Traditional retirement planning is dead, and adapting to the 2027 retirement trends dictates whether you outlive your money or live comfortably on your terms. You can no longer rely on outdated rules of thumb to survive the shifting economic outlook. Wall Street wants your nest egg parked in high-fee target-date funds, but savvy savers are exploiting new tax loopholes, dynamic withdrawal strategies, and geographic arbitrage to protect their cash. Future retirement income depends entirely on how aggressively you pivot away from the obsolete pension mindset and embrace modern wealth preservation. The senior finance trends dominating the next decade require immediate action. Delay means leaving massive tax savings and passive income on the table right now.

Trend #1: Phased Retirements Replace the Hard Stop

The concept of working until Friday and sitting on a beach by Monday is over. Employers facing massive brain drain are quietly offering lucrative phased retirement contracts. Instead of quitting outright, you negotiate a reduced schedule—working two days a week while keeping premium healthcare benefits and partial salary. This strategy stretches your portfolio significantly. By covering your baseline living expenses with part-time income, you delay tapping into your traditional retirement accounts or Social Security.

Delaying Social Security until age seventy guarantees an eight percent annual bump in payouts. When you factor in the mathematical advantage of uninterrupted compound interest on your untouched investments, a three-year phased retirement can add hundreds of thousands of dollars to your ultimate net worth.

Employers are desperate to retain specialized talent as demographic cliffs approach. You hold all the negotiating power. Ask for remote work flexibility alongside the phased hours. This allows you to test-drive your retirement lifestyle without entirely severing your primary cash flow.

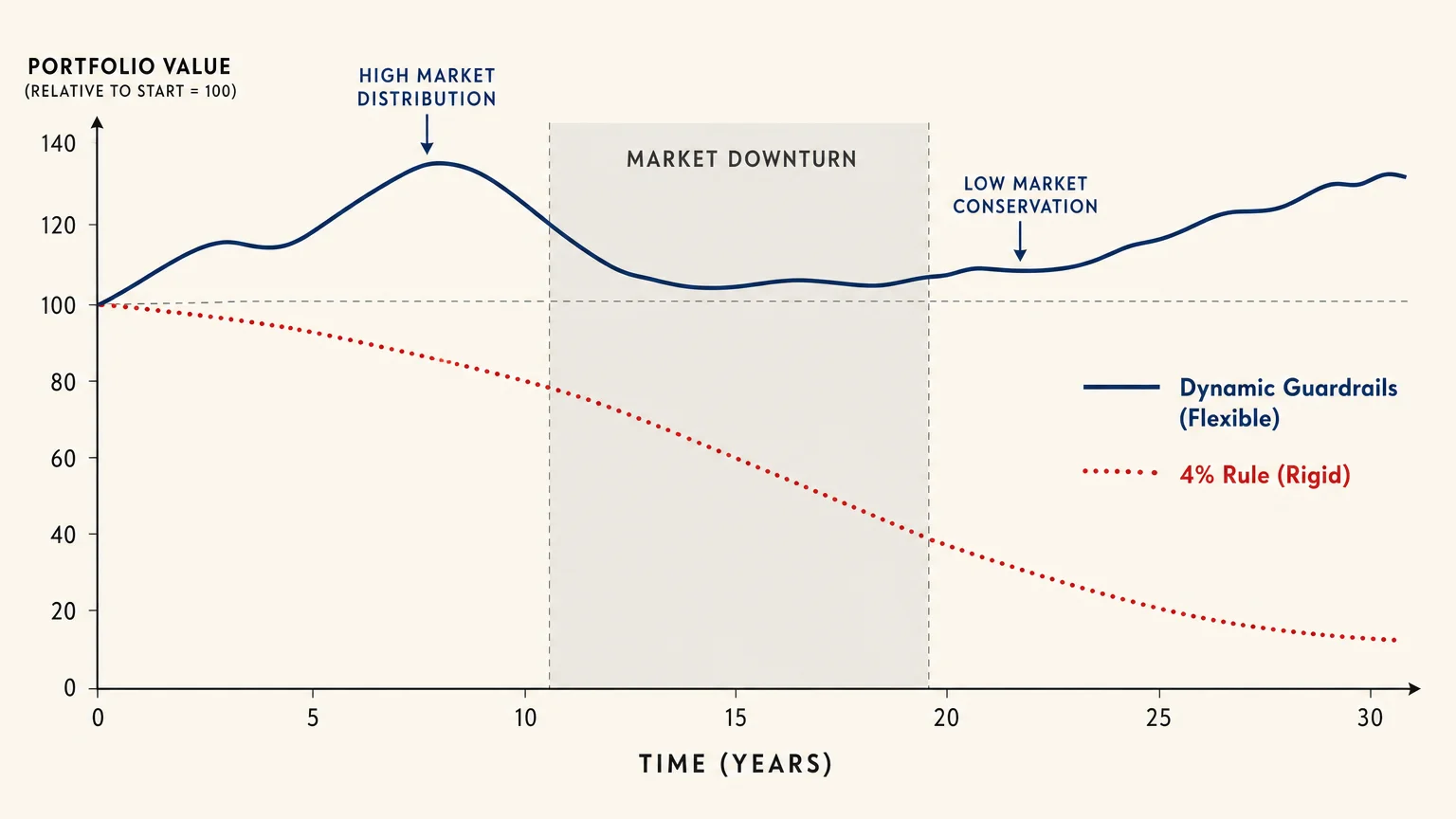

Trend #2: Dynamic Withdrawal Rates Kill the Four Percent Rule

Financial planners have peddled the four percent withdrawal rule for decades. It is mathematically broken for 2027. Market volatility and sticky inflation require a much more agile approach to future retirement income. Enter the dynamic withdrawal strategy. Instead of blindly pulling a fixed percentage out of your accounts every single year, you adjust your distributions based on portfolio performance and market valuations.

When the market hits all-time highs, you take a slightly larger distribution and stash the excess cash in high-yield reserves. When bear markets strike, you tighten your belt, cut discretionary spending, and rely on those cash reserves rather than liquidating stocks at depressed prices. This flexible approach prevents the dreaded sequence of returns risk from destroying your portfolio early in retirement.

Smart retirees are using guardrail strategies—setting strict upper and lower limits on their withdrawal rates—to guarantee they never run out of money. You must ruthlessly track your portfolio’s performance every quarter. Utilizing a guardrail strategy means you never blindly pull out cash when the market is bleeding. This mathematically secures your longevity risk and ensures your money outlives you.

Trend #3: Geographic Arbitrage Hits the Midwest

Retiring to Florida or Arizona is a luxury of the past. Sunbelt real estate prices and catastrophic property insurance premiums have completely destroyed the cost-of-living advantages those states once held. The new geographic arbitrage strategy focuses heavily on the Midwest and the Rust Belt. States like Ohio, Indiana, and Michigan are attracting massive waves of retirees looking to slash their housing costs by sixty percent.

You can sell an average home in a coastal city for a million dollars, buy a massive property in a vibrant midwestern college town for a third of the price, and bank the massive cash difference. This influx of capital immediately turbocharges your investment accounts. Furthermore, these emerging retirement hotspots offer robust healthcare systems tied to major universities, avoiding the notorious specialist shortages plaguing traditional southern retirement communities.

Your location dictates your baseline burn rate more than any other variable. Do not underestimate the power of dropping your property taxes from twenty thousand dollars a year down to three thousand dollars. That immediate savings acts exactly like a massive raise. You can redirect those funds straight into your brokerage accounts.

Trend #4: Health Savings Accounts Become the Ultimate Stealth IRA

Most Americans fundamentally misunderstand the Health Savings Account. They treat it like a checking account for medical copays. By 2027, elite savers treat the HSA exclusively as a stealth retirement account. The HSA offers the ultra-rare triple tax advantage: contributions lower your taxable income, the money grows completely tax-free, and withdrawals for qualified medical expenses are never taxed.

The secret hack is paying for your current medical expenses out of pocket while leaving the HSA funds fully invested in low-cost index funds. Keep your receipts. Years from now, you can reimburse yourself for decades of past medical expenses completely tax-free. Once you hit age sixty-five, the HSA behaves exactly like a traditional IRA for non-medical expenses; you simply pay ordinary income tax without any penalties.

Do not let your HSA sit in a cash position earning zero interest. Log into your provider portal, move the funds into a broad market index fund, and let compound growth do the heavy lifting for the next two decades. Maximizing your HSA contributions and refusing to touch the principal is the most powerful tax-dodging maneuver available to middle-class Americans today.

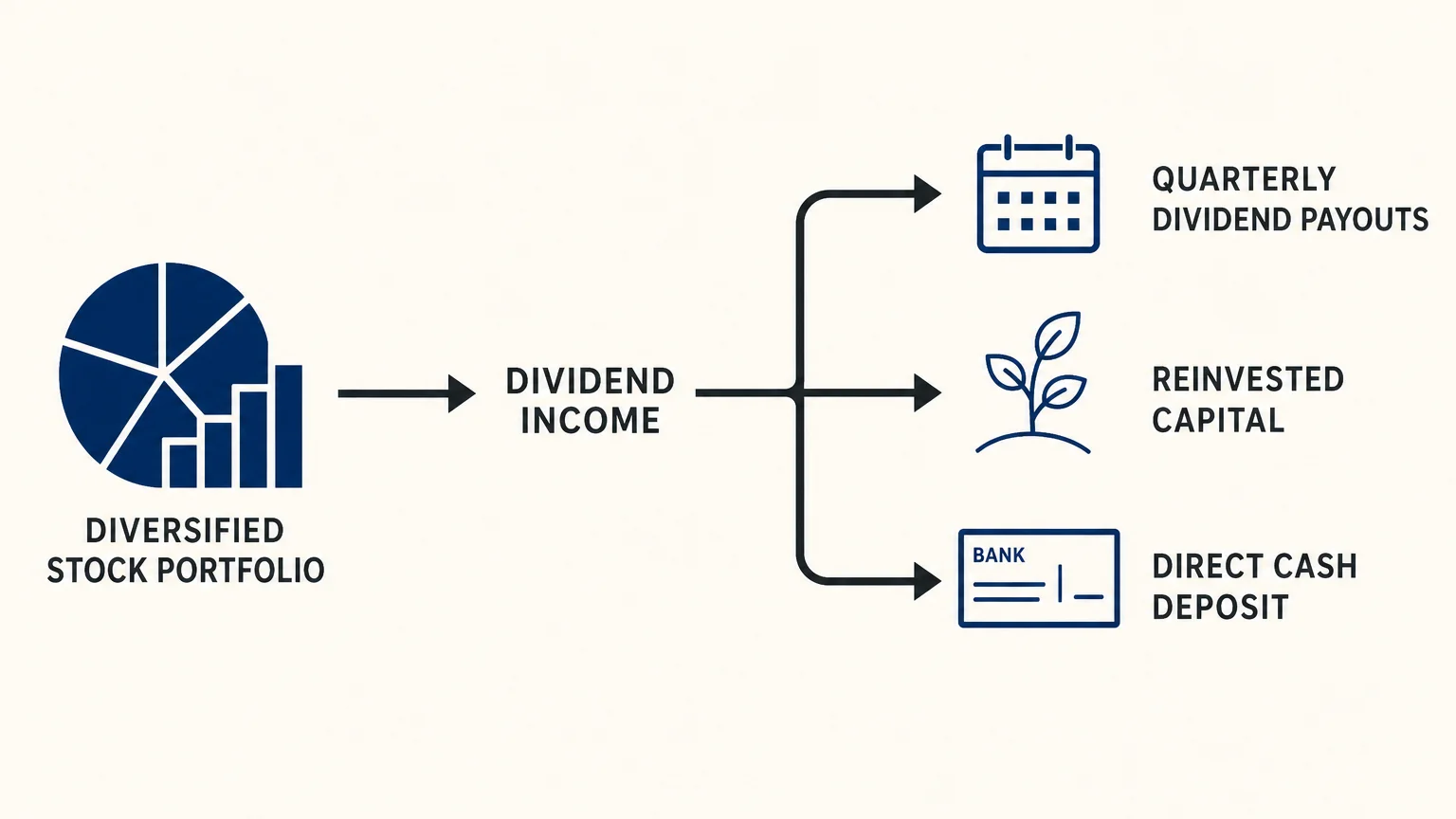

Trend #5: Dividend Harvesting Replaces Fixed Annuities

Insurance companies sell annuities by playing on your fear of outliving your cash, but they trap you in rigid contracts with horrible internal fees. You can build a vastly superior income stream using a diversified dividend harvesting strategy. Modern retirees are abandoning complex insurance products and building portfolios packed with high-quality dividend growth stocks, real estate investment trusts, and business development companies.

You focus entirely on the cash flow generated by the portfolio rather than sweating the daily price fluctuations. Companies with a fifty-year track record of increasing their dividends—often called Dividend Aristocrats—provide a naturally growing income stream that actively fights inflation. While a fixed annuity pays you the exact same dollar amount decades from now when that dollar buys half as much, a properly structured dividend portfolio hands you an organic pay raise every single year.

Stop accepting pathetic yields from traditional savings vehicles. By reinvesting your dividends back into the market during your working years, you build a massive snowball of compounding cash flow that eventually covers every single one of your household bills. You maintain complete control over your principal while enjoying a steady stream of passive cash.

Trend #6: Micro-Consulting and Premium Senior Gig Work

The gig economy is no longer just ride-sharing and food delivery. By 2027, the demand for senior-level gig work is surging. Micro-consulting platforms connect specialized professionals with businesses needing short-term expertise. You can monetize decades of industry experience without committing to a grueling full-time schedule. Engineers, marketing executives, and human resources directors are pulling in hundreds of dollars an hour advising startups on video calls from their living rooms.

This premium gig work fundamentally changes retirement forecasts because it provides immense intellectual stimulation while generating highly lucrative independent contractor income. You can funnel this income into a Solo 401(k), further shielding your earnings from the IRS while supercharging your tax-advantaged savings. You dictate your hours, choose your clients, and ruthlessly protect your time.

You leverage your decades of corporate survival into a highly profitable solo enterprise. Furthermore, the tax deductions available to independent contractors—writing off portions of your internet, phone, and home office—drastically lower your overall taxable footprint. This model turns your accumulated career capital into a highly liquid, on-demand asset class.

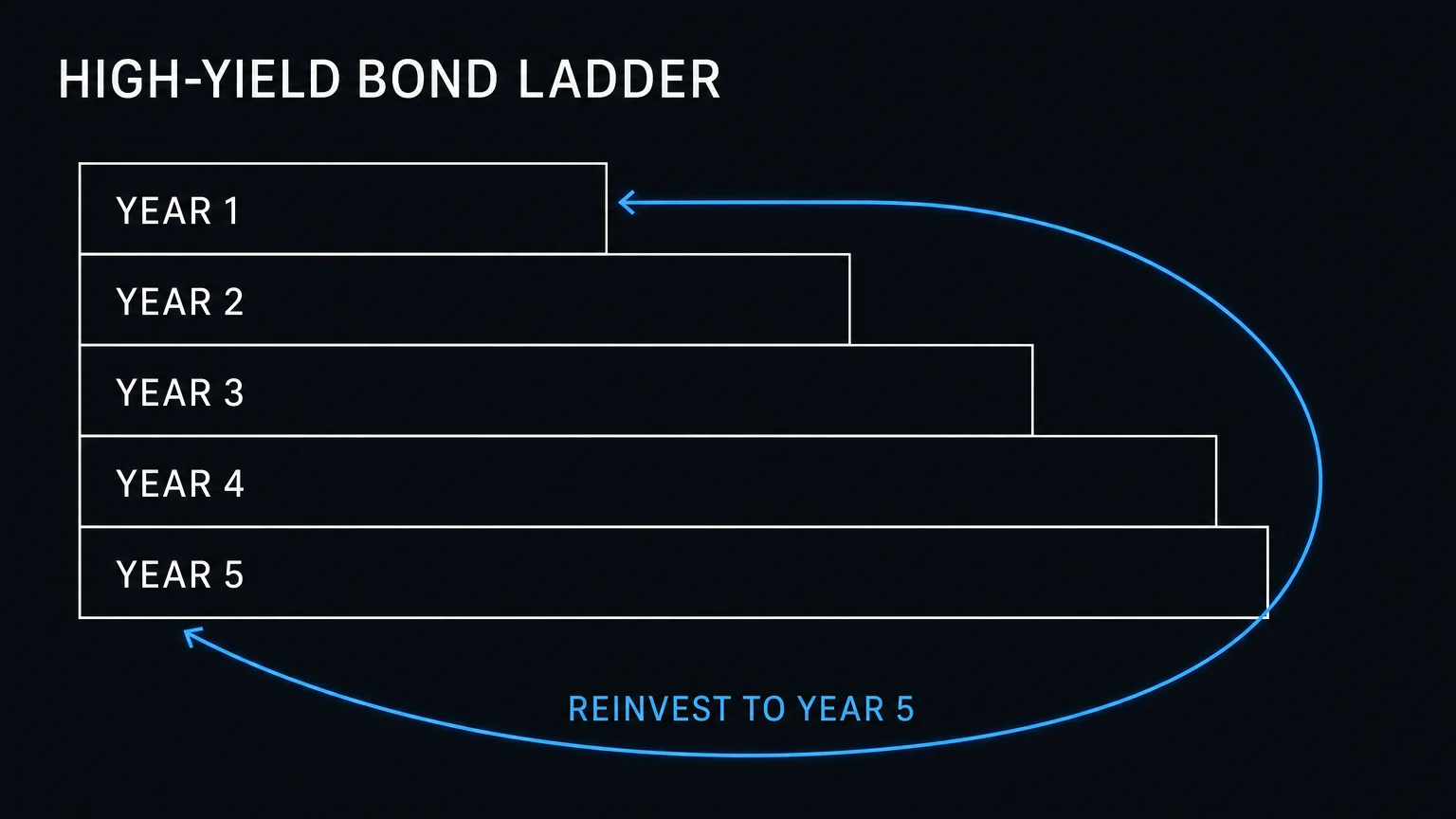

Trend #7: High-Yield Bond Laddering Returns to Dominance

For over a decade, zero-interest-rate policies forced retirees to take massive risks in the stock market just to generate a meager yield. The current economic outlook has flipped this dynamic completely. Bond laddering is back, and it provides a virtually risk-free foundation for your retirement income. A bond ladder involves purchasing a series of Treasury bills or high-grade corporate bonds that mature at different intervals—such as three months, six months, one year, and two years.

As the short-term bonds mature, you collect the principal and interest. If you need the cash for living expenses, you spend it. If you do not need the cash, you reinvest it at the longest end of your ladder. This strategy effectively insulates you from interest rate fluctuations and guarantees that you always have liquid cash maturing exactly when you need it. You completely eliminate the need to sell equities during market crashes.

Stop paying exorbitant management fees to advisors who just stick you in generic bond funds. Building your own ladder using direct Treasury purchases online takes twenty minutes and costs you zero dollars in commission.

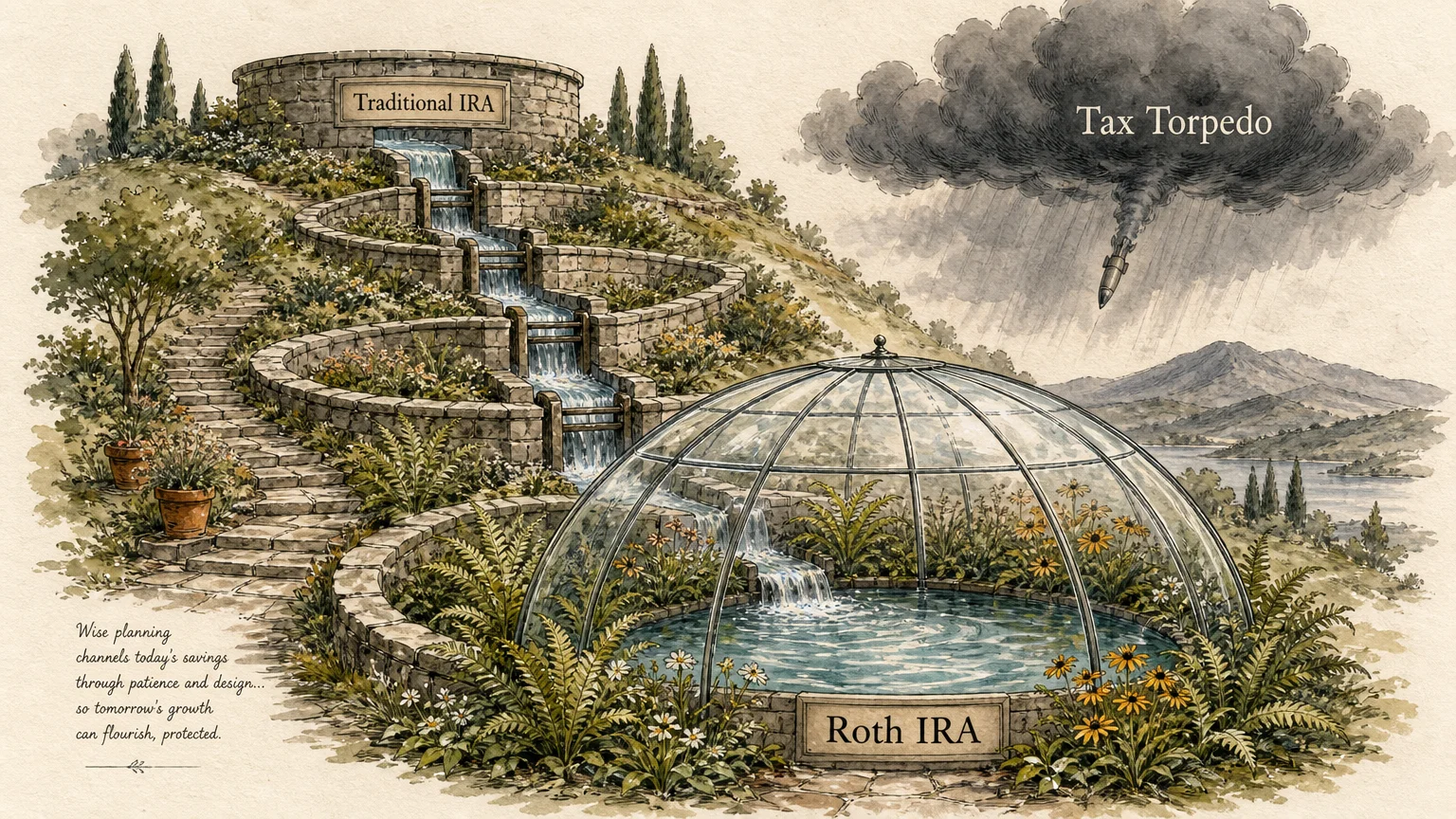

Trend #8: Aggressive Roth Conversion Ladders Dodge the Tax Torpedo

The IRS is sitting on a massive time bomb regarding your traditional retirement accounts. When you hit Required Minimum Distribution age, the government forces you to pull money out of your tax-deferred accounts, frequently pushing you into a much higher tax bracket. This is the dreaded retirement tax torpedo. Savvy investors are neutralizing this threat by executing aggressive Roth conversion ladders during their early retirement years.

When you first stop working, your earned income plummets, temporarily dropping you into a remarkably low tax bracket. You strategically convert portions of your traditional IRA into a Roth IRA up to the top edge of your current low bracket. You pay a small amount of taxes now to guarantee that the money grows tax-free forever.

You must coordinate this strategy meticulously with your accountant to avoid bumping into Medicare premium surcharges. However, executing this perfectly allows you to shift massive amounts of capital out of the government’s reach. Over a five-year period, you ensure that your future withdrawals remain entirely untouchable by federal tax hikes, leaving a massive, entirely tax-free inheritance to your children.

Trend #9: Fractional Real Estate Replaces Traditional Landlording

Being a traditional landlord involves fixing leaking toilets at midnight, dealing with nightmare tenants, and paying exorbitant property management fees. Those headaches contradict the very essence of a peaceful retirement. However, the cash flow from real estate remains essential for robust senior finance trends. The solution for 2027 is fractional real estate investing.

Platforms now allow you to purchase equity shares in commercial properties, apartment complexes, or single-family rental portfolios across the country. You collect your proportionate share of the rental income and property appreciation without ever touching a hammer or screening a renter. This strategy allows for massive diversification; instead of tying up hundreds of thousands of dollars in a single local rental property, you can spread that same capital across dozens of properties in high-growth markets nationwide.

Forget chasing down late rent checks or repairing drywall. Fractional platforms perform all the heavy lifting, analyze the market data, and deposit your distributions directly into your checking account every single quarter. You get all the financial benefits of real estate investing with absolute zero operational friction.

Trend #10: Multi-Generational Co-Housing Cuts Expenses in Half

The nuclear family model is evolving rapidly as housing affordability crumbles. A major trend shaping the late 2020s is the strategic return to multi-generational living, but with a modern architectural twist. Families are pooling their resources to purchase large properties with detached accessory dwelling units or fully separated mother-in-law suites. This arrangement drastically reduces everyone’s baseline living expenses.

You split property taxes, utility bills, and maintenance costs while maintaining total privacy in your own designated living space. Beyond the profound financial savings, this structure offers built-in childcare for your adult children and immediate elder care support for you as you age. Avoiding the astronomical costs of private assisted living facilities can save your estate hundreds of thousands of dollars.

Zoning laws across the country are rapidly changing to encourage accessory dwelling units. Capitalize on this legislative shift by building equity on land you already own, effectively creating a powerful family compound that insulates you from external economic shocks. By consolidating real estate equity across generations, you create an impenetrable financial fortress that benefits the entire family tree.

The Bottom Line: What This Means for Your Wallet

The retirement playbook you were taught twenty years ago is now entirely obsolete. Sticking your head in the sand and trusting a generic mutual fund will not cut it in 2027. The current economic outlook demands a proactive, almost aggressive approach to wealth management. By leveraging these modern tactics—from ruthlessly optimizing your health savings accounts to executing strategic Roth conversions—you legally steal your own money back from the IRS.

Geographic arbitrage allows you to dramatically slash your burn rate overnight, while AI-driven gig work and dividend harvesting guarantee that cash keeps flowing into your accounts long after you stop punching a corporate clock. Stop waiting for the government or Wall Street to save you. Take immediate, absolute control over your financial destiny. Implement these senior finance trends today, restructure your assets for maximum efficiency, and build an unstoppable income engine that thrives in any economic environment.

Frequently Asked Questions

Is the four percent rule completely dead for new retirees?

Yes, blindly following a rigid four percent withdrawal rate is highly dangerous today. Market dynamics and shifting inflation demand flexibility. You must adopt dynamic withdrawal rates that adapt to current portfolio valuations. You take slightly less during market downturns and capture excess gains during bull runs to build your cash buffers.

How late is too late to start a Roth conversion ladder?

It is never mathematically too late until you are forced into Required Minimum Distributions, but the optimal window is between the day you retire and the day you claim Social Security. This period usually represents your lowest lifetime tax bracket. Moving money from traditional accounts to Roth accounts during these gap years minimizes your tax burden and permanently shelters future growth.

Can I really live off dividend harvesting without touching my principal?

Absolutely. A well-constructed portfolio of Dividend Aristocrats, real estate investment trusts, and high-yield bonds can reliably generate four to five percent in annual passive income. If you have a one million dollar portfolio, that is forty to fifty thousand dollars a year in cash flow. You never sell the underlying shares, meaning your original capital remains completely intact while producing endless income.

Do I lose access to premium healthcare if I relocate for geographic arbitrage?

No. The key to modern geographic arbitrage is moving to midwestern university towns, not rural outposts. Cities anchored by major research universities offer world-class healthcare networks and specialized medical facilities that rival any expensive coastal city. You get premium medical care at a fraction of the cost of living.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply