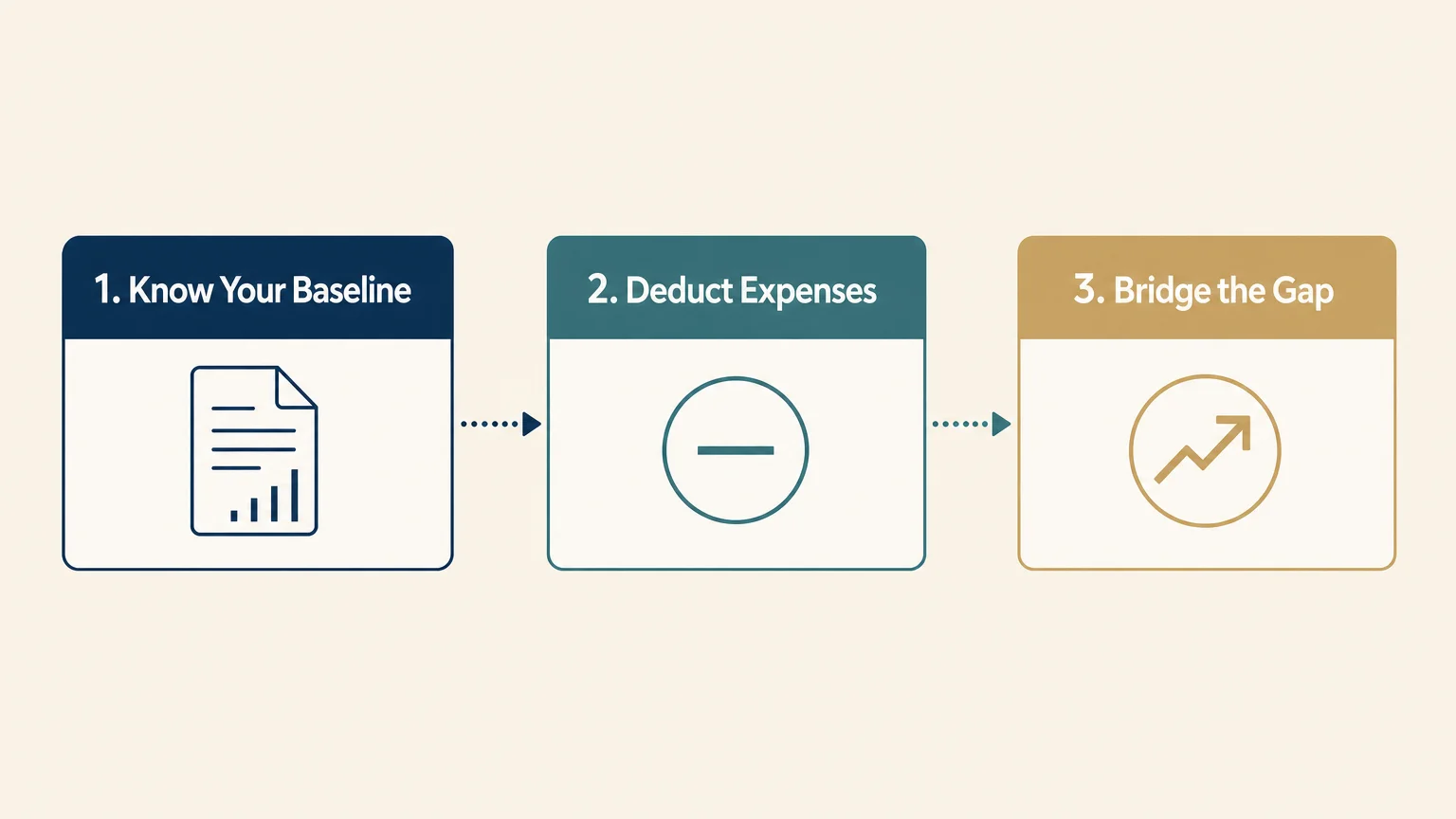

Millions of Americans ask if they can survive on a standard Social Security check, and the brutal truth is that relying on it alone guarantees a financial struggle. The average monthly payout in 2026 hovers around $2,081, which is barely enough to cover basic housing, food, and utilities in most states. If you expect the federal system to fully fund your golden years, you are walking into a dangerous trap. Understanding the massive gap between government benefits and real-world living expenses is the very first step to protecting your retirement. You need aggressive strategies to maximize your total payout, minimize the taxes draining your check, and bridge your income shortfall before it is too late.

