Introduction: A No-Nonsense Guide to The $50-a-Week Grocery Challenge

Grocery inflation has aggressively outpaced wage growth and fixed-income adjustments over the past several years. When a standard trip to the supermarket costs upwards of $100 for a handful of bags, surviving on a tight food budget seems impossible. Yet, a specific demographic is quietly mastering the art of the hyper-efficient kitchen. You can learn exactly how to drastically slash your food costs by studying the 50 dollar grocery seniors who thrive on fixed incomes without sacrificing nutrition or flavor. The secret isn’t starvation—it is strategic allocation.

Taking control of your food expenses remains one of the fastest ways to free up cash flow. You cannot control your fixed mortgage rate or utility base charges, but you have absolute authority over what goes into your shopping cart. Lowering your food costs immediately translates to more money available for paying down high-interest debt, building an emergency fund, or investing for your future. This guide breaks down exactly how older Americans are conquering the cheap grocery challenge and how you can apply their battle-tested tactics to your own life.

We are going to dissect seven non-negotiable financial habits that make a $50 weekly grocery budget a reality. These strategies require discipline, intentionality, and a willingness to break away from modern consumer habits. If you implement these seven steps, you will transform your grocery shopping from a weekly financial drain into a predictable, manageable expense.

Financial Habit #1: Mastering the Inventory-First Method

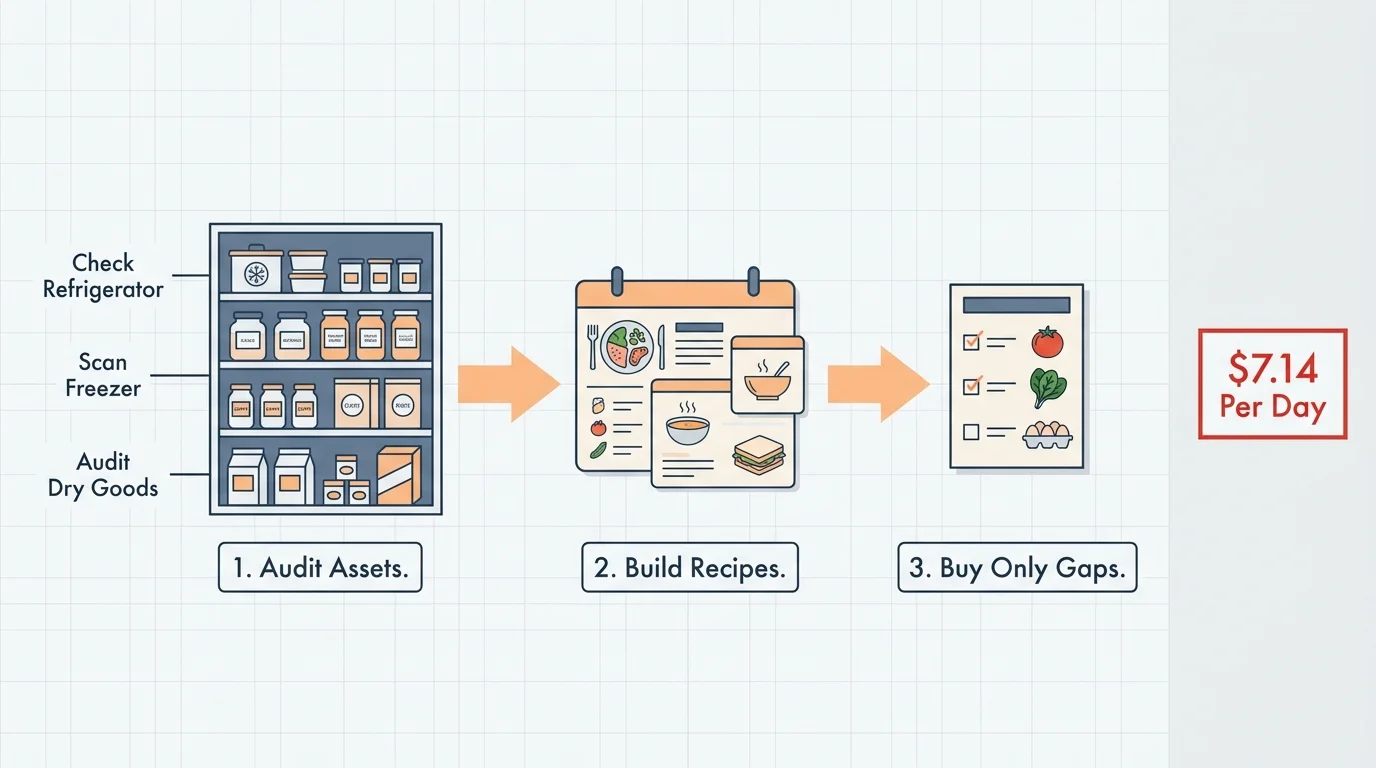

Most Americans plan their meals by deciding what sounds good, finding a recipe, and then driving to the store to buy the ingredients. This approach guarantees overspending. Extreme frugal seniors operate entirely in reverse; they shop their own pantries before they ever step foot in a supermarket. The inventory-first method demands that you know exactly what you already own and build your weekly diet around those existing assets.

Before you write a grocery list, you must audit your refrigerator, freezer, and dry goods shelves. If you discover a half-empty bag of lentils, two chicken thighs in the freezer, and a few wilting carrots, those items become the non-negotiable foundation of your upcoming meals. You only buy the missing components required to turn your existing inventory into complete dishes. If you spend $50 a week, you are operating on $7.14 per day for food. You cannot afford to buy what you already possess; wasting food means wasting cash.

Maintaining a visible inventory also prevents the insidious trap of duplicate buying. Buying a second jar of peanut butter or another box of pasta because you forgot you had one hiding in the back of the cupboard drains your micro-budget. Create a simple paper ledger taped to your pantry door. Track your high-calorie staples. When you treat your kitchen like a commercial restaurant that tracks inventory with ruthless precision, your weekly spending plummets.

Financial Habit #2: Strategic Loss Leader Exploitation

Supermarkets do not price items randomly. They heavily discount specific products—known as loss leaders—to lure you into the store, fully expecting you to buy highly marked-up items while you are there. Smart shoppers flip this dynamic. They buy the deeply discounted meat, eggs, or produce and outright refuse to purchase the profitable center-aisle items the store wants them to buy.

To succeed at this, you must analyze the weekly store circulars before you plan your shopping trip. If the local grocer features bone-in chicken thighs for $0.99 a pound, chicken becomes your primary protein for the week. If pork shoulder is on sale for $1.49 a pound, you pivot to pork. You never pay full retail price for your dietary anchors. You build your menu around what the store is virtually giving away.

Operating this way requires flexibility. You cannot be rigidly attached to eating beef on Tuesday if beef is currently $7.00 a pound. You adapt to the market. By cherry-picking the absolute best deals across two or three local grocers—provided they are within a short driving distance to avoid negating your savings with gas costs—you force your average cost per calorie down to rock bottom. This strategy alone can shave 30 percent off a standard grocery bill.

Financial Habit #3: Embracing Plant-Based Proteins and Alternate Cuts

Meat is consistently the most expensive line item in any grocery budget. If you insist on buying boneless, skinless chicken breasts and premium steaks, you will obliterate a $50 limit by Wednesday. You must rely on high-yield, low budget food staples to stretch your dollars. Beans, lentils, eggs, and canned fish deliver substantial nutrition at a fraction of the cost of fresh butchered meat.

Consider the stark mathematics of protein economics. A pound of ground beef might cost $6.00 and yield roughly four servings. A pound of dried black beans costs approximately $1.50, expands to three times its volume when cooked, and yields six to eight servings. By simply substituting beans for meat in three dinners a week—think black bean tacos, lentil stew, or chickpea curry—you instantly reclaim a massive portion of your weekly budget.

When you do purchase meat, you must learn to utilize alternate cuts. Bone-in, skin-on chicken costs significantly less than its processed counterparts, and the leftover bones provide the foundation for nutrient-dense homemade broths. Tougher cuts of beef or pork, when cooked low and slow in a slow cooker, become incredibly tender and flavorful. You pay a premium for convenience; taking the time to process whole foods yourself keeps your money in your bank account.

Financial Habit #4: Utilizing Senior Discount Days and Loyalty Programs

Leaving money on the table is a cardinal sin of personal finance. Many regional and national grocery chains offer dedicated senior discount days—typically falling on a Tuesday or Wednesday—where shoppers over a certain age receive 5 to 10 percent off their entire purchase. Ten percent might not sound life-changing, but it drastically impacts a tight budget. Saving $5 on a $50 trip equals $260 a year; that is more than a full month of free groceries.

Younger shoppers can mimic this aggressive discounting by fiercely maximizing digital coupons and store loyalty apps. Grocery stores have shifted their best deals away from physical paper clippings and onto their proprietary mobile applications. You must download the app for your local store and load the digital coupons before you shop. Often, stores offer “digital only” pricing that slashes the cost of staples by 50 percent.

You must compound these savings. Combine a store sale with a digital coupon, and if applicable, use a cash-back credit card that offers 5 percent back on grocery purchases—provided you pay the balance in full every single month. Stacking discounts requires zero heavy lifting but demands organizational discipline. When you combine every available promotion, you buy premium food at generic prices.

Financial Habit #5: Mastering Component Batch Cooking

Meal prepping is a popular concept, but preparing five identical containers of chicken and broccoli often leads to palate fatigue and eventual food waste. Component batch cooking is the superior alternative. Instead of cooking entire finished meals, you prepare large batches of versatile base ingredients that you can rapidly combine into different flavor profiles throughout the week.

For example, you might cook a massive pot of brown rice, bake a tray of seasoned chicken thighs, and roast a large pan of root vegetables on a Sunday afternoon. On Monday, you combine the chicken and rice with soy sauce and frozen peas for a quick stir-fry. On Tuesday, you shred the chicken over the roasted vegetables with a vinaigrette dressing. On Wednesday, you mix the rice with black beans and salsa for a burrito bowl. This variety keeps you satisfied while leveraging deep meal plan savings.

Component cooking also guarantees zero waste. When you view your food as modular building blocks, you never let leftovers spoil. A leftover baked potato becomes Wednesday morning’s hash browns; a remnant of Sunday’s roast becomes Monday’s sandwich meat. You extract maximum caloric value from every single dollar you spend.

Financial Habit #6: Pivoting to Frozen Produce

A common myth suggests that eating cheaply means eating unhealthily. Many assume that fresh produce is too expensive for a $50 weekly budget. The mistake lies in buying fresh produce out of season and paying heavy premiums for cross-country shipping. Frozen vegetables and fruits are the ultimate budget-friendly nutritional hack.

Frozen produce is harvested at peak ripeness and flash-frozen immediately, locking in the nutrient density. In many cases, frozen broccoli or frozen berries contain more vitamins than their “fresh” counterparts that have spent two weeks degrading on a transport truck. More importantly, frozen produce costs a fraction of the fresh equivalent and carries zero risk of spoiling in your crisper drawer.

If fresh strawberries are $6 for a small plastic clamshell in January, you skip them. You buy a large bag of frozen mixed berries for $3 and use them in your morning oatmeal or smoothies. You rely on frozen spinach for your eggs and frozen green beans for your dinner sides. You only buy fresh produce when it is hyper-local, deeply in season, and aggressively on sale. This pivot guarantees your diet remains nutrient-rich without fracturing your budget.

Financial Habit #7: Sticking to a Ruthless Cash Envelope System

Financial discipline heavily relies on psychology. Swiping a plastic card distances your brain from the reality of the transaction; handing over physical paper money registers as a genuine loss. To enforce strict adherence to the $50 limit, you must embrace the cash envelope system. You walk into the supermarket with a single $50 bill and leave your debit and credit cards locked in the glovebox of your car.

When you only have a physical $50 bill, you are forced to actively calculate your total as you walk the aisles. You round up prices, you add in estimated local taxes, and you weigh the utility of every item. If you reach the checkout counter and the register rings up $53, you cannot shrug and swipe a card. You must look the cashier in the eye, hand an item back, and stay under your hard limit. That friction is entirely the point.

This forced constraint breaks the habit of impulse buying. The bag of brand-name chips or the expensive pre-made dessert suddenly loses its appeal when you realize buying it means you cannot afford eggs for the week. The cash-only rule enforces a level of ruthless prioritization that transforms casual shoppers into highly calculated budgeters.

The Big Picture: How This Affects Your Financial Future

Trimming your grocery bill to $50 a week is not merely about surviving; it is a defensive wealth-building maneuver. The United States Department of Agriculture estimates that the average single adult spends between $350 and $400 a month on groceries. By dropping your cost to $200 a month, you instantly generate up to $200 in free cash flow every single thirty days.

That $200 a month equates to $2,400 a year. If you redirect those savings to attack a high-interest credit card balance, you save hundreds more in avoided interest. If you invest that $2,400 annually into a simple S&P 500 index fund earning a historical average return, those grocery savings compound into tens of thousands of dollars over a decade or two. You are literally eating your wealth when you overspend at the supermarket.

Financial independence requires you to widen the gap between what you earn and what you spend. Mastering this challenge proves that you do not need to wait for a raise or a windfall to improve your financial footing. You have the power to create your own economic margin today by simply changing how you feed yourself.

Frequently Asked Questions

Is $50 a week actually realistic in today’s inflationary environment?

Yes; however, it requires a complete shift in dietary habits. You cannot buy pre-packaged convenience foods, premium meat cuts, or out-of-season produce. You must center your diet around cheap staples like rice, oats, beans, eggs, and seasonal sales. It demands cooking from scratch, aggressive couponing, and zero food waste. It is entirely possible, but it requires effort.

How do I balance getting enough protein with a strict low-cost grocery budget?

You must look beyond the meat counter. Eggs remain one of the cheapest and most bioavailable protein sources on the market. Canned tuna, sardines, dry lentils, chickpeas, and peanut butter are all incredibly dense in protein per dollar. When you do buy meat, look for clearance manager specials—meat that is near its sell-by date—and freeze it immediately upon returning home.

What if I live in a high-cost-of-living area where everything is more expensive?

Your base prices will be higher, meaning your $50 might buy less volume than it would in the Midwest. In these areas, you must rely heavier on bulk purchasing. Buy massive bags of rice and dried beans from warehouse clubs or international markets where the price-per-ounce is radically lower than traditional supermarkets. You may need to adjust your target to $60 a week, but the foundational principles of inventory tracking, component cooking, and avoiding convenience foods remain exactly the same.

For official information on consumer finance and debt, consult the CFPB. Tax information is available from the IRS. For investment basics, refer to the U.S. SEC.

Disclaimer: This article provides informational content and personal opinions, not professional financial advice. Consult a certified financial advisor for guidance tailored to your specific situation.

Leave a Reply