Your path to keeping more of your paycheck starts by challenging the recurring costs draining your bank account. Providers rely on complacency to increase prices, hoping you never call to contest the charges. You can lower monthly bills significantly by speaking with retention specialists. Current economic shifts have made companies desperate to retain loyal customers, giving you unprecedented leverage to negotiate bills and slash household expenses. By applying these frugal living tips to your recurring charges, you instantly create more breathing room in your budget to pay down debt and accelerate your wealth-building goals. Let us examine the specific recurring charges where a brief conversation yields massive long-term savings.

Financial Habit #1: Cable and Internet Service

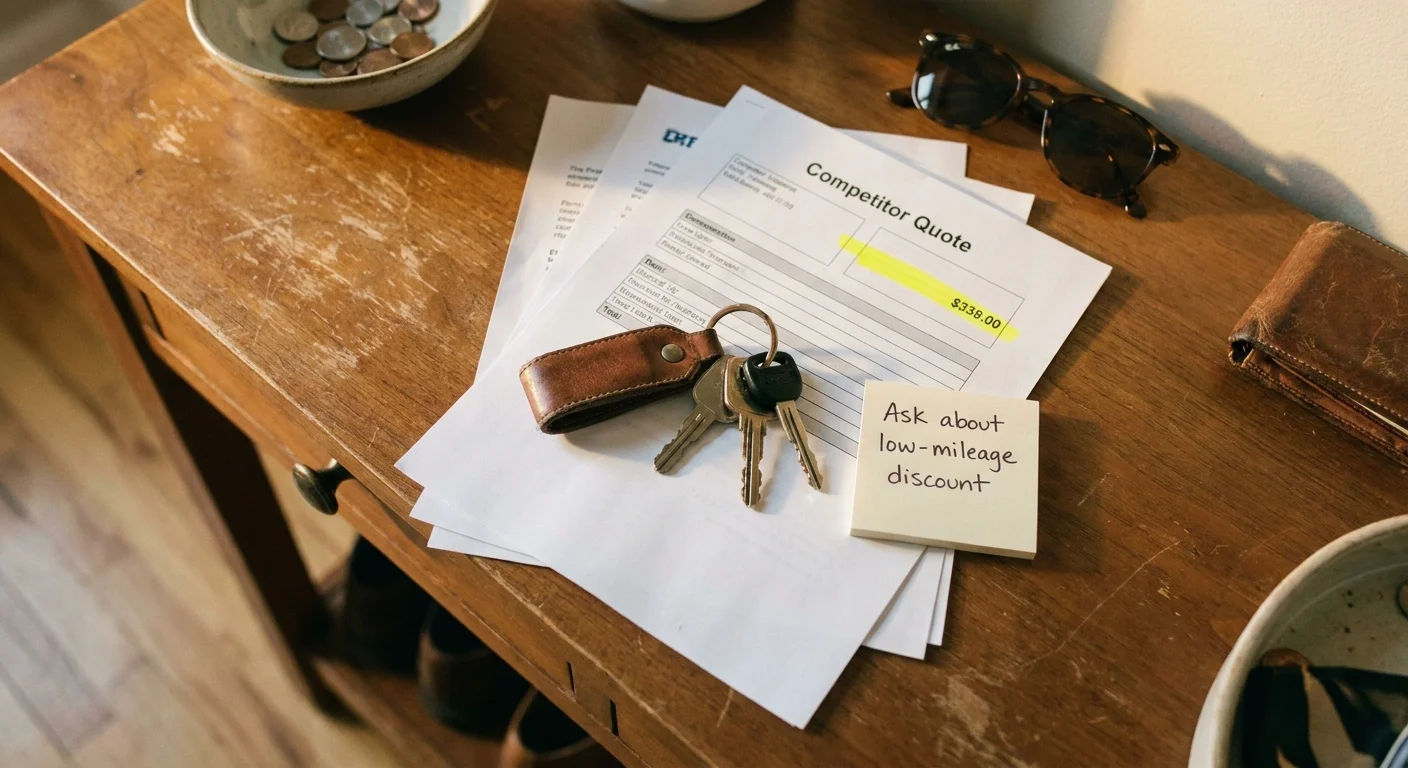

Internet providers rely heavily on introductory pricing models. When your twelve-month promotional rate expires, your bill often skyrockets by forty to sixty percent. You must take proactive steps to reset this rate. Call your provider and immediately request the cancellation or customer retention department—front-line representatives rarely possess the authority to authorize heavy discounts. Inform the retention agent that you received a competitive offer from a rival fiber or wireless home internet provider for fifty dollars a month. Request that they match this rate to keep your business. If they hesitate, politely ask for the cancellation date to be scheduled a week out. Providers typically fold before losing a reliable account, offering a new promotional rate or upgraded speeds at your original price point. Consistently applying this strategy saves the average household over five hundred dollars annually on connectivity costs.

Financial Habit #2: Cell Phone Plans

The telecommunications landscape has shifted dramatically, eliminating the need to pay premium prices for unlimited data. Major carriers disguise their bloated bills with mandatory fees and unnecessary perks like complimentary streaming services you never actually use. You hold immense power to slash this household expense by confronting your current carrier. Start by researching Mobile Virtual Network Operators. These companies lease tower space from the major networks but charge half the price. Armed with a twenty-five-dollar unlimited plan offer from a competitor, call your carrier and demand a better rate. Mention your willingness to port your number immediately. Carriers frequently offer unadvertised loyalty plans or apply permanent monthly credits to your account to prevent churn. If they refuse to budge, make good on your threat and switch. You keep the exact same coverage, allowing you to save money monthly without sacrificing quality.

Financial Habit #3: Auto Insurance Premiums

Loyalty no longer pays in the auto insurance industry. Insurers utilize complex algorithms to identify customers who auto-renew without checking competitor rates, a practice known as price optimization. They slowly increase your premiums over time, assuming you lack the motivation to shop around. To combat this, you must aggressively negotiate your auto insurance at least once a year. Use online comparison tools to gather three quotes from competing agencies. Call your current broker and present the lowest quote. Ask them to review your policy for missing discounts, such as defensive driving course credits, low-annual-mileage reductions, or telematics tracking programs that reward safe driving habits. If your current provider cannot match the competitor rate for identical coverage limits, switch insurers immediately. Maintaining a flawless driving record gives you the ultimate leverage to dictate terms and secure massive reductions on your premium.

Financial Habit #4: Medical Bills and Hospital Debts

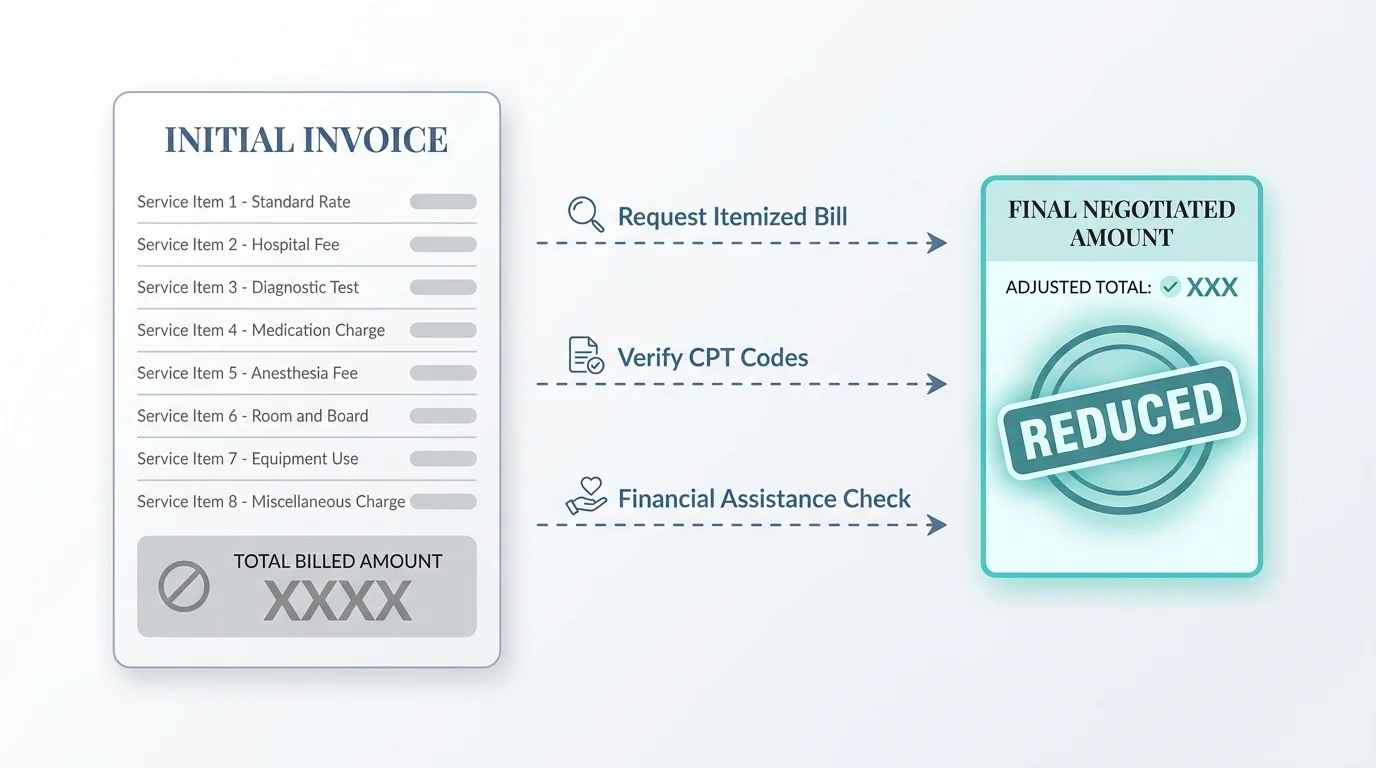

Healthcare costs devastate household budgets, but few Americans realize that medical bills serve as a starting offer rather than a final verdict. Hospitals and clinics routinely inflate charges, knowing insurance companies will negotiate them down. If you face a steep out-of-pocket balance, you possess several avenues to reduce the financial blow. First, demand a fully itemized bill with billing codes. Scrutinize this document for duplicate charges, canceled tests, or upcoded services. Once you verify the actual services rendered, contact the billing department to negotiate a cash-pay discount. Providers often slash a bill by thirty to fifty percent if you agree to settle the balance with a single lump-sum payment. Alternatively, ask about income-driven financial assistance programs or zero-interest payment plans. Medical providers prefer securing a guaranteed reduced amount over sending your account to a collection agency where they recover pennies on the dollar.

Financial Habit #5: Credit Card Interest Rates

Carrying a balance on a credit card incurs punitive interest charges that rapidly destroy your wealth-building potential. With average annual percentage rates soaring past twenty-four percent in 2026, lowering this specific metric remains a critical priority. You do not need to accept the assigned interest rate permanently. Call the number on the back of your credit card and remind the representative of your flawless payment history. Inform them that you hold a balance transfer offer from a competing bank featuring zero percent interest for eighteen months. Ask if they can permanently reduce your current annual percentage rate to keep you from moving your balance. Creditors spend heavily to acquire customers. They will often lower your rate by several percentage points rather than lose your revolving debt to a rival. This five-minute conversation easily saves you hundreds of dollars in compounding interest charges.

Financial Habit #6: Gym and Fitness Memberships

The fitness industry relies on an archaic business model designed to lock you into high monthly fees while hoping you never actually use the facility. In 2026, boutique gyms and big-box fitness centers face intense competition from home workout platforms and community wellness centers. You can use this saturation to your advantage. Approach the gym manager and express your intent to cancel due to the high monthly cost. Cite a cheaper competitor nearby or a digital fitness subscription you plan to use instead. Managers possess wide latitude to retain members. They can waive annual maintenance fees, drop your monthly rate to a corporate or student tier, or throw in complimentary personal training sessions. If you pay upfront for the entire year in cash, you can often negotiate an additional twenty percent off the standard monthly rate.

Financial Habit #7: Home Alarm and Security Systems

Traditional home security companies charge exorbitant monthly monitoring fees, relying on the fear of property crime to justify forty to sixty dollars a month. The explosion of high-quality, do-it-yourself security ecosystems has completely disrupted this market, stripping traditional providers of their pricing power. Call your security company and express frustration with the high monthly recurring cost. Point out that you can purchase a comprehensive wireless system for a one-time fee and pay just ten dollars a month for professional monitoring elsewhere. To avoid losing you entirely, traditional providers will frequently cut your monitoring fee in half or offer free hardware upgrades to modernize your aging system. Never accept a simple equipment upgrade without securing a permanent reduction in your monthly monitoring rate. Your goal is to decrease your baseline expenses and keep your cash.

Financial Habit #8: Pest Control Services

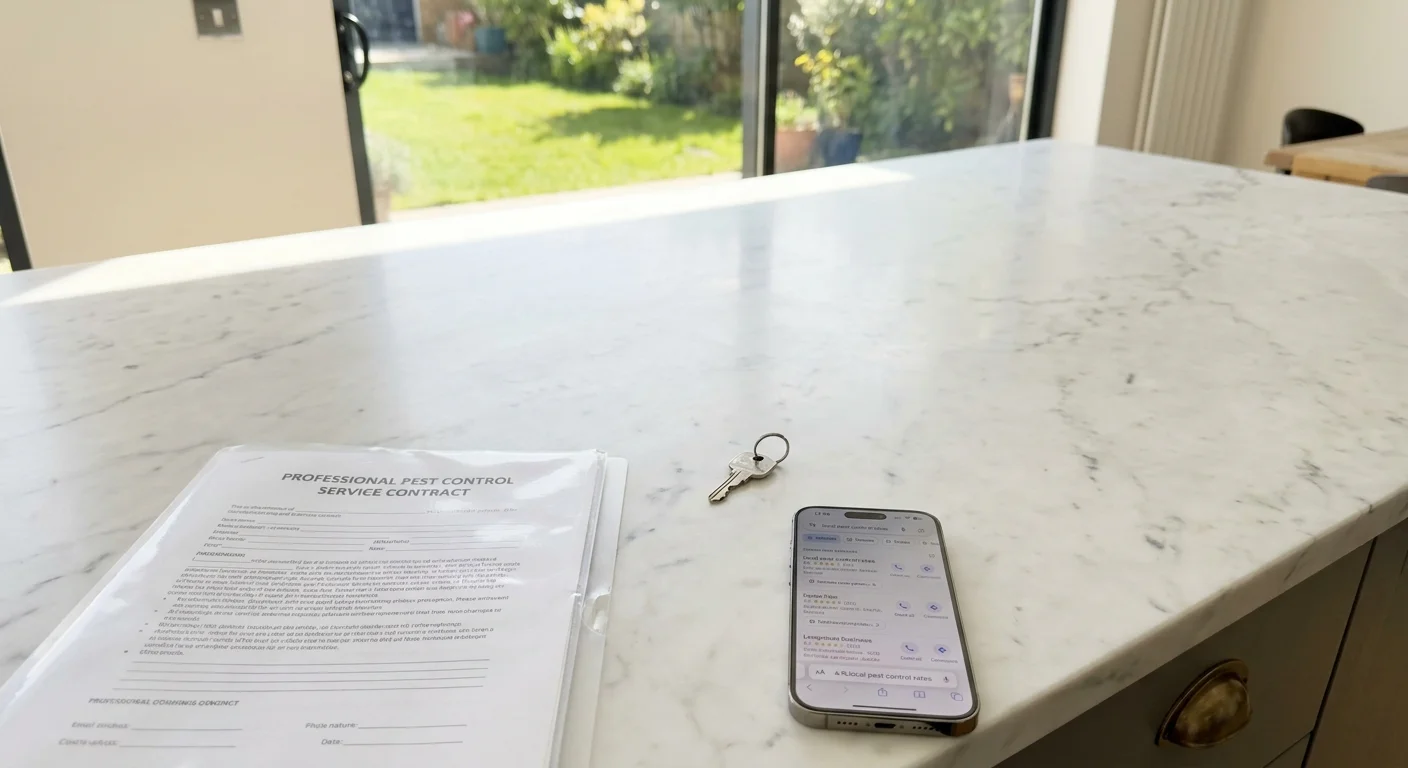

Pest control companies operate on a route-based business model, meaning their profitability hinges on servicing multiple homes in the same neighborhood on the same day. You hold significant leverage if you understand this logistical constraint. When your quarterly or annual renewal notice arrives, call the local branch manager. Explain that you are reviewing your household expenses and considering cheaper alternatives. Ask for a loyalty discount or a price match against a local competitor. To maximize your negotiating power, speak with your neighbors. If you can bundle two or three homes on your street and present this package deal to the pest control company, they will almost always grant a heavy volume discount to secure the localized route. This strategy easily shaves twenty to thirty percent off your annual service contract without sacrificing the quality of your treatments.

Financial Habit #9: Rent and Lease Renewals

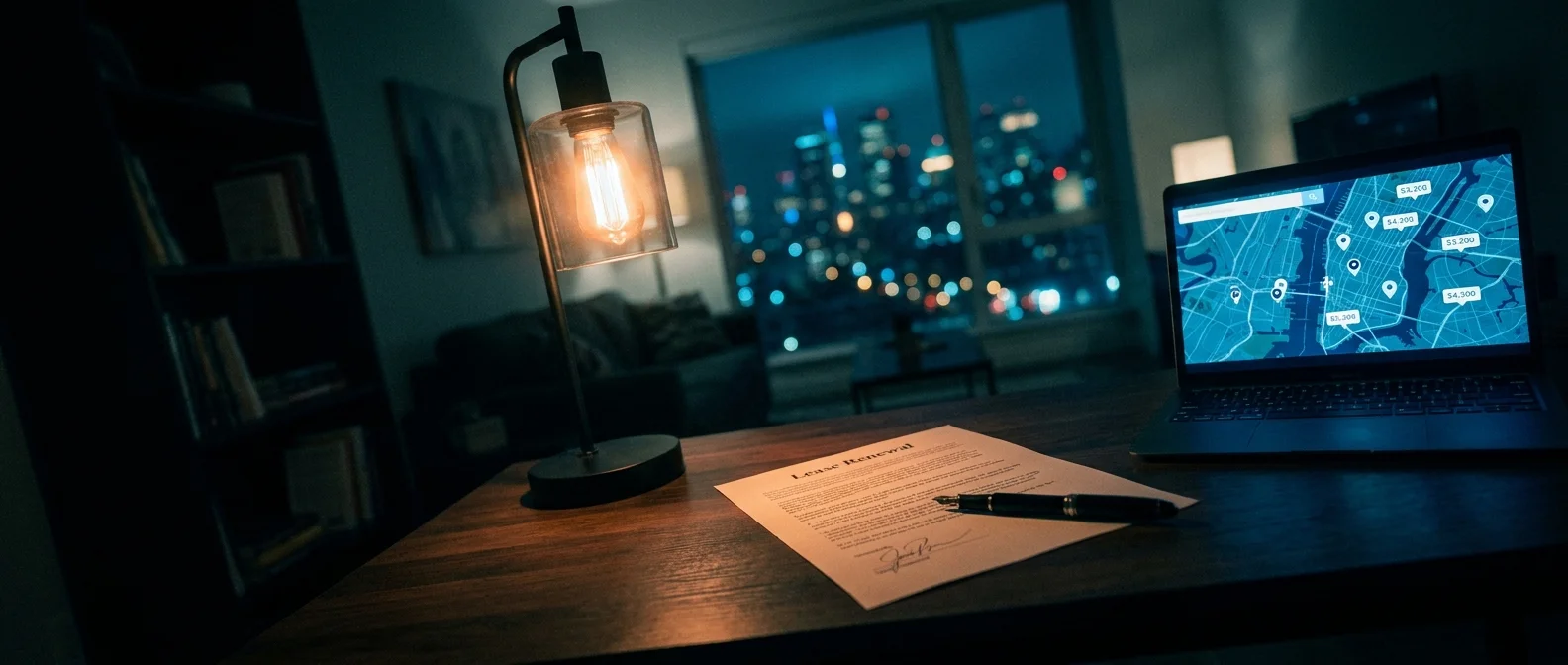

Housing represents the largest line item in the average American budget, and accepting a proposed rent increase without a fight constitutes a massive financial unforced error. Property managers despise turnover. Cleaning a unit, marketing the property, and letting it sit vacant for a month completely eradicates their profit margins. Two months before your lease expires, research comparable units in your exact neighborhood. If market rents have cooled or stabilized, print out these listings. Schedule a meeting with your landlord or property manager to discuss your renewal. Emphasize your stellar track record. Remind them that you pay rent early, maintain the property immaculately, and never cause disturbances. Propose a flat renewal with zero increase, or offer to sign an extended eighteen-month lease in exchange for a lower monthly rate. Landlords routinely concede a slight reduction to retain a reliable tenant.

Financial Habit #10: Streaming and Subscription Bundles

The streaming wars have resulted in severe subscription fatigue, with the average household bleeding over a hundred dollars monthly on digital services they barely watch. Media companies have realized that retaining subscribers is far cheaper than acquiring new ones, shifting the balance of power back to the consumer. You rarely even need to speak to a human to negotiate these bills down. Log into your account settings and initiate the cancellation process. As you click through the prompts, the algorithm will aggressively attempt to save your account by offering immediate discounts. You will frequently encounter offers for fifty percent off your next six months or a complimentary upgrade to an ad-free tier. Accept the discounted rate, set a calendar reminder for when the promotion expires, and repeat the process. By systematically threatening cancellation across your digital ecosystem, you capture premium content at a fraction of the retail price.

The Big Picture: How This Affects Your Financial Future

Trimming ten dollars here and fifty dollars there might feel insignificant in the heat of the moment, but these minor victories create massive shockwaves across your overall financial trajectory. The core philosophy behind these frugal living tips does not revolve around deprivation; it centers entirely on efficiency. When you negotiate bills and eliminate artificial corporate markups, you reclaim capital that rightfully belongs to you. This is the cornerstone of responsible personal finance.

Consider the mathematical reality of these negotiations. If you successfully apply these tactics to lower monthly bills across your cable, auto insurance, and cell phone plans, you easily free up an additional three hundred dollars every single month. That translates to three thousand six hundred dollars a year in found money. Instead of allowing that cash to vanish into the corporate coffers of a telecommunications giant, you can deploy it strategically. You can direct that capital toward crushing high-interest credit card debt, building an impenetrable six-month emergency fund, or maxing out your individual retirement account.

If you invest that saved three hundred dollars a month into a low-cost index fund returning an average of eight percent annually, your brief phone calls will compound into over fifty-four thousand dollars in just ten years. Wealth building rarely stems from a single windfall. True financial independence materializes through the ruthless optimization of your baseline expenses. By taking control of your outgoing cash flow today, you dictate the terms of your financial future and accelerate your journey toward absolute financial freedom.

Frequently Asked Questions

How often should I negotiate my bills?

You should perform a comprehensive audit of your household expenses every six to twelve months. Most promotional rates, introductory discounts, and retention offers expire after a year. Set a recurring calendar reminder thirty days before a major contract or promotional period ends. This proactive approach gives you ample time to research competitor pricing and initiate negotiations before a sudden rate hike hits your checking account. Consistent monitoring ensures you never pay the loyalty penalty.

What should I say if a representative refuses to lower my rate?

If a front-line representative denies your request, remain polite but firm. Acknowledge that they may not have the authorization to adjust pricing, and request a transfer to the retention department or a shift supervisor. Retention agents possess specific metrics tied to preventing customer churn and hold the authority to dispense heavy discounts. If the retention specialist still refuses, calmly state that you will be canceling your service and moving to a competitor. You must be willing to follow through on this threat. Sometimes the best negotiation tactic involves simply walking away and securing the new customer promotional rate at a rival company.

Do negotiation services actually work, or should I do it myself?

Third-party bill negotiation platforms have surged in popularity, offering to haggle with providers on your behalf in exchange for a percentage of the savings. While these services provide convenience, they eat into your actual wealth-building potential. Taking thirty to forty percent of your first-year savings represents a steep and unnecessary fee. You are fully capable of reading a script and making a ten-minute phone call. Doing it yourself ensures you keep one hundred percent of the money you save. Reserve third-party services only for situations where you suffer from extreme phone anxiety or simply do not have the time to audit your finances.

Can negotiating my bills negatively impact my credit score?

Negotiating standard utility, telecommunications, or insurance rates has absolutely zero impact on your credit score. These companies do not report your successful price reductions to credit bureaus. However, you must exercise caution when negotiating active debt, such as a credit card balance or a massive medical bill. Asking for a lower interest rate on a credit card is perfectly safe, but settling a debt for less than you owe will severely damage your credit profile. Always specify that you are seeking an interest rate reduction or a hardship payment plan, not a debt settlement that will trigger a negative mark on your credit report.

For official information on consumer finance and debt, consult the CFPB. Tax information is available from the IRS. For investment basics, refer to the U.S. SEC.

Disclaimer: This article provides informational content and personal opinions, not professional financial advice. Consult a certified financial advisor for guidance tailored to your specific situation.

Leave a Reply