Tip #1: Know Your Real Numbers (Not Just the Averages)

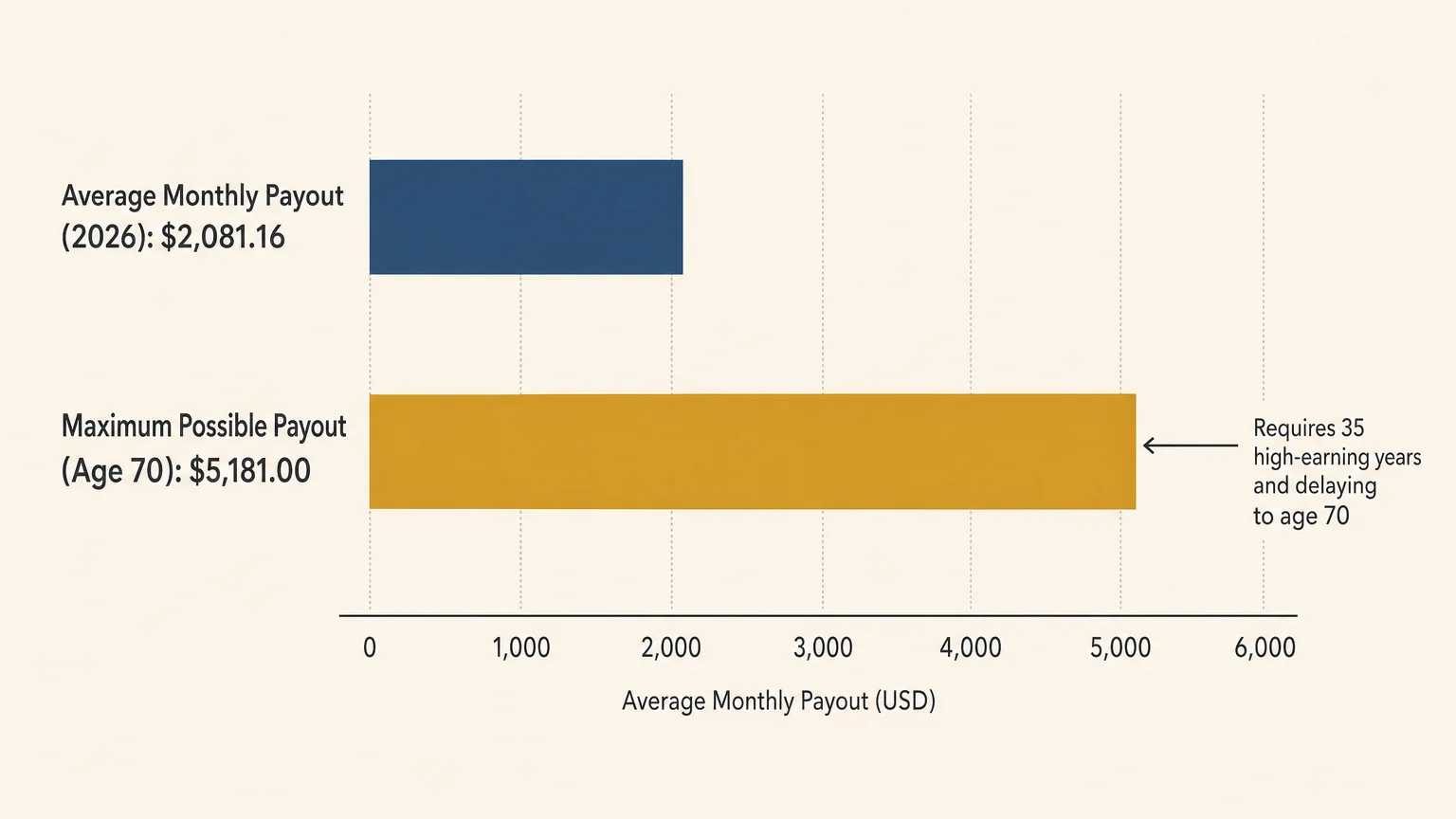

To figure out if you are getting enough, you first need to stop looking at national averages and start looking at your specific earnings record. The Social Security Administration reported that the average monthly check for retired workers hit $2,081.16 in April 2026. If you blindly assume you will receive something close to that amount, you are gambling with your financial future. Your actual payout is calculated based on your 35 highest-earning years indexed for inflation. If you worked for only 25 years, the government formula plugs in zero for the remaining ten years. Those zeroes will drag down your primary insurance amount like a heavy anchor. You need to log into the official government portal, pull your statements, and verify your earnings history today. Do not wait until you are 61 to discover that a clerical error in 1998 erased three years of your highest wages. Finding out your precise baseline allows you to calculate the exact gap between your guaranteed income and your projected living expenses. The maximum benefit in 2026 caps at a robust $5,181 for those who wait until age 70 and earned past the taxable wage base for 35 years. Most Americans will never see that maximum number; therefore, you must aggressively manage the numbers you actually have. Self-employed individuals are notoriously guilty of aggressively writing off business expenses to lower their tax bills, completely forgetting that this directly reduces their future Social Security payout. Knowing exactly what the government owes you empowers you to make surgical adjustments to your savings rate right now.

Tip #2: Calculate the Medicare Premium Bite

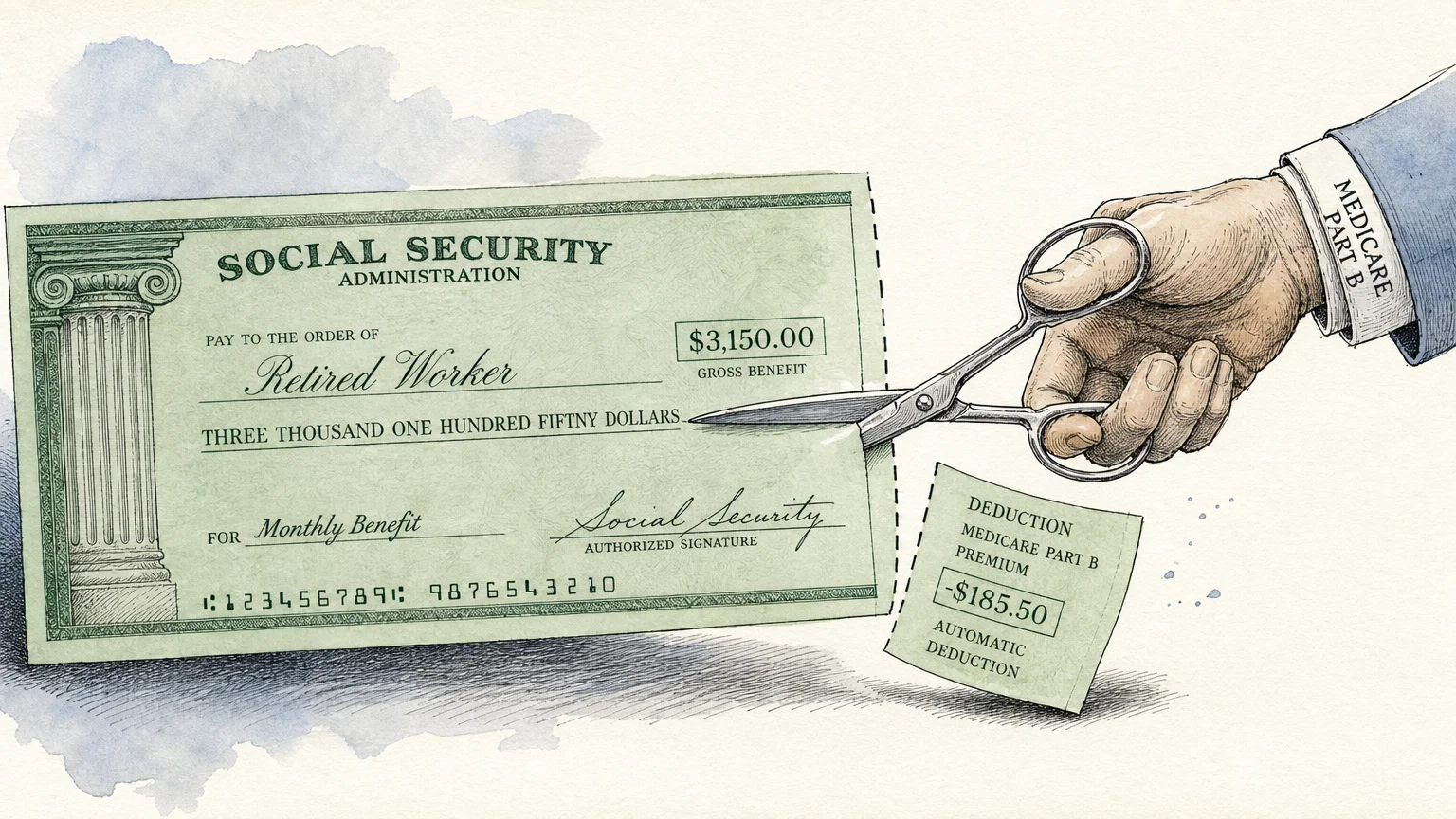

Your gross Social Security check is merely an illusion because the government takes a significant cut before the money ever hits your bank account. The most substantial silent drain on your benefits is Medicare Part B. In 2026, retirees received a 2.8 percent cost-of-living adjustment. While that sounds like a helpful raise on paper, rising Medicare premiums instantly cannibalized a huge chunk of that extra cash for millions of seniors. The standard Part B premium is deducted automatically from your monthly benefit. If your income was unusually high in previous years, you might also be slammed with the Income-Related Monthly Adjustment Amount. This hidden surcharge can easily double or triple your Part B costs and dramatically shrink your net payout. Furthermore, while the federal hold harmless provision prevents your Medicare premiums from reducing your net check below the previous year’s amount, it does not protect your overall purchasing power against rampant inflation. Your check might technically stay the exact same, but your grocery bill certainly will not. You must meticulously budget based on your net income, not your gross award. A $2,000 gross check often drops below $1,800 once premiums and standard deductions apply. Planning your retirement lifestyle around the gross number is a rookie mistake that will leave you desperately scrambling to cover basic utility bills by the middle of the month. You have to forecast your actual cash flow and prepare for the reality that healthcare costs will grow much faster than your annual cost-of-living adjustments.

Tip #3: Factor in the Sneaky Taxes on Your Benefits

Most retirees wrongly assume that Social Security income is completely tax-free. The brutal reality is that the federal government can tax up to 85 percent of your benefits if your total income pushes past an outdated and highly punitive threshold. The IRS calculates your provisional income by taking your adjusted gross income, adding any nontaxable interest you earned, and tacking on exactly half of your Social Security benefits. If you are a single filer and that final number exceeds $25,000—or $32,000 for married couples filing jointly—you owe taxes. These thresholds were established in the 1980s and have incredibly never been adjusted for inflation. Decades of cost-of-living adjustments and wage growth have naturally pushed millions of frugal Americans straight into these taxable brackets. This stealth tax actively penalizes you for saving responsibly and building other income streams. To fight back against this trap, you need a highly tax-efficient withdrawal strategy. Pulling money from traditional IRAs or 401(k) accounts increases your provisional income and immediately triggers the tax bomb on your benefits. Conversely, qualified withdrawals from a Roth IRA do not count toward this specific IRS calculation. By deliberately shifting your assets into Roth accounts before you officially claim Social Security, you can keep your provisional income artificially low. This legal tax shelter shields your hard-earned benefits from the IRS and keeps substantially more money in your pocket where it belongs. Do not let poor tax planning rob you of the payout you spent forty years earning.

Tip #4: Leverage the Delay Strategy for a Guaranteed Return

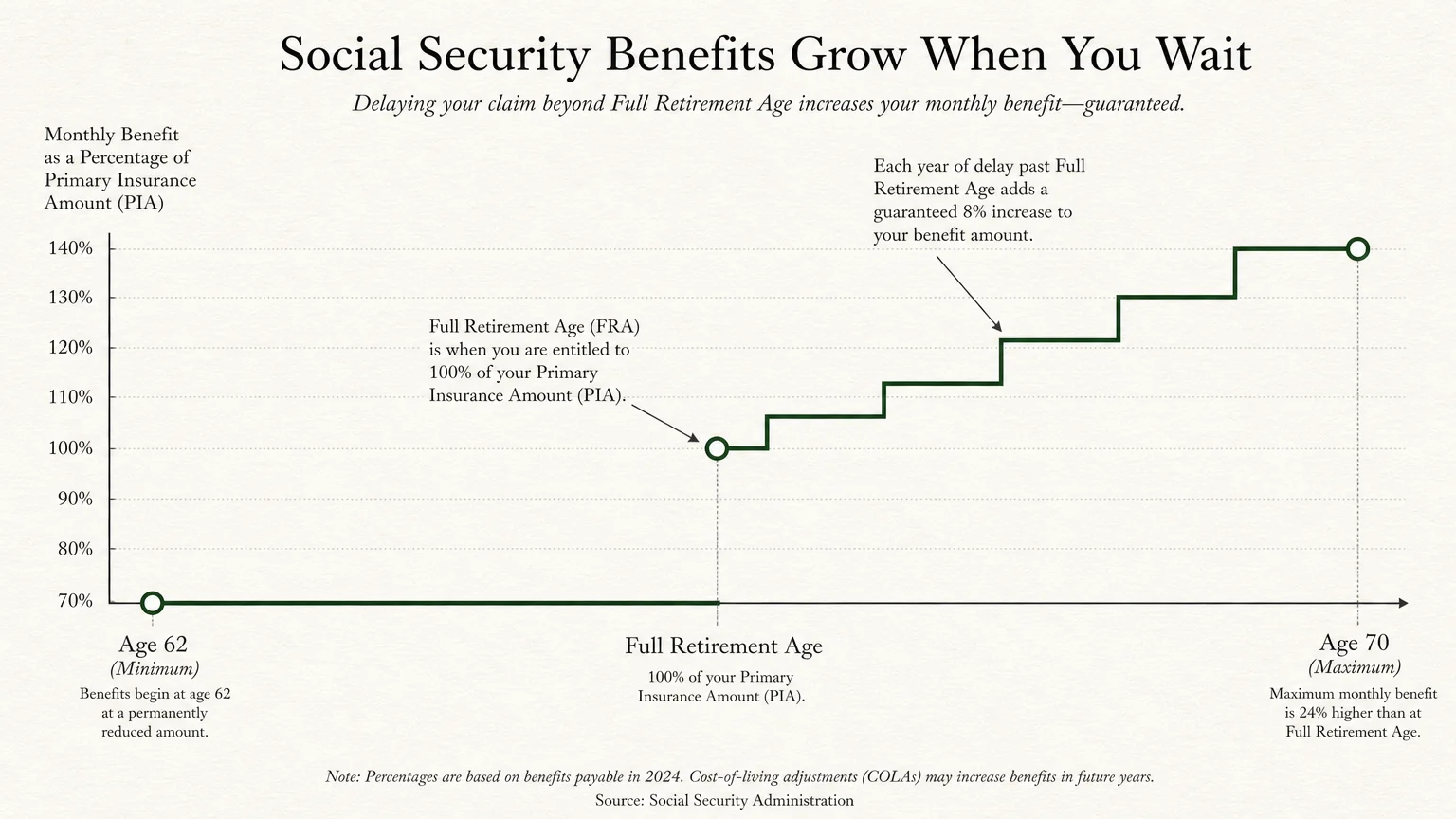

Claiming Social Security is arguably the most consequential financial decision you will make in your sixties. The system allows you to claim as early as age 62, but doing so permanently slashes your monthly payout by up to 30 percent compared to your full retirement age. Too many Americans file early out of a misguided fear that the system will soon go bankrupt. That panic is incredibly expensive. Even if the trust fund is theoretically depleted in the 2030s, ongoing tax revenues collected from active workers would still cover the vast majority of promised benefits. By letting fear drive your filing decision, you voluntarily lock in a poverty-level baseline income for the rest of your life. Instead, you need to treat your benefit like a premier investment vehicle. For every single year you delay claiming past your full retirement age up to age 70, the government guarantees an 8 percent increase in your payout. There is absolutely no stock market index, corporate bond, or insurance annuity on the planet that offers a guaranteed, inflation-adjusted 8 percent annual return. If your health is decent and you have a family history of longevity, delaying is the ultimate financial hack. You essentially purchase the cheapest, highest-yielding longevity insurance available to the public. To successfully bridge the financial gap between age 62 and 70, savvy retirees systematically burn through their taxable investment accounts or secure part-time income first. By depleting other assets while letting Social Security aggressively compound, you ensure a massive, unshrinkable baseline income for your vulnerable later years.

Tip #5: Coordinate Spousal Benefits to Maximize Household Income

Married couples consistently leave tens of thousands of dollars on the table by claiming their individual benefits in isolation rather than coordinating a unified household strategy. The Social Security system provides a unique spousal benefit that allows a lower-earning spouse to claim up to 50 percent of the higher earner’s full retirement age amount. This rule applies even if the lower earner never worked a single day in a traditional job. However, the real financial secret lies entirely in survivor benefits. When one spouse passes away, the household permanently loses the smaller of the two Social Security checks. The surviving spouse automatically gets to keep the larger check. Therefore, maximizing the higher earner’s benefit is not just about getting slightly more money today; it is about fiercely protecting the surviving spouse from financial devastation tomorrow. The primary breadwinner should do everything mathematically possible to delay claiming until age 70 to supercharge that permanent survivor benefit. Furthermore, divorced individuals possess a hidden advantage that few properly utilize. If you were married for at least ten consecutive years and remain currently unmarried, you are legally entitled to claim benefits based directly on your ex-spouse’s earnings record. Your ex-spouse never needs to know, and your private claim does not reduce their payout or the payout of their current spouse in any way. By treating Social Security as a comprehensive household asset rather than a basic individual right, you can strategically sequence your claims to extract the absolute maximum payout from the federal government.

Tip #6: Trim the Fat Off Your Retirement Budget

Because Social Security was fundamentally designed to replace only about 40 percent of your pre-retirement income, trying to maintain your old extravagant lifestyle on a federal stipend is a mathematical impossibility. Frugal Americans inherently understand that reducing daily overhead is significantly easier than generating brand new income in your seventies. You must ruthlessly trim the fat from your retirement budget right now. Start by attacking your absolute largest expense: housing. Holding onto a massive four-bedroom home with crushing property taxes and bloated utility bills is an emotional decision that will financially bleed you dry. Downsizing or utilizing geographic arbitrage—deliberately moving to a state with no income tax and lower property taxes—can instantly free up thousands of dollars in cash flow every single year. Next, attack your unnecessary transportation costs. Maintaining two costly vehicles when you no longer commute daily is literally throwing money into a furnace. Sell the secondary car, dramatically slash your insurance premiums, and bank the routine maintenance savings. You must also aggressively audit your recurring expenses with zero mercy. Cancel the bloated cable packages, drop the expensive whole life insurance policies that no longer serve an actual purpose, and take immediate advantage of every senior discount and property tax exemption your local municipality offers. By shrinking your fixed mandatory expenses to safely match your guaranteed baseline income, you regain total control over your financial life.

Tip #7: Build Supplemental Income Streams That Do Not Penalize You

Since the average government check is rarely enough to comfortably fund a modern lifestyle, securing reliable supplemental income is absolutely non-negotiable. However, if you claim Social Security before reaching your full retirement age and decide to work a traditional part-time job, you will slam right into the dreaded earnings test penalty. In 2026, the Social Security Administration will strictly withhold $1 in benefits for every $2 you earn above the $24,480 limit. While you technically get this money back in the form of a recalculated benefit later, the immediate cash flow crunch can absolutely devastate your budget. The secret is knowing exactly what the government actually considers income. The earnings test only applies to traditional W-2 wages and active net earnings from self-employment. It completely ignores passive income streams. You can generate unlimited cash flow from stock dividends, capital gains, rental properties, corporate pensions, or interest from high-yield savings accounts without triggering a single financial penalty. Savvy retirees intentionally build portfolios specifically designed to yield passive cash flow to seamlessly bridge the gap. Additionally, pulling money from a Roth IRA provides entirely tax-free and penalty-free liquidity that the government cannot legally touch. If you desperately want to keep working, consider transitioning into independent consulting or freelance work where you can aggressively utilize legal business deductions to keep your net active earnings safely below the penalty threshold.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

The Bottom Line: What This Means for Your Wallet

Relying solely on the federal government to fund your retirement is a guaranteed path to permanent financial stress. The stark math is undeniably clear: the average monthly benefit is simply not robust enough to cover the rapidly rising costs of housing, specialized healthcare, and basic daily necessities in 2026. However, you are absolutely not powerless in this challenging equation. By actively managing your earnings record, delaying your claim to guarantee an 8 percent return, legally avoiding stealth taxes, and building penalty-free passive income, you can turn a mediocre government stipend into a powerful financial engine. You must permanently abandon the passive mindset and treat Social Security like a strategic personal asset that requires ruthless optimization. Take absolute control of your monthly budget, eliminate toxic recurring expenses, and systematically use these contrarian strategies to extract maximum value from the federal system you loyally paid into for decades. Your long-term financial security depends entirely on your willingness to plan aggressively and execute relentlessly.

Frequently Asked Questions

Can I survive on Social Security alone?

Surviving on just Social Security is technically possible but practically miserable. With the average 2026 benefit hovering around $2,081, you would be instantly forced into extreme poverty-level budgeting in most major American cities. To mathematically make it work, you must completely eliminate all consumer debt, own your modest home outright, and strategically live in a low-cost geographic area with highly favorable property taxes. Even then, a single unexpected medical bill or major home repair could instantly bankrupt you. You must aggressively build supplemental savings or passive income streams to ensure a genuinely safe, dignified retirement.

Will Social Security run out of money before I retire?

No, the system is not technically going bankrupt, but it is facing a severe and undeniable funding shortfall. The trust funds are currently projected to be fully depleted sometime in the 2030s. If Congress does absolutely nothing to fix the impending issue, the ongoing tax revenue collected from current workers would still be enough to consistently pay out roughly 80 percent of promised benefits. While a 20 percent structural cut would be incredibly painful, the system will not unexpectedly drop to zero. Federal lawmakers have multiple viable tools—like raising the full retirement age or heavily increasing the taxable wage cap—to stabilize the program before that disaster happens.

Does my ex-spouse’s claim affect my own Social Security benefit?

Absolutely not. If you are legally divorced, your strategic decision to claim benefits based on your ex-spouse’s earnings record has zero financial impact on their personal payout. Furthermore, it explicitly does not reduce the benefits of their current spouse if they happen to have remarried. The Social Security Administration handles these claims completely independently and confidentially. You do not even need your ex-spouse’s permission to successfully file, provided you meet the basic federal requirements of being married for at least ten consecutive years and remaining currently unmarried at the time of your application.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply