americans remain desperate for cheaper, safer alternatives to park their expensive recreational vehicles, boats, or boxes of seasonal gear. By actively undercutting corporate storage facilities by just ten or twenty percent, you provide a high-demand community service while creating a brilliant new stream of alternative income. If you own an empty, climate-controlled garage, you can easily charge a significant premium to safely house a neighbor’s classic car during the harsh winter months.

This localized strategy requires almost zero physical labor and requires no active management. Once the user signs the digital lease agreement and parks their vehicle on your property, the rental money automatically deposits directly into your bank account each month. It operates as the perfect avenue to optimize your income diversification without forcing you to take on a physically demanding part-time job or risk your capital in erratic financial markets. You effectively monetize property you already legally own and already pay property taxes on.

Tip #3: The Home Equity Conversion Mortgage Line of Credit

Reverse mortgages carry a heavy cultural stigma born from outdated, predatory industry practices. Modern Home Equity Conversion Mortgages (HECMs) are heavily regulated by the federal government and offer a brilliant line of credit strategy that elite financial planners use to bulletproof retiree finances. Unlike a traditional home equity line of credit secured from a standard commercial bank, a HECM line of credit cannot be unexpectedly frozen or canceled if local housing prices suddenly plummet.

The absolute most overlooked feature of the HECM line of credit is its guaranteed, built-in growth rate. The unused portion of your available credit actually grows larger every single year, completely independent of your physical home’s market value. If you aggressively open the credit line early in your retirement and leave the funds untouched for a decade, your available borrowing power expands significantly. This mathematical quirk creates an incredibly robust financial safety net that you control entirely.

Smart retirees deploy this credit line as a strategic buffer asset during severe economic downturns. When the stock market crashes, selling your portfolio shares to buy groceries locks in permanent, devastating capital losses. Instead of liquidating depressed index funds, you draw tax-free cash from your expanding HECM line of credit to cover your living expenses. Once the stock market inevitably recovers its lost ground, you confidently resume your standard portfolio withdrawals and optionally repay the borrowed funds at your own pace.

Tip #4: Cash Value Life Insurance Dividend Payouts

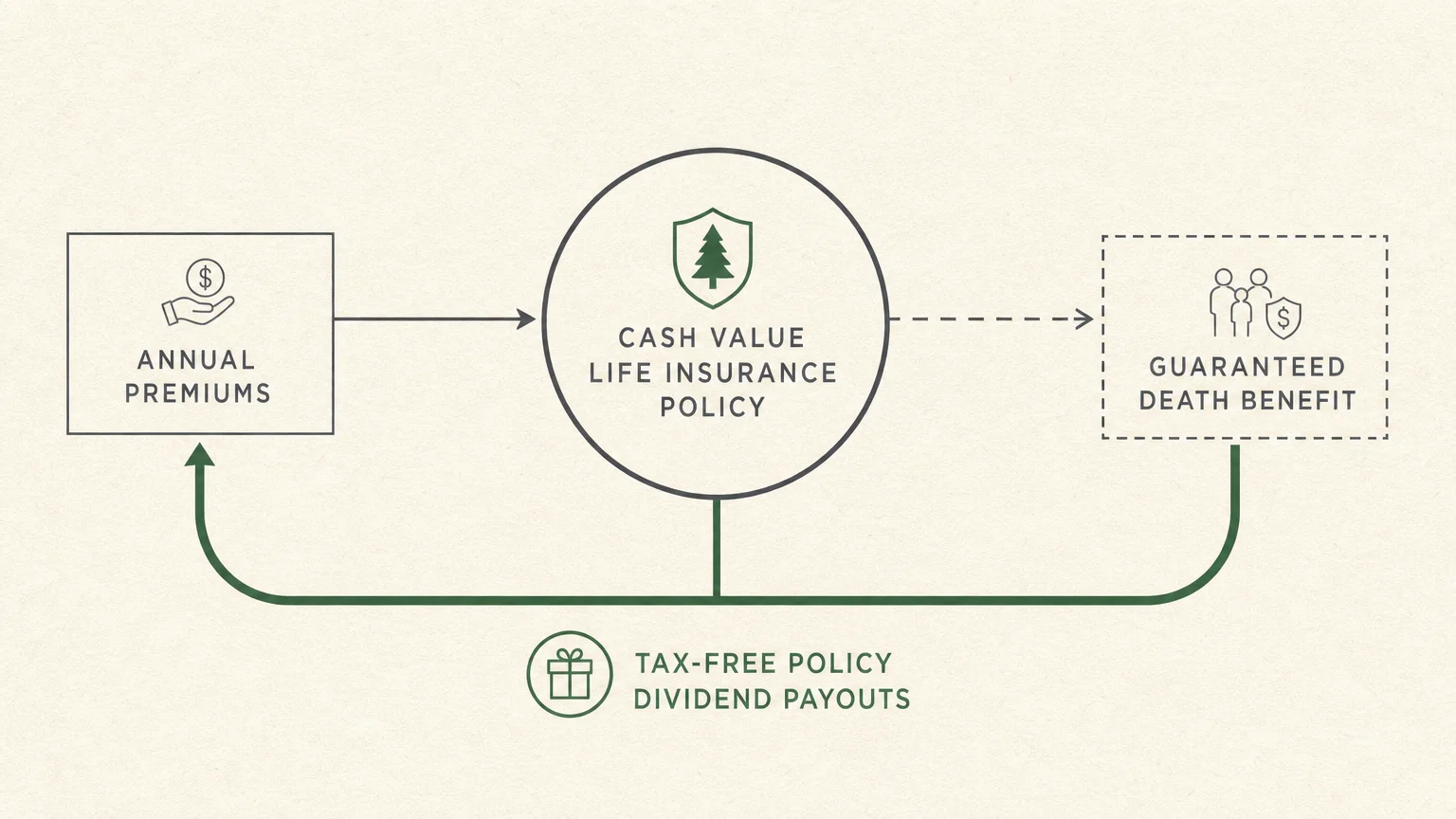

Millions of Americans dutifully purchased permanent, participating whole life insurance policies decades ago, yet they incorrectly view these rigid contracts merely as a final death benefit for their children. If you hold a mature policy with a highly reputable mutual insurance company, you actually possess a highly flexible reservoir of alternative income. These unique policies accumulate guaranteed cash value and earn annual dividend payments that can radically reshape your retirement cash flow.

As your life insurance policy matures over the decades, the annual dividend payments naturally grow larger. Instead of allowing the insurance company to automatically use these dividends to purchase additional, unnecessary insurance coverage, you can directly instruct your carrier to pay the dividends to you in liquid cash. Because the IRS generally treats these specific dividends as a simple return of the premium you paid over the years, the distributions hit your checking account completely tax-free up to your total cost basis.

Furthermore, you hold the contractual right to extract tax-free loans directly against the accrued cash value of the policy. Executing a strategic policy loan provides immediate passive retirement income during specific years when you want to intentionally lower your taxable income bracket to qualify for subsidies. You never have to pay the loan back while you are alive; the insurance company simply subtracts the outstanding loan balance from the final death benefit payout, allowing you to access the money when you actually need it.

Tip #5: Selling Covered Calls on Dividend Stocks

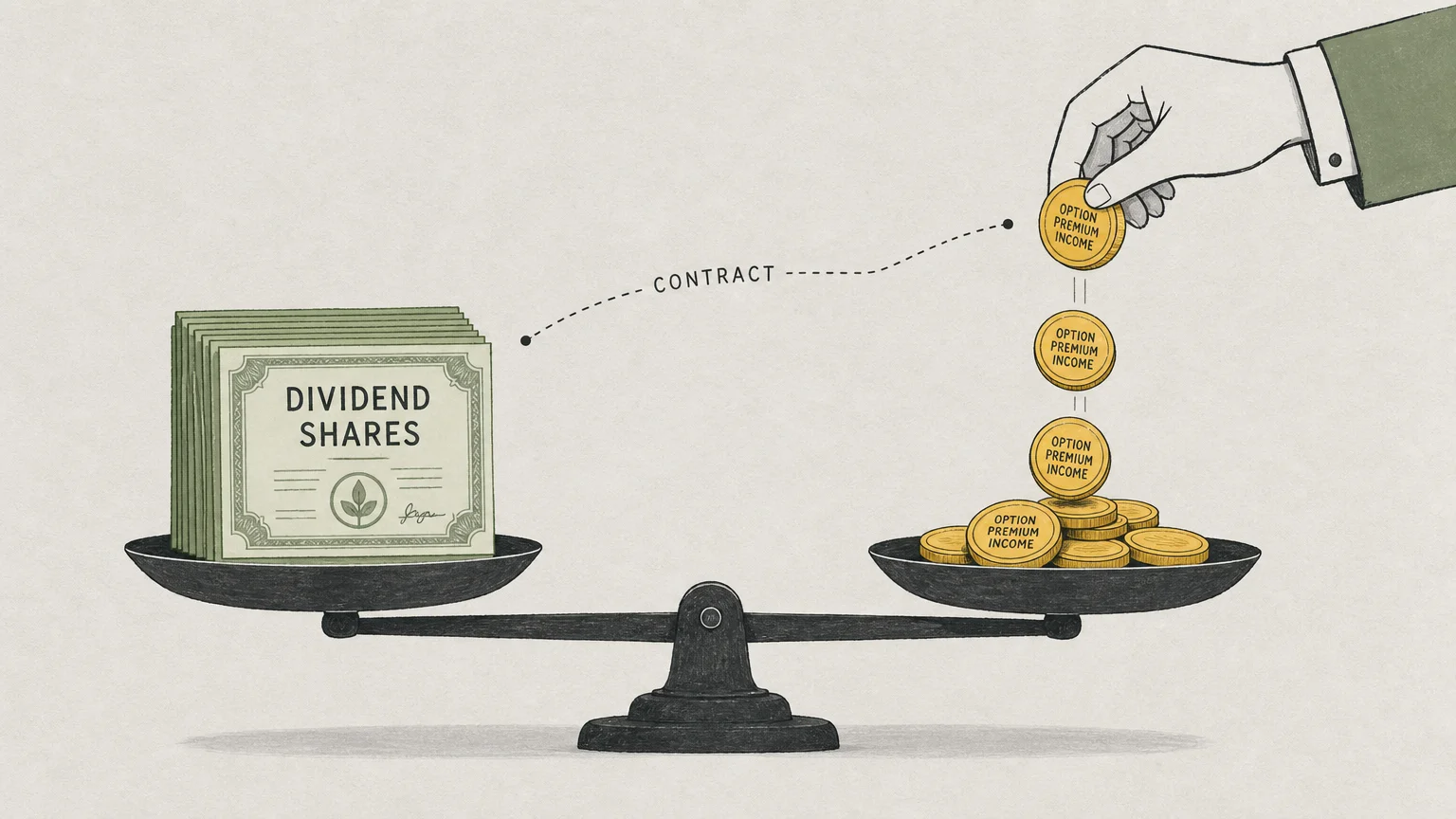

Options trading terrifies the average retail investor, conjuring stressful images of reckless day traders blowing up their retirement accounts. However, systematically selling covered calls remains an incredibly conservative financial strategy used by institutions to generate immediate, tangible cash flow from the boring blue-chip dividend stocks you already hold. You are simply getting paid a cash premium to grant another trader the right to buy your shares at a specific, higher price within a tightly designated timeframe.

If the targeted stock price goes down or trades sideways during the contract period, the options contract expires entirely worthless. You keep the upfront cash premium in your account, and you retain full, unrestricted ownership of your shares. You can then confidently sell another covered call the very next month. This repetitive dynamic creates a powerful synthetic dividend that actively turbocharges your income diversification without requiring you to buy riskier, high-yield assets.

If the stock price unexpectedly rockets past your agreed-upon strike price, you are legally obligated to sell your shares for a guaranteed, predetermined profit, and you still keep the initial cash premium. Retirees holding massive, stagnant positions in legacy telecommunication or utility companies can utilize this exact technique to squeeze an extra three to five percent yield out of their portfolios annually. It acts as an incredible shock absorber when the broader equity markets refuse to climb.

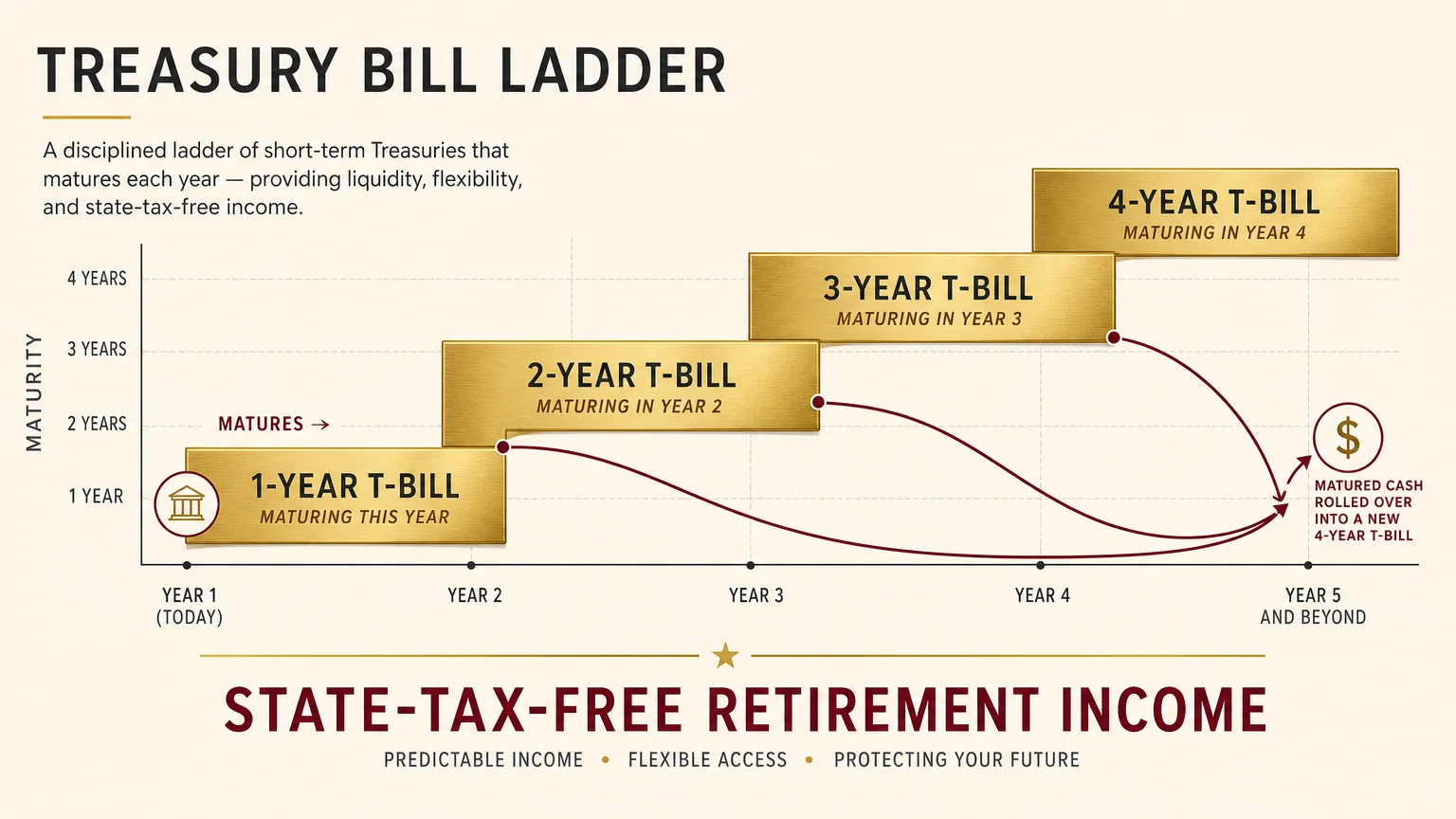

Tip #6: Building State-Tax-Free Treasury Ladders

Leaving excessive amounts of cash languishing in traditional brick-and-mortar savings accounts guarantees you will lose your purchasing power to silent inflation. Even modern online high-yield savings accounts present frustrating risks, as digital banks can aggressively slash their interest rates overnight based on the unpredictable whims of the Federal Reserve. Building a structured ladder of short-term United States Treasury bills locks in attractive yields and establishes an elite level of safety for your baseline retirement cash flow.

Constructing a precise Treasury ladder involves purchasing a series of secure government bonds that mature at strategically staggered intervals—such as three, six, nine, and twelve months into the future. Every time a specific bond reaches maturity, you face a remarkably simple choice. If you require the cash to pay your property taxes or fund a long-awaited vacation, you simply spend the money. If you do not need the liquidity, you automatically reinvest that principal into a brand new bond placed at the furthest end of your ladder.

The primary secret driving this strategy is the massive, undeniable tax advantage. The interest you actively earn on United States Treasury bills remains legally exempt from all state and local income taxes. For retirees living in high-tax jurisdictions, this localized tax exemption makes Treasuries significantly more profitable than standard bank certificates of deposit that offer seemingly identical headline interest rates.

Tip #7: Fractional Commercial Real Estate Investing

You absolutely do not need millions of dollars in capital or the endless headache of answering midnight maintenance calls to earn lucrative real estate income. Fractional commercial real estate investing empowers everyday Americans to purchase small equity shares in massive, institutional-grade properties. You can easily own a profitable slice of a grocery-anchored shopping plaza, a sprawling medical facility, or a massive luxury apartment complex without ever holding a hammer.

Specialized online investing platforms allow you to seamlessly pool your capital alongside thousands of other investors to aggressively fund major commercial developments. The corporate tenants pay their rent, the dedicated property management team handles every stressful operational detail, and you receive your proportional share of the profits deposited directly into your checking account. This clean arrangement entirely divorces your physical time from your earnings, securing the truest and most reliable form of passive retirement income.

Commercial real estate leases typically feature built-in rent escalators that are directly tied to national inflation metrics. This crucial detail means your alternative income naturally and automatically increases as the broader cost of living goes up. Because massive commercial properties generally move independently of daily stock market chaos, this hands-off strategy provides vital income diversification that heavily stabilizes your overall net worth during turbulent economic periods.

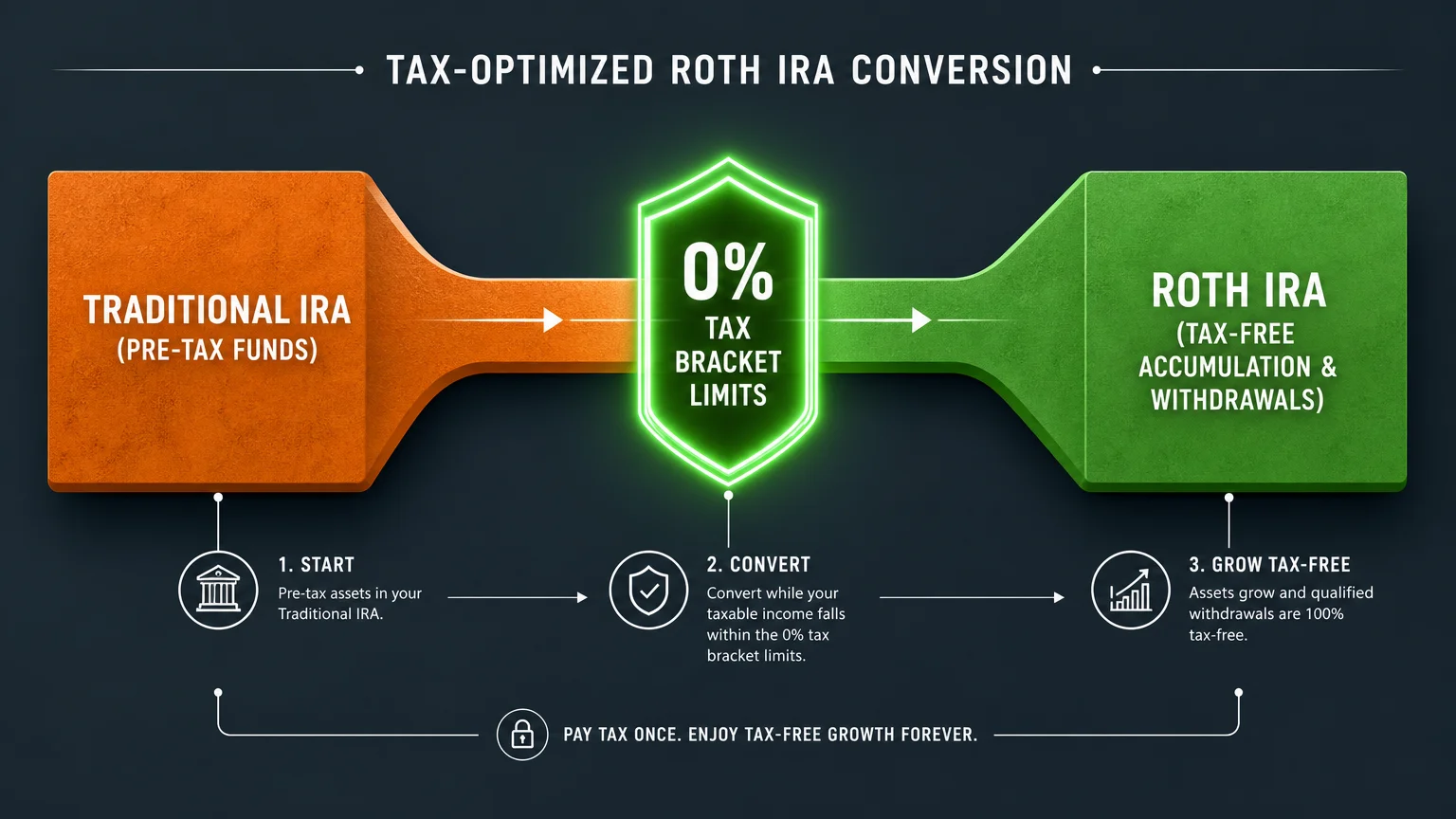

Tip #8: The Zero-Tax Roth Conversion Strategy

Money actively saved from the Internal Revenue Service is mathematically identical to new money earned from a job. Mastering the obscure nuances of the federal tax code serves as the ultimate, high-level hack for permanently increasing your functional retiree finances. During the early phases of retirement—specifically the gap years after you stop working but before you file for Social Security or trigger Required Minimum Distributions—you often drop into a historically low marginal tax bracket.

This narrow, predictable window of time presents the perfect opportunity to execute the zero-tax Roth conversion strategy. By methodically transferring funds from your heavily taxed traditional 401(k) or IRA into a Roth IRA up to the absolute ceiling of your current low tax bracket, you pay a remarkably small amount of upfront income tax. Once those dollars successfully cross the threshold into the protected Roth account, all future compounding growth and all future withdrawals become one hundred percent tax-free.

You are effectively pre-paying your tax obligations at a massive, unrepeatable discount to secure permanent tax immunity for the rest of your natural life. When you reach your late seventies and face predictably steep medical bills or elevated living costs, accessing a massive pool of completely untaxed wealth prevents you from being accidentally pushed into a punitive tax bracket. This strategy defends your capital against future politicians who will inevitably raise tax rates.

The Bottom Line: What This Means for Your Wallet

Securing a comfortable and entirely stress-free retirement requires you to look far beyond the obvious solutions. Traditional pension plans and basic stock market index funds merely form the foundation of your financial house; they are rarely enough to finish the roof. The most successful Americans aggressively utilize every single tool at their disposal to build an impenetrable fortress of sustainable wealth. By exploring these unconventional avenues—from leveraging your hidden home equity and life insurance policies to optimizing your tax brackets and leasing out your physical space—you create a highly resilient web of alternative income.

Do not wait until a severe economic recession wipes out your primary portfolio to start desperately searching for extra cash. Take a comprehensive, unflinching inventory of your assets right now. Identify the dormant financial accounts, the empty storage spaces, and the hidden tax advantages you currently ignore. Taking immediate, decisive action to broaden your income diversification ensures your retirement cash flow remains fiercely robust, regardless of what the unpredictable global economy throws your way.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Frequently Asked Questions

What is the safest alternative income source for a new retiree?

Building a staggered ladder of United States Treasury bills is widely considered the safest cash-generating strategy available. Because the federal government fully backs these bonds, the risk of default remains virtually nonexistent. Furthermore, the complete exemption from state and local income taxes provides a guaranteed, mathematical boost to your real-world returns.

Does earning passive retirement income negatively affect my Social Security benefits?

It depends entirely on exactly how the Internal Revenue Service classifies the specific income. Standard W-2 wages from a part-time job can trigger the Social Security earnings test and severely reduce your monthly benefits if you claim before reaching your full retirement age. However, truly passive revenue streams—such as real estate rental profits, corporate stock dividends, and covered call options premiums—do not count toward the restrictive earnings limit.

How much of my overall cash flow should come from non-traditional sources?

There is no absolute universal percentage, but elite financial planners typically suggest that covering your basic, mandatory living expenses with guaranteed or highly stable alternative income allows you to take calculated, profitable risks with your remaining investment portfolio. Aiming for at least twenty to thirty percent of your total cash flow to stem from diversified, non-market sources drastically reduces your sequence of returns risk during major stock market crashes.

Leave a Reply