The 2026 retirement landscape is packed with hidden financial landmines and unprecedented opportunities that most Americans will not see coming. If you think your retirement income is on autopilot, you are leaving thousands of dollars on the table. This year brings drastic shifts to Medicare Part D costs, a stealth tax on high-earner catch-up contributions, and a shrinking Social Security cost-of-living adjustment that will stretch your budget to the limit. We dug into the latest IRS code updates and federal healthcare shifts to expose the truth about your money. You must act aggressively to protect your nest egg. Here is exactly how to navigate the biggest retirement income surprises this year and keep more cash in your pocket.

Tip #1: The Social Security COLA “Illusion” and Medicare Part B

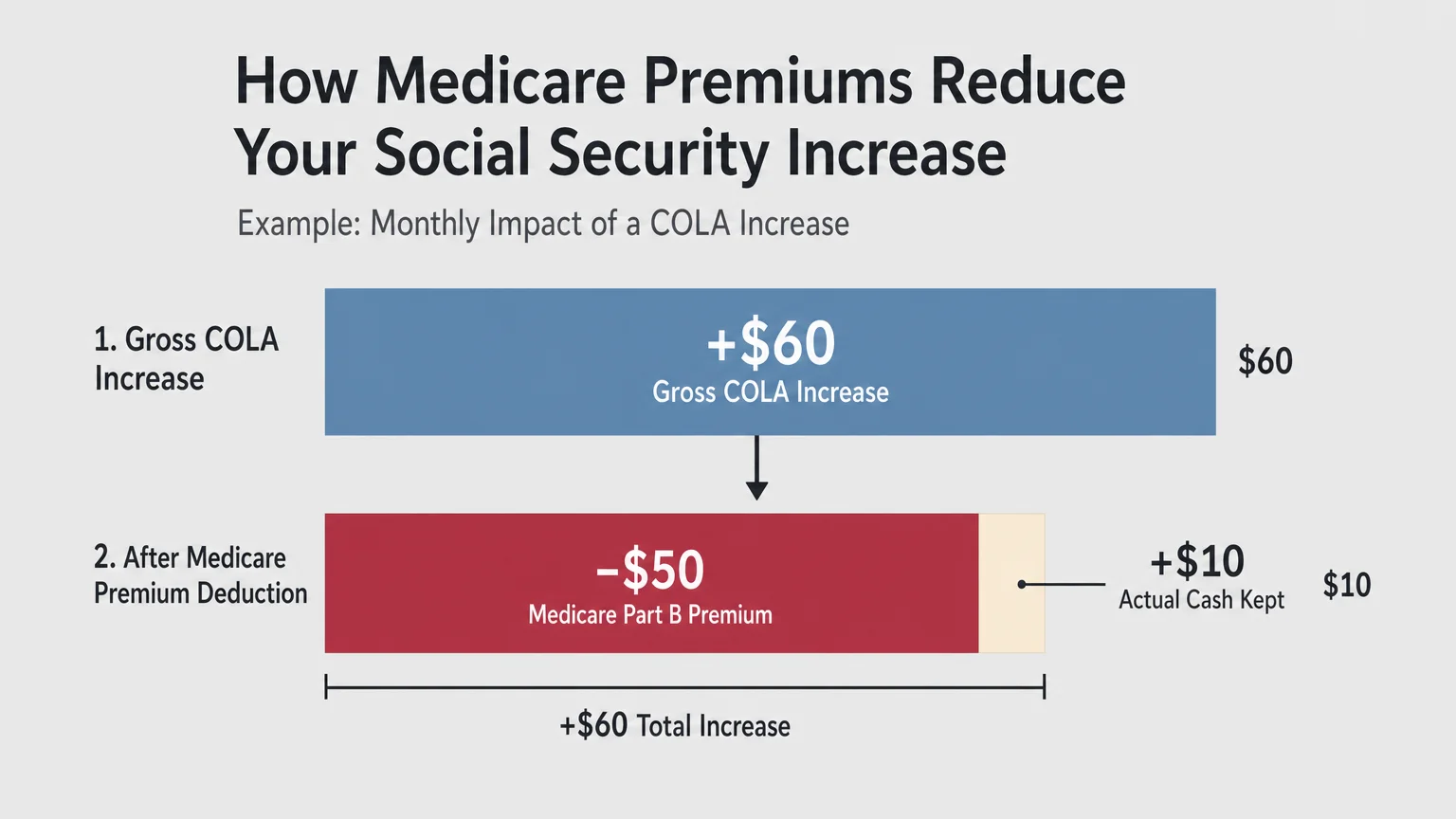

The Social Security cost-of-living adjustment for 2026 is projected to hover around 2.8 percent, a stark drop from the historic inflation-driven spikes of previous years. While a modest bump sounds like a victory on paper, it is effectively an illusion for millions of beneficiaries. The financial surprise comes directly from the Centers for Medicare and Medicaid Services.

Medicare Part B premiums are rising aggressively this year. Because Part B premiums are deducted directly from your Social Security checks, this cost increase will cannibalize almost the entire COLA for average earners. You might see a gross increase of sixty dollars a month, only to watch fifty dollars vanish to cover healthcare. This is a severe hit to senior budgeting strategies.

Advocates have long argued that the current formula, which uses the Consumer Price Index for Urban Wage Earners and Clerical Workers, completely fails to capture the true living expenses of seniors. Until the government adopts an index focused on elderly expenses, your benefits will continue to lose purchasing power.

Your best defense is to aggressively manage your Modified Adjusted Gross Income. The government uses your income from two years prior to determine your Medicare premiums through the Income-Related Monthly Adjustment Amount surcharge. If you had a temporary income spike in 2024, you will be punished with higher premiums in 2026. File an appeal form SSA-44 immediately if you have experienced a life-changing event like retirement or a drop in work hours to eliminate this surcharge.

Tip #2: The Stealth Tax on High-Earner Catch-Up Contributions

One of the most consequential retiree updates this year targets high earners directly. If your W-2 wages exceeded $150,000 in the previous year, you are now legally barred from making pre-tax catch-up contributions to your 401(k), 403(b), or 457(b) retirement plans.

Under the fully active SECURE 2.0 legislation, the IRS forces you to direct those extra catch-up dollars into a Roth account. While Roth accounts provide tax-free growth, losing the immediate upfront tax deduction is a brutal blow to your current-year tax strategy. For a high earner maxing out an $8,000 catch-up, losing that deduction could mean paying thousands more in federal income tax this April.

Payroll providers and plan administrators are tasked with enforcing this rule, but administrative errors are rampant. You must proactively audit your pay stubs. If an error occurs and your pre-tax catch-up is incorrectly allowed, you face the nightmare of unwinding excess contributions and paying IRS penalty fees. Take charge of your payroll settings early in the year.

You must adapt to these benefit changes. If you are self-employed or have a side business, you have leverage. You can adjust your business structure or owner compensation to keep your official W-2 wages just under the $150,000 threshold, allowing you to retain the pre-tax deduction. Alternatively, if you are forced into the Roth catch-up, balance the tax hit by maximizing contributions to a Health Savings Account, which remains fully pre-tax and triple-tax-advantaged regardless of your income bracket.

Tip #3: Surviving the Medicare Part D Plan Consolidation

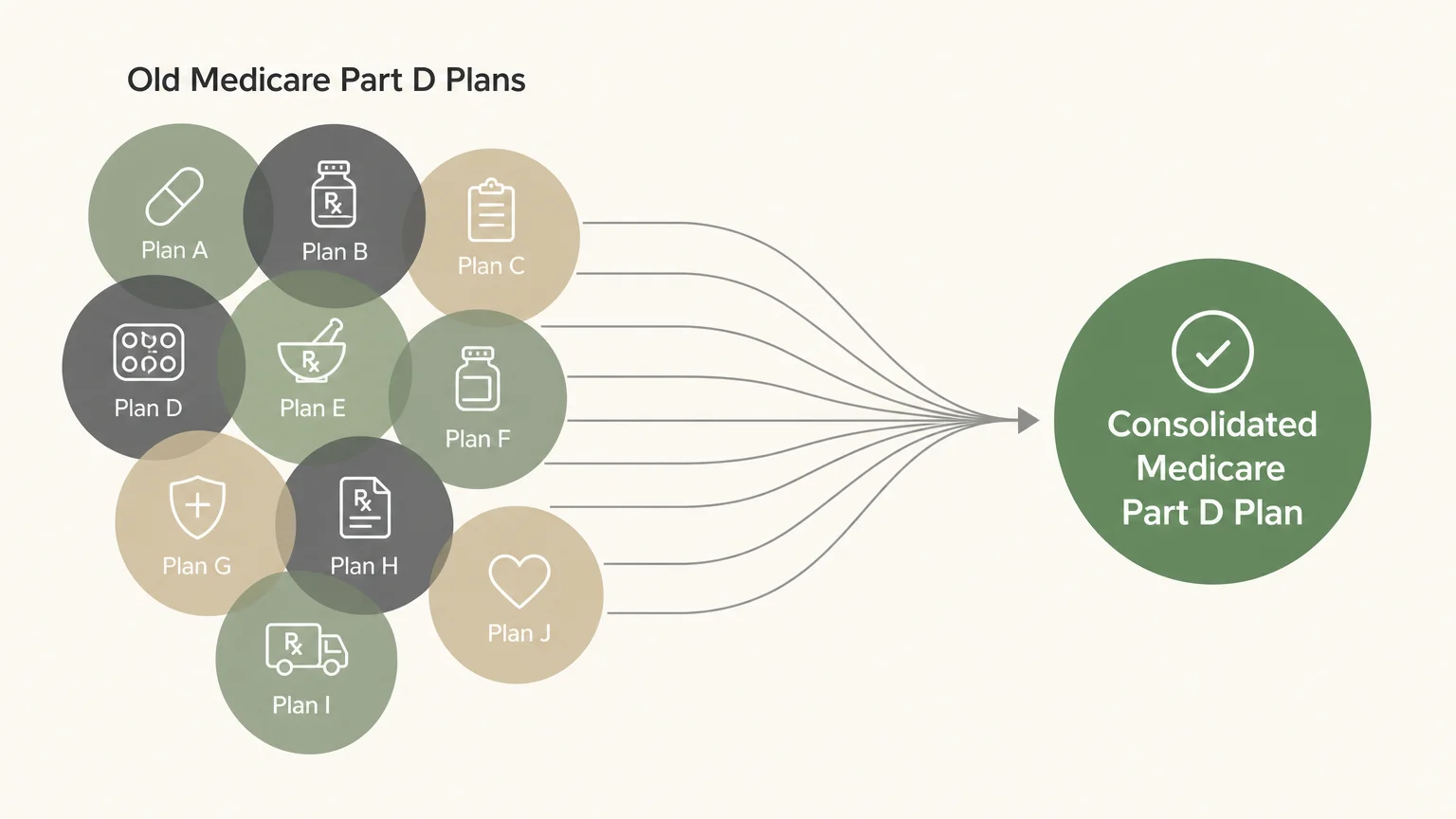

Retirement income trends are heavily influenced by healthcare costs, and the Medicare Part D landscape has fundamentally shifted. The Inflation Reduction Act successfully capped out-of-pocket prescription drug costs at $2,000 annually, which is a massive win for seniors with expensive medical conditions. However, insurance companies are not charities, and they have reacted aggressively.

To offset the new $2,000 cap, major insurers have abandoned the standalone prescription drug plan market. Experts note that a staggering number of plans have been withdrawn, leaving a virtual oligopoly in control of your coverage. The remaining plans are surviving by dramatically increasing monthly premiums, inflating base deductibles, and reclassifying maintenance drugs into higher, more expensive tiers.

The infamous coverage gap, commonly known as the donut hole, has been structurally eliminated, which simplifies the billing process. However, insurers are recouping those lost margins through aggressive prior authorization demands. You might find that a medication you have taken for a decade suddenly requires your doctor to submit extensive paperwork before the pharmacy will fill the prescription.

Do not auto-renew your coverage this year. The drug plan that saved you money last year could drain your wallet in 2026. You must input your exact prescription list into the Medicare Plan Finder during the Annual Enrollment Period. Pay close attention to formulary restrictions and prior authorization requirements, which insurers are using as a backdoor method to deny coverage for expensive medications.

Tip #4: The 401(k) “Super Catch-Up” Window

If you are between the ages of 60 and 63, the IRS has handed you a golden ticket. A little-known provision has activated, creating a specialized super catch-up contribution tier for older workers nearing the finish line.

Instead of the standard $8,000 catch-up allowance for anyone over fifty, this specific age bracket can funnel up to $11,250 in catch-up contributions into a workplace retirement plan. When combined with the new base contribution limit of $24,500, a 62-year-old worker can shelter a massive $35,750 in a single year.

Keep in mind that this super catch-up provision interacts with the high-earner Roth mandate. If you make over $150,000 and are in the 60-to-63 age bracket, you can still contribute the massive $11,250 catch-up, but every single cent of it must go into the Roth side of your plan. This creates a fascinating planning dynamic where your peak earning years intersect with mandatory after-tax savings.

This is one of the most powerful financial surprises of the decade. The catch is that this window closes as soon as you turn 64, dropping your limit back to the standard threshold. You must exploit this four-year gap. If you and your spouse fall into this age range, you can jointly shelter over $70,000 annually from federal income taxes. Use this brief period to aggressively front-load your investments and pad your nest egg right before you transition into fixed-income living.

Tip #5: Navigating the New Tax Landscape and the “Senior Bonus”

For years, financial planners warned of a massive tax cliff due to the expiration of the Tax Cuts and Jobs Act. The good news is that recent legislative maneuvers have largely averted this disaster, making the lower marginal tax brackets and the elevated standard deductions permanent for the foreseeable future.

This stability provides a massive advantage for your retirement income strategy. Because we now know the 22 percent and 24 percent tax brackets are secure, you can confidently execute multi-year Roth conversion ladders. Moving money from your pre-tax IRA to a Roth IRA up to the top of these relatively low brackets is the ultimate defensive play against future deficit-driven tax hikes.

Beyond the standard deduction, the State and Local Tax deduction cap has seen significant movement, offering relief to retirees residing in high-tax states. Balancing your property tax payments against the new deduction caps requires meticulous year-end tax planning. Do not rely on outdated tax software that fails to account for these eleventh-hour legislative changes.

Additionally, Congress introduced targeted relief for older Americans. Taxpayers aged 65 and older can now claim a significantly expanded senior bonus deduction, which pushes the standard deduction for an older married couple well past $40,000. By strategically keeping your taxable income below this threshold, you can pull thousands of dollars from your traditional retirement accounts entirely tax-free.

Tip #6: RMD Rules Are Tightening Around Inherited IRAs

The Internal Revenue Service has finally ended the grace period regarding inherited retirement accounts. If you inherited an IRA from a non-spouse who was already taking Required Minimum Distributions, the confusing ten-year rule is now being strictly enforced.

Many heirs falsely assumed they could leave the inherited funds untouched for nine years to maximize tax-deferred growth, draining the account in year ten. The IRS has firmly ruled that you must take annual distributions during years one through nine if the original owner had reached RMD age. Failing to withdraw these funds results in a brutal excise tax penalty.

This tightening also deeply impacts trusts named as IRA beneficiaries. The look-through rules determining how fast a trust must distribute retirement assets are incredibly unforgiving under the new regime. If your estate plan relies on an outdated trust structure to pass down IRA wealth, your heirs could face a devastating accelerated tax bill.

This forces you to meticulously plan your withdrawals. If you are still working and in your peak earning years, taking an unexpected inherited RMD can easily bump you into a higher tax bracket and trigger capital gains surtaxes. You need to work with a tax professional to calculate the precise minimum amount required each year, deferring larger withdrawals for years when your primary income drops, such as immediately after you officially retire.

Tip #7: Inflation Has Permanently Shifted “Safe” Withdrawal Rates

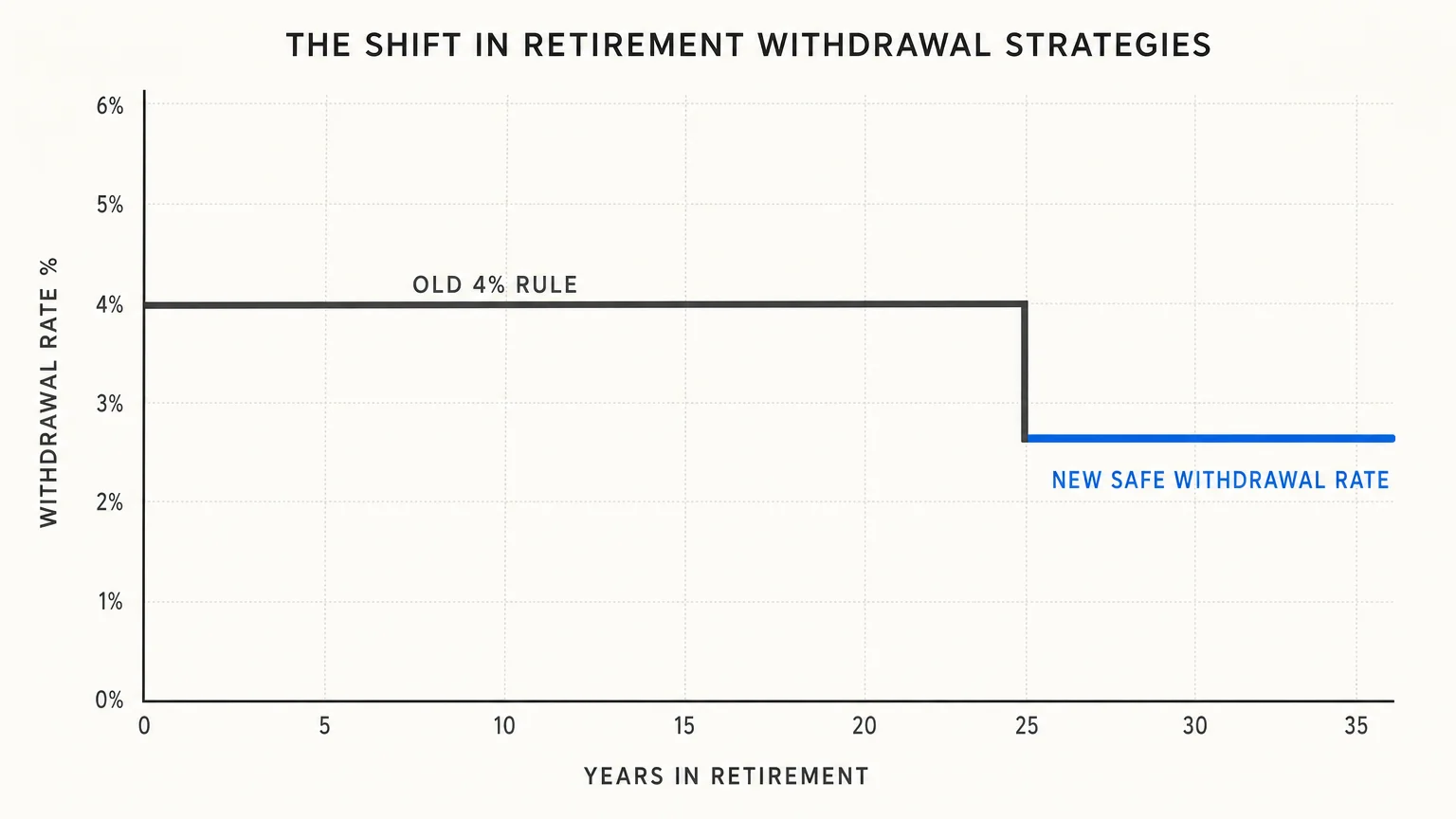

Inflation has fundamentally broken traditional retirement math. The famous four percent rule—the idea that you can safely withdraw four percent of your portfolio in year one and adjust for inflation thereafter—is mathematically dangerous in the current economic environment. Rigidly pulling fixed amounts during market volatility will either deplete your portfolio prematurely or force you to live on a shoestring budget.

Savvy retirees are adopting dynamic withdrawal strategies. This means taking a slightly higher percentage when your portfolio is outperforming the market, and tightening your belt when equities take a hit. This flexibility is the only way to ensure your money outlives you.

This concept is known as mitigating sequence of returns risk. Experiencing a severe bear market in the first three years of your retirement can permanently cripple your portfolio if you are forced to sell shares at a discount. A dynamic approach, anchored by a robust cash reserve, acts as an impenetrable shield against Wall Street volatility.

To execute this hack successfully, you must establish a cash buffer. Keep two to three years of essential living expenses in high-yield savings accounts, short-term Treasuries, or certificates of deposit. When the stock market crashes, you pause your portfolio withdrawals and live off the cash buffer. This prevents you from selling equities at a loss and guarantees your investments have the time they need to recover.

Tip #8: Phased Retirement is the New Normal

The concept of a hard-stop retirement date—where you work full-time on Friday and completely stop on Monday—is rapidly becoming obsolete. The current trend sweeping the corporate world is the phased retirement off-ramp. Employers are desperate to retain institutional knowledge in a tight labor market and are willing to negotiate lucrative part-time arrangements.

Instead of quitting entirely, you can transition to a twenty-hour workweek. The secret hack here is that many of these phased retirement packages allow you to retain your full corporate health insurance benefits and continue receiving employer matches in your 401(k). This setup covers your essential living expenses and medical costs while keeping your primary nest egg completely untouched.

Furthermore, a phased retirement allows you to delay claiming your Social Security benefits. Every year you hold off past your full retirement age guarantees an eight percent permanent increase in your monthly payout. Using part-time income to bridge the gap until age seventy is one of the most mathematically sound strategies to maximize your lifetime government benefits.

You should pitch this arrangement to your human resources department at least a year before you intend to leave. Frame it as a necessary succession planning tool to train your replacement. Working just two extra years on a part-time basis can drastically reduce the number of years you rely solely on your savings, entirely changing the trajectory of your financial future.

The Bottom Line: What This Means for Your Wallet

Complacency is the enemy of a wealthy retirement. As the rules surrounding taxes, healthcare, and account withdrawals shift, relying on outdated advice is a guaranteed way to lose your hard-earned money. The 2026 landscape demands active, aggressive management of your financial life. You must scrutinize your Medicare coverage annually, optimize your catch-up contributions, and remain hyper-vigilant about your tax brackets.

Take control of your money by challenging the default options. Do not settle for auto-renewals, and never assume the government will optimize your tax burden for you. By applying these strategies, you can bypass the traps and secure the comfortable, stress-free retirement you deserve.

Frequently Asked Questions

Will Social Security run out of money soon?

No, Social Security is not going bankrupt. The program is funded continuously by payroll taxes from active workers. However, the trust funds supplementing those taxes face depletion by the mid-2030s. If Congress fails to pass structural reforms, benefits could face an across-the-board reduction. You should plan your budget assuming a conservative payout and prioritize your personal investment accounts to bridge any future gaps.

Is a Roth conversion still a smart move this year?

Yes, executing a Roth conversion remains one of the most powerful tax hacks available. With the recent extension of the lower income tax brackets, you have a clear, predictable window to convert pre-tax dollars at historically favorable rates. Moving money into a Roth account shields your future growth from inevitable tax hikes and eliminates Required Minimum Distributions entirely for those specific funds.

How can I avoid the Medicare premium surcharge?

You must meticulously track your Modified Adjusted Gross Income. The dreaded Income-Related Monthly Adjustment Amount surcharge is based on your tax return from two years prior. Avoid executing massive, single-year taxable events like cashing out a large stock position or converting your entire IRA at once. Spread your taxable income evenly across multiple years to stay under the surcharge thresholds and keep your healthcare costs manageable.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply