Retirement brings freedom, but relying on a fixed income turns every supermarket trip into a financial battle. You can quickly slash $50 off your weekly grocery bill by treating your shopping like a business and outsmarting retail tricks designed to drain your wallet. Supermarkets engineer their layouts, pricing models, and packaging to extract maximum profit from unsuspecting shoppers. By ignoring flashy endcaps, weaponizing senior discounts, and changing how you source protein, you immediately take back control of your food costs. It requires a contrarian mindset and a willingness to abandon lifelong shopping habits; however, keeping an extra $200 a month in your retirement account is the ultimate payoff.

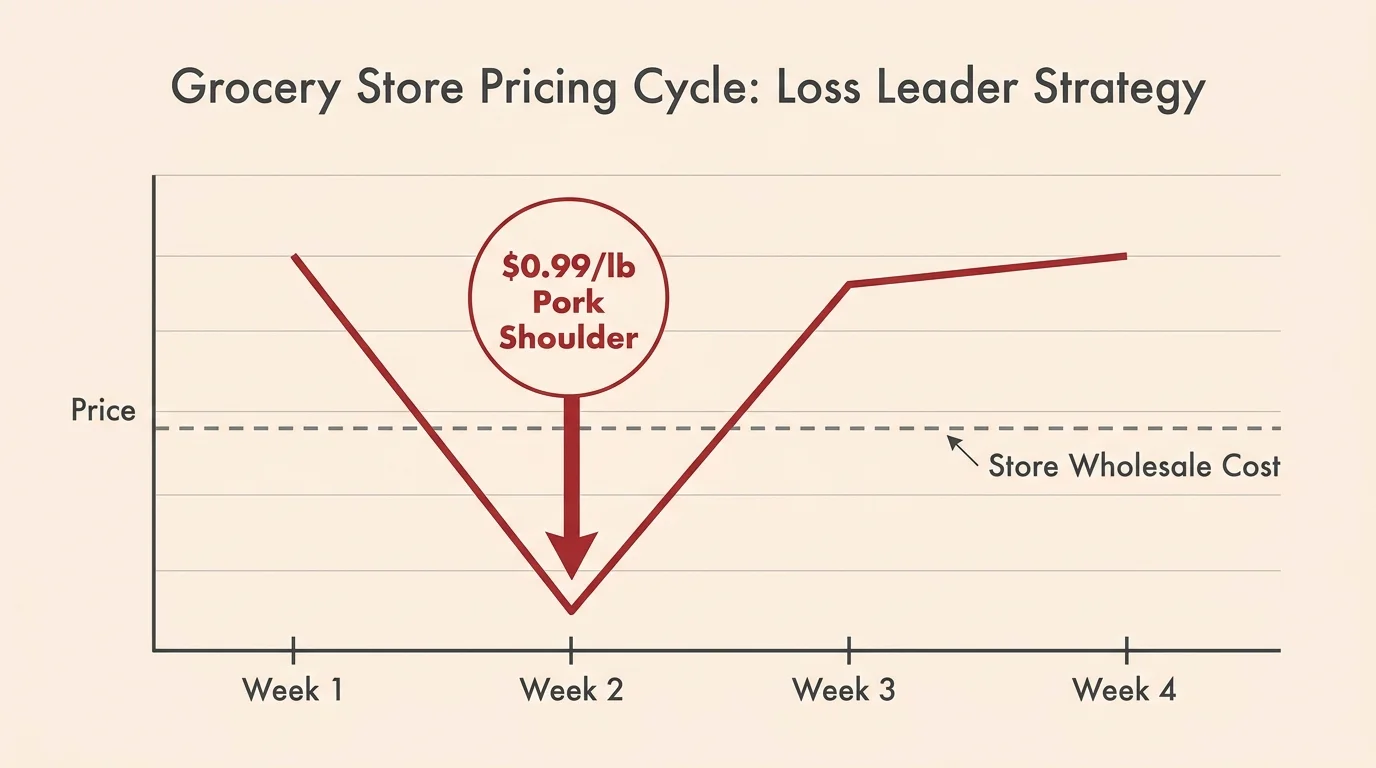

Tip #1: Exploit the “Loss Leader” Meat Cycle

Supermarkets play a constant game of psychological warfare, and their most effective weapon is the loss leader. These are items—usually expensive proteins like beef roasts, chicken breasts, or pork chops—that the store sells below cost simply to drag you through their automatic doors. Frugal retirees know exactly how to exploit this strategy for grocery savings. Instead of planning your meals and then shopping, you must flip the script; plan your meals exclusively around what the supermarket is virtually giving away. If pork shoulder is ninety-nine cents a pound, you are eating pulled pork. Buy these loss leaders in bulk, process them at home, and load your freezer. Stores expect you to buy the deeply discounted chicken and then fill your cart with high-margin marinades, sides, and snacks. You defeat their system by walking in, grabbing the loss leaders, and ignoring the overpriced traps completely. Doing this consistently forces your overall food costs down dramatically while keeping your kitchen heavily stocked.

Tip #2: Weaponize Unadvertised Senior Discount Days

Many grocery chains offer senior discount days, but the most lucrative programs are often hidden from public view. Supermarkets rely on you feeling too embarrassed to ask for a discount, hoping you just pay full price. As a retiree protecting a fixed retirement budget, you must abandon any shame and directly ask customer service desk managers about unadvertised senior perks. Regional grocers frequently offer five to ten percent off your entire cart on specific weekdays when foot traffic is slow. You can compound these savings by scheduling major shopping trips exclusively on these discount days and stacking them with digital coupons. Never assume the cashier will automatically apply your discount; it is your responsibility to demand it before paying. Ten percent off a two-hundred-dollar cart immediately hands you twenty dollars back. Over a month, simply choosing the right day of the week to buy groceries gets you incredibly close to that fifty-dollar weekly goal.

Tip #3: Ditch National Brands for Store-Brand Private Labels

The grocery industry operates on a brilliant illusion of choice, tricking you into paying a premium for a fancy logo. Most generic store brands roll off the exact same manufacturing lines as their heavily marketed national competitors. Frugal retirees understand that paying an extra dollar for a branded box of cereal is the fastest way to ruin a retirement budget. By categorically switching all basic pantry staples—flour, sugar, canned vegetables, spices, and dairy—to the store brand, you instantly shave twenty percent off your bill. You are literally paying for television commercials and flashy packaging when you buy national brands. Conduct a blind taste test at home; you will almost certainly fail to spot the difference between premium ketchup and the private label. Making this permanent switch across your entire shopping list removes the emotional attachment to brands and treats food strictly as a commodity.

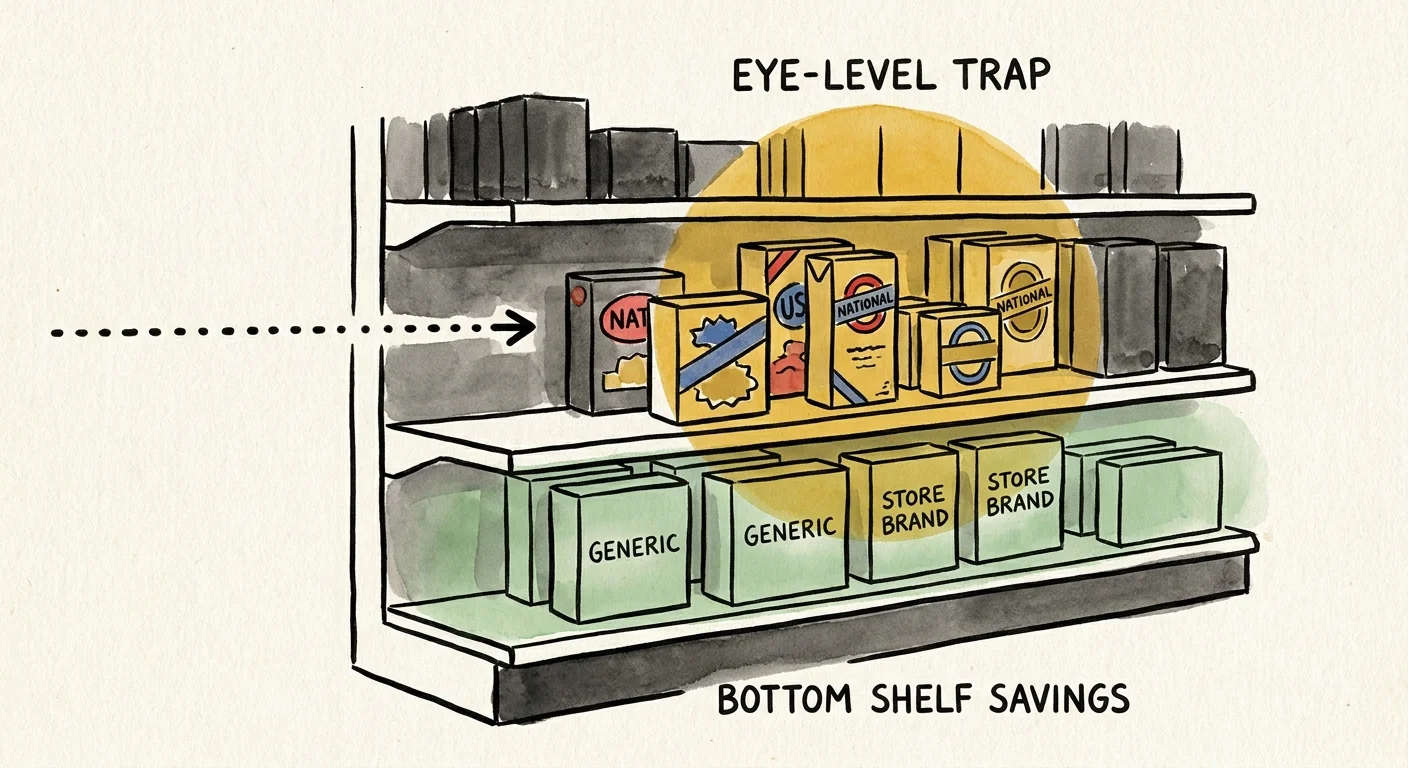

Tip #4: Master the Art of the Bottom Shelf Scan

Supermarket layouts are engineered by consultants who track eye movements and consumer psychology. The golden rule of grocery merchandising places products with the highest profit margins directly at eye level. When you stroll down the aisle and casually grab a jar of pasta sauce without looking down, you are overpaying. To protect your retirement budget, you must master the art of the bottom shelf scan. The cheapest products, bulk items, and best overall values are almost always relegated to the floor-level shelves. Supermarkets know that most shoppers are simply too lazy to bend down and hunt for bargains. By consciously shifting your gaze to the lowest tiers, you uncover incredible food costs savings. You will spot the oversized bags of rice, bulk dried beans, and aggressively priced store brands that the supermarket hopes you ignore. Train yourself to look at the bottom shelf first.

Tip #5: Avoid the Convenience Tax on Pre-Cut Produce

One of the most insidious ways supermarkets drain your wallet is by charging a massive premium for basic knife skills. Pre-cut fruits, bagged salads, and diced vegetables carry an astronomical convenience tax, sometimes costing three times more per pound than their untouched counterparts. When working full-time, buying a plastic container of cubed melon made sense to save precious time. In retirement, you have the bandwidth to chop your own produce. Frugal retirees recognize that spending five minutes with a cutting board pays an absurdly high hourly rate in grocery savings. Buying whole heads of lettuce, whole carrots, and block cheese instead of the shredded variety significantly reduces your food costs while extending shelf life. Pre-cut food spoils dramatically faster because more surface area is exposed to the air. Ditch the convenience items entirely; your kitchen knife is your greatest asset.

Tip #6: Capitalize on Salvage Grocers and Bakery Outlets

If you only shop at pristine, mainstream supermarkets, you are voluntarily paying a premium for ambiance. The most aggressive grocery savings are found on the fringes of the retail world, specifically at salvage grocery stores and bakery outlets. Salvage grocers purchase massive lots of items from traditional supermarkets that are slightly damaged, discontinued, or nearing their arbitrary best-by dates. These dates rarely relate to food safety; they merely indicate peak freshness. You can walk out of a salvage grocer with a cart full of canned goods, boxed pastas, and premium snacks for a fraction of the original cost. Similarly, regional bakery outlets sell day-old bread and bagels at steep discounts simply because they lack fresh-from-the-oven status. Bread freezes beautifully, meaning you can buy ten loaves cheaply and store them for months. Embracing these alternative supply chains radically shrinks your grocery budget.

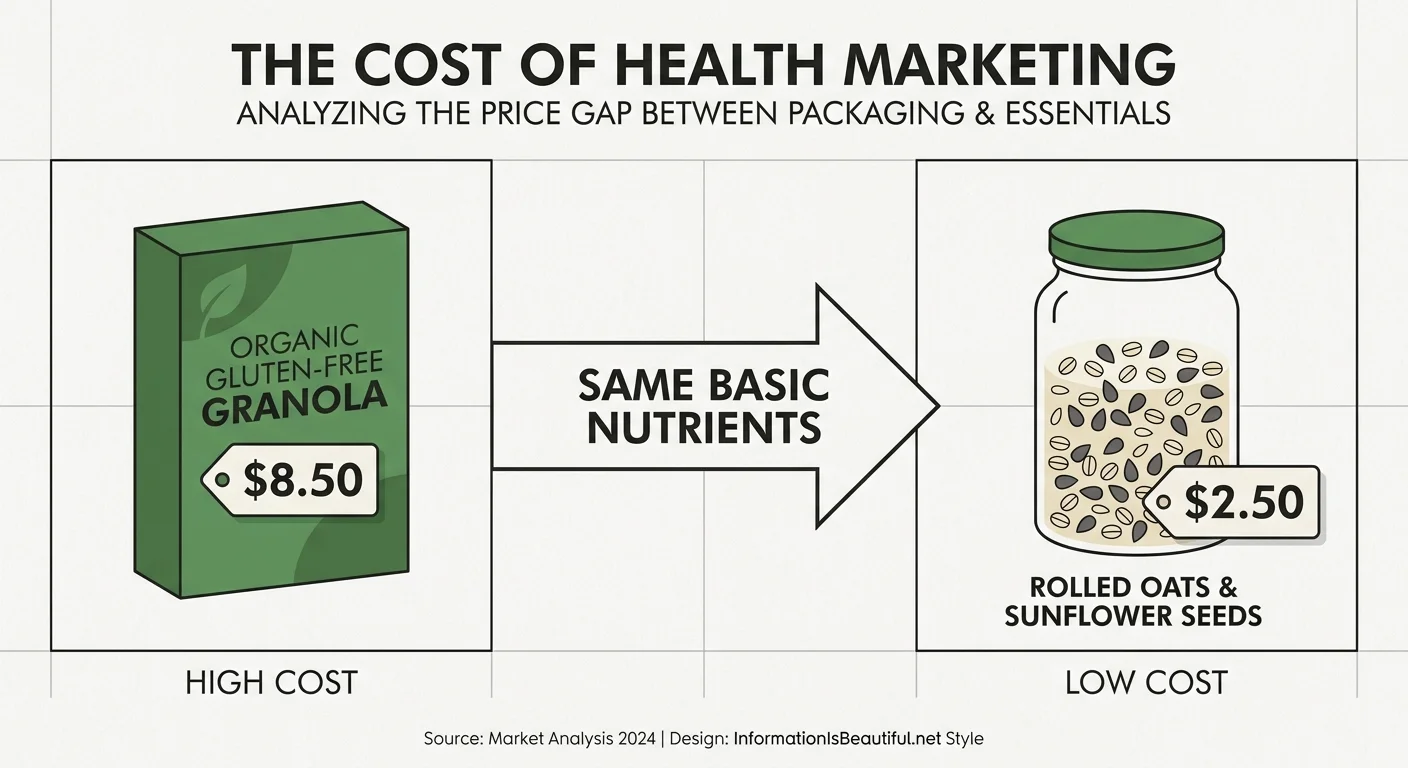

Tip #7: Stop Paying for Fake Health Food Halos

Marketers know that aging Americans are highly motivated by health concerns, and they exploit this fear by slapping “superfood” or “organic” labels on ordinary products to justify a massive markup. You do not need to buy twenty-dollar bags of organic chia seeds to maintain your health in retirement. The health food halo is a pervasive marketing trick designed to inflate your food costs under the guise of longevity. Often, the nutritional difference between a standard apple and a certified organic apple is negligible, but the price difference is staggering. Instead of falling for buzzwords on colorful boxes, focus your retirement budget on simple, single-ingredient whole foods. Conventional produce, standard oats, and basic lean proteins provide excellent nutrition without the artisan price tag. Do not let food manufacturers guilt-trip you into spending your pension on unregulated marketing adjectives.

Tip #8: Implement a Ruthless Pantry Inventory System

The fastest way to waste money is buying food you already own. Frugal retirees operate their kitchens with ruthless efficiency, utilizing strict pantry inventory systems to prevent duplicate purchases and food waste. Before you touch a pen to write your grocery list, you must conduct a physical audit of your refrigerator, freezer, and pantry. If you find two half-empty jars of marinara sauce hiding in the back of the fridge, pasta is immediately going on the menu. Create a running inventory sheet on your kitchen counter and cross items off as you consume them. By forcing yourself to build meals around ingredients currently languishing in your cupboards, you delay trips to the store and stretch your grocery cycles. Pushing your supermarket visit back by just three days every month effectively eliminates a full week of grocery spending from your annual budget.

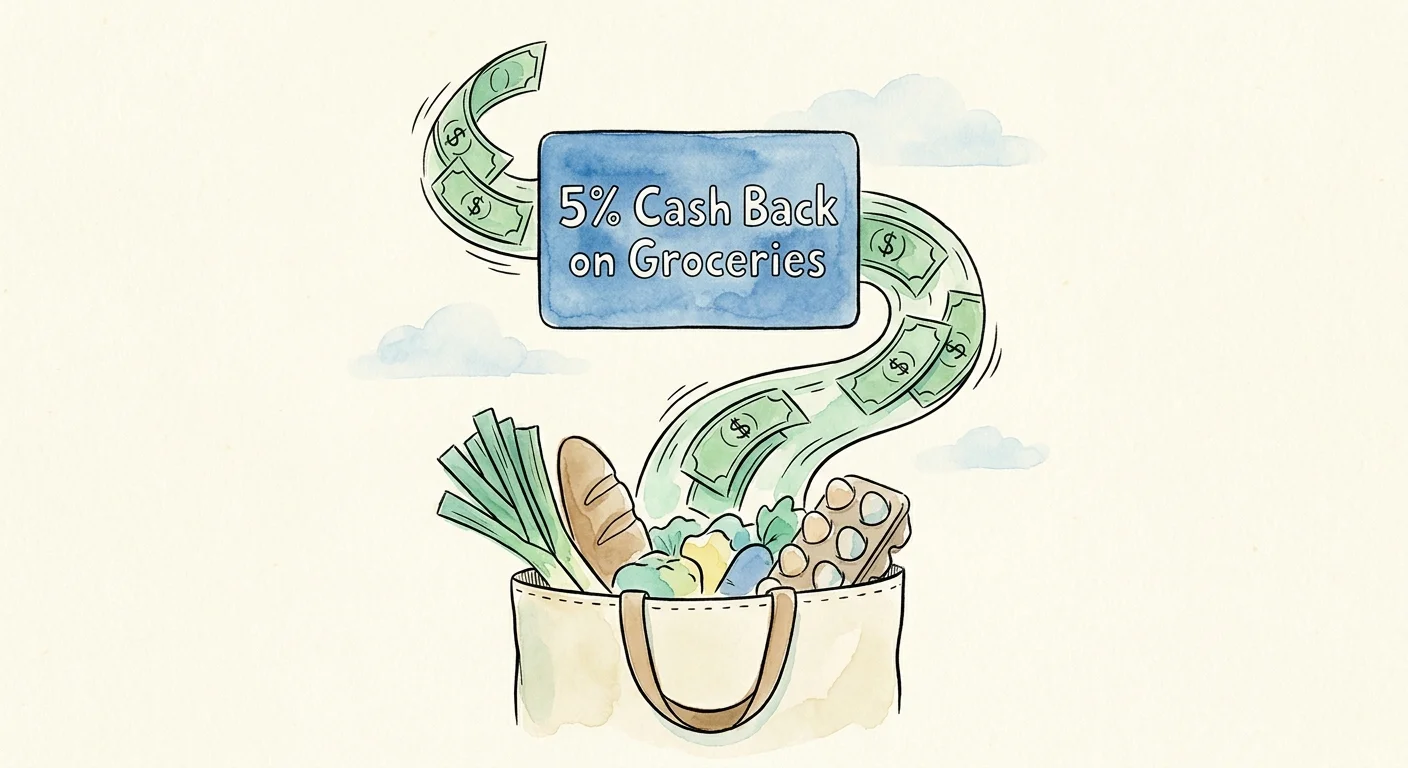

Tip #9: Exploit Credit Card Cash-Back Multipliers

Paying for groceries with cash or a standard debit card is leaving free money on the checkout conveyor belt. The banking industry offers highly competitive cash-back credit cards specifically tailored for supermarket spending, and smart shoppers use these tools as a direct discount mechanism. Several no-annual-fee credit cards offer three to six percent cash back on every single dollar spent at the grocery store. If you spend four hundred dollars a month on food, a five percent cash-back card automatically hands you twenty dollars back. The trick is treating this credit card strictly as a coupon; you must pay the balance in full the moment the statement arrives to avoid crippling interest charges. By routing your unavoidable food costs through an optimized cash-back portal, you force credit card companies to subsidize your retirement budget.

Tip #10: Pivot Your Primary Protein Sources

The American culinary tradition insists that every dinner must revolve around a massive, expensive piece of meat. Continuing this habit into retirement is a surefire way to obliterate your grocery budget. To achieve dramatic grocery savings, you must actively pivot your primary protein sources away from premium beef and poultry toward nutrient-dense, hyper-cheap alternatives. Legumes—specifically black beans, chickpeas, and lentils—cost literal pennies per serving when purchased dry and offer incredible fiber and protein. Eggs remain one of the most cost-effective proteins in the supermarket, versatile enough for any meal of the day. You do not have to become a strict vegetarian; simply implementing three meatless dinners a week radically alters your bottom line. Redefining what a complete meal looks like is the ultimate strategy for frugal retirees determined to conquer their food costs.

The Bottom Line: What This Means for Your Wallet

Achieving a significant reduction in your weekly grocery bill does not happen by accident; it happens through deliberate, calculated action. You are fighting against highly optimized retail systems designed to separate you from your retirement funds. By ignoring manipulative store layouts, aggressively seeking out unadvertised senior discounts, and fundamentally altering the way you source and prepare your meals, you build a fortress around your finances. Saving fifty dollars every week compounds into a staggering twenty-six hundred dollars a year. That is real money that you can redirect toward travel, hobbies, healthcare, or simply strengthening your emergency fund. The grocery store is not a place for leisurely browsing; it is an arena where you must execute a strict financial game plan. Armed with these grocery shopping tips, you possess the tools to outsmart the system. Stop subsidizing the supermarket’s profit margins with your fixed income. Take the extra five minutes to chop your own vegetables, hunt the bottom shelves, and leverage your pantry inventory. The ultimate reward is financial peace of mind.

Frequently Asked Questions

Are warehouse clubs like Costco or Sam’s Club worth the membership fee for retirees?

Warehouse clubs can be highly profitable for frugal retirees, provided you possess the discipline to avoid impulse buying. The massive quantities make sense for non-perishable staples, paper goods, and generic medications, which often justify the annual fee alone. However, buying bulk produce or massive trays of bakery items usually leads to food waste for a one- or two-person household. If you split bulk purchases with a neighbor or heavily utilize a deep freezer for your proteins, the membership easily pays for itself. If you tend to buy oversized snacks and let fresh food rot, stick to the standard supermarket.

How much should a retired couple actually spend on groceries per month?

While figures vary wildly based on geography and dietary restrictions, a disciplined, frugal retired couple can comfortably eat well on three hundred to four hundred dollars a month. This requires strict adherence to the grocery savings strategies outlined above, leaning heavily on dry goods, seasonal produce, and loss-leader proteins. The United States Department of Agriculture provides monthly food plan estimates, but their thrifty plan often hovers much higher than what a truly savvy shopper spends. By leveraging salvage grocers and avoiding the convenience tax, you can easily beat the national averages and protect your retirement budget.

Do digital coupon apps really save money, or do they just steal your data?

Digital coupon applications absolutely collect your shopping data to build consumer profiles; however, the financial payout is often worth the privacy trade-off. Apps like Ibotta, Fetch Rewards, or your local supermarket’s proprietary application offer immense grocery savings that physical newspaper clippings simply cannot match. You must approach these apps strategically—only clip coupons for items you already planned to buy. Do not let an app convince you to purchase a premium brand just to save fifty cents. When used strictly on necessary staples, digital rebate apps funnel direct cash back into your retirement budget.

Is it cheaper to grow your own vegetables in retirement?

Gardening can dramatically lower your food costs, but it comes with a massive caveat regarding startup expenses. If you aggressively purchase raised beds, premium soil, and expensive tools, it will take years to break even on a few tomatoes. Conversely, if you start seeds indoors, compost your kitchen scraps, and focus on high-yield, expensive supermarket items like fresh herbs, leafy greens, and bell peppers, the return on investment is stellar. Gardening is an excellent physical activity for retirees; treat it as an evolving hobby that eventually produces a lucrative edible dividend.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply