If you were born between 1941 and 1969, thousands of dollars in senior benefits are sitting on the table waiting for you to claim them. Corporations and government agencies rarely advertise these retirement perks, preferring you pay full price while they pocket the difference. By leveraging your age, you can drastically reduce your daily living costs, lower your tax burden, and protect your savings from inflation. You do not need a special membership to access most of these baby boomer benefits; you simply need to know exactly where to look and what to ask for. Stop leaving money behind and start tapping into these ten powerful benefits for seniors today to secure a much more comfortable retirement.

Tip #1: State-Level Property Tax Freezes and Exemptions

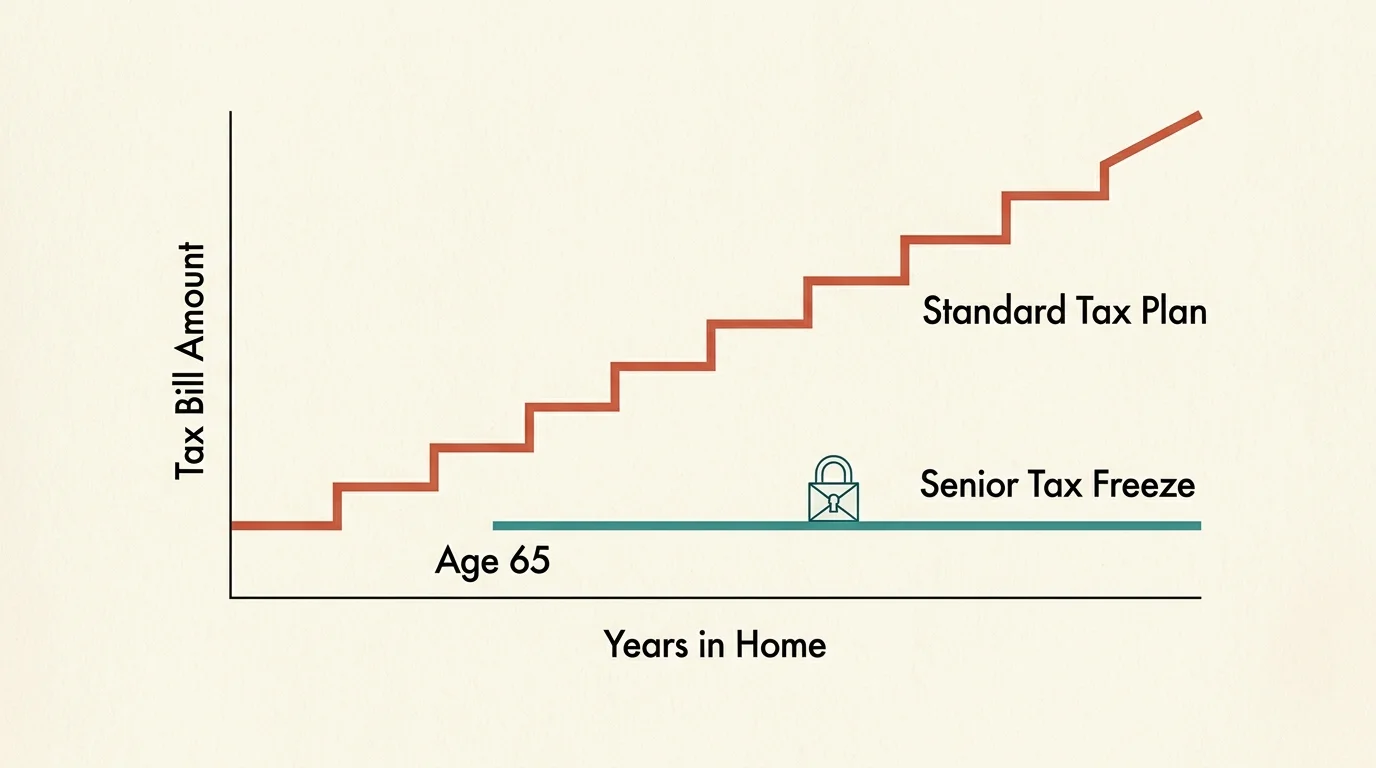

Many seniors live on a fixed income while their property taxes skyrocket year after year. Most states offer a hidden lifeline known as a property tax freeze or a homestead exemption specifically designed for older homeowners. If you meet the age and income requirements, your local tax assessor will lock your property valuation at its current rate, ensuring your tax bill never increases again. Other jurisdictions offer straight deductions, shaving thousands off your assessed value before the tax rate is even applied.

Counties intentionally hide these exemptions to keep their tax revenues artificially high. You must proactively file the paperwork with your county assessor; they will never automatically apply this discount. States like Texas and Florida offer substantial homestead exemptions that can drop your tax burden significantly. Call your local tax office today and ask about their age-based exemptions. Taking thirty minutes to fill out a single form could easily save you thousands of dollars every single year and keep you comfortably in your own home.

Tip #2: The Lifetime America the Beautiful Senior Pass

Skip the overpriced tourist traps and take advantage of the most lucrative travel hack available to older Americans. The National Park Service offers a lifetime Senior Pass to anyone aged 62 or older for a one-time fee of just eighty dollars. This pass grants you and your passengers free entry to more than two thousand federal recreation sites across the country. If you prefer short-term savings, you can purchase an annual pass for twenty dollars instead.

Aside from free admission, this pass often provides a massive fifty percent discount on federal camping fees, swimming fees, and boat launch rates. A single vehicle entry to popular destinations like Yosemite or Zion National Park costs thirty-five dollars; therefore, the lifetime pass pays for itself in just three visits. Purchase your pass online or at any federal recreation site before your next road trip to instantly slash your vacation expenses and explore the country for pennies on the dollar.

Tip #3: Stealth Cell Phone and Internet Discounts

Telecommunications companies deliberately hide their best rates, hoping you will blindly renew your expensive legacy plan year after year. If you are aged 55 or older, major carriers heavily discount their senior plans to mirror premium packages at a fraction of the cost. You can secure unlimited talk, text, and data for thirty to forty dollars per line. Telecom giants secretly offer these 55+ plans, but they often restrict them to residents of specific states—unless you negotiate aggressively.

Cable and internet providers also offer unadvertised low-income or age-based tiers. If you utilize certain federal retirement programs or simply meet the age threshold, you can drop your home internet bill to roughly twenty dollars a month. Stop paying the standard retail price for connectivity. Call your provider, state your age, and demand to be switched to their senior tier. If the representative refuses, threaten to take your business to a competitor who will gladly lower your monthly bill.

Tip #4: Zero-Cost Preventative Health Screenings Under Medicare

Millions of older Americans skip the doctor because they fear out-of-pocket costs, entirely unaware that Medicare Part B covers a massive list of preventive services at absolutely zero cost to the patient. You can schedule an annual wellness visit, cardiovascular screenings, diabetes tests, and various cancer screenings without paying a single dime in copays or deductibles. The medical system profits when you get sick, but you win by catching potential health issues early.

When you call your physician to book an appointment, explicitly state that you are scheduling your free Medicare annual wellness visit. Insist that the billing department codes the visit as preventative to avoid surprise charges. Taking advantage of these fully covered services keeps you healthier longer. More importantly, it protects your retirement savings from catastrophic medical debt down the road by catching manageable conditions before they morph into expensive, chronic emergencies.

Tip #5: Hidden Auto Insurance Discounts for Defensive Driving

Car insurance premiums are rising at an alarming rate, but you hold a trump card that younger drivers cannot access. Almost every major auto insurance provider offers a mandatory discount for seniors who complete a certified defensive driving course. Organizations like your local AAA branch offer these simple refresher courses online, and they typically take just a few hours to complete from the comfort of your living room.

New York drivers, for instance, are guaranteed a ten percent reduction on their auto liability and collision premiums for three full years after completing a certified course. Once you hand the completion certificate to your insurance agent, state laws frequently dictate that they must drop your premium. A thirty-dollar online class could effortlessly yield hundreds of dollars in cumulative savings over the next thirty-six months. Check with your insurance agent to confirm exactly how much you will save, then lock in this guaranteed return on your time.

Tip #6: Grocery Store Senior Discount Days

Supermarkets operate on razor-thin margins, making them highly protective of their profits. However, many regional and national chains dedicate specific days of the week or month to senior shoppers. Depending on your local store, you could easily score five to ten percent off your entire grocery bill just by shopping on a designated Tuesday or Wednesday. Supermarkets rely on older customers being too shy to ask for the discount, allowing the store to keep the extra cash.

While ten percent might sound trivial, shaving that amount off a four-hundred-dollar monthly food budget keeps almost five hundred dollars in your pocket over the course of a year. Regional chains have historically offered significant markdowns on their senior days. Cashiers are specifically trained not to ask your age, meaning you must proactively request the discount at checkout before you pay. Speak up, show your identification, and watch your grocery total drop instantly.

Tip #7: Auditing College Courses for Free

Retirement offers the perfect opportunity to learn a new language, study history, or dive into computer science without paying outrageous tuition fees. More than thirty states mandate that public universities and community colleges allow older adults to audit classes completely free of charge or for a nominal administrative fee. You get to absorb all the knowledge from world-class professors without the stress of exams, term papers, or student loan debt.

Schools rarely market these retirement perks because non-paying students do not boost their bottom line. In states like Ohio and Virginia, state law strictly requires public universities to allow seniors to sit in on classes tuition-free. Go to your local state university website and search for senior citizen tuition waivers. You will discover a simple registration process that grants you full access to a sprawling campus, modern libraries, and high-level academic lectures for absolutely nothing.

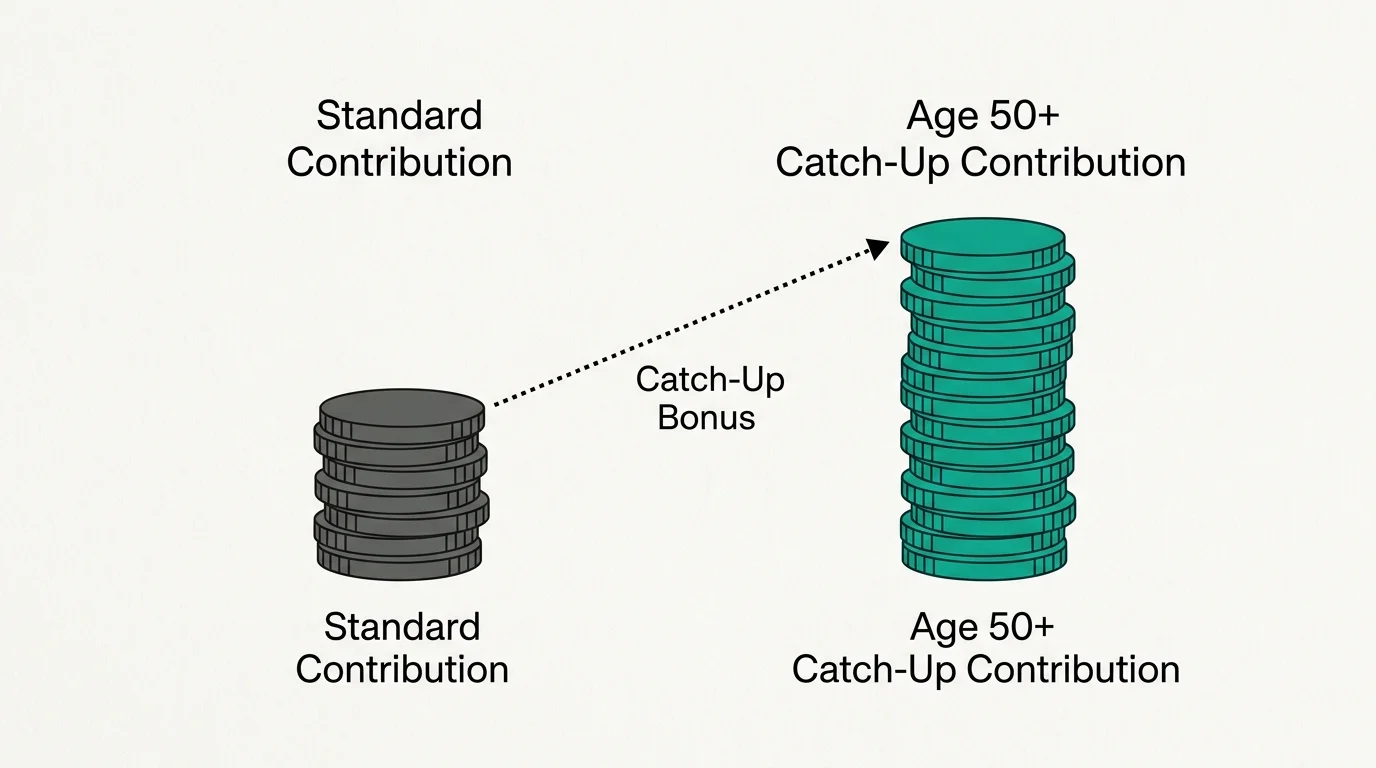

Tip #8: Catch-Up Contributions to Supercharge Your Nest Egg

If you are still working and feel behind on your retirement savings, the IRS offers a powerful tax loophole exclusively for individuals aged 50 and older. You are legally allowed to make catch-up contributions to your retirement accounts and Health Savings Accounts beyond the standard annual limits. In 2026, the IRS allows you to funnel thousands of extra dollars into a 401(k) and an IRA, shielding that money from immediate taxation.

Every extra dollar you funnel into a pre-tax account lowers your current taxable income, leaving you with a significantly smaller tax bill come April. This strategy effectively forces the federal government to subsidize your retirement. Check your current payroll deductions and increase your contribution rate immediately to take full advantage of this age-based tax shelter before you exit the workforce for good.

Tip #9: Deep Discounts on Amtrak and Public Transit

Driving cross-country or navigating airport security can quickly become exhausting and expensive. Savvy seniors turn to the railway system for a comfortable, budget-friendly alternative. Amtrak provides a flat ten percent discount on most rail fares for travelers aged 65 and older. Whether you are traveling across the continent to visit your grandchildren or just riding downtown, you should never pay full price for transit.

Local transit authorities are even more generous, frequently offering half-price fares or entirely free boarding passes for older residents riding buses, subways, and commuter trains. Riding the Chicago CTA or the Pennsylvania SEPTA system can cost you absolutely nothing if you enroll in their older adult transit programs. Stop buying standard tickets at the kiosk. Apply for your local reduced-fare transit card today and always select the senior passenger option when booking your next train ticket online.

Tip #10: Unclaimed State Funds and Utility Assistance

States currently hold billions of dollars in unclaimed property, and a significant portion of those funds belongs to older Americans who simply forgot about old bank accounts, uncashed insurance checks, or utility deposits. Head over to the official unclaimed property website for your state and run a free search using your name; you might instantly find missing money. State governments make no effort to find you; you must hunt down your own cash.

Furthermore, low-income seniors can tap into the Low Income Home Energy Assistance Program to drastically cut their winter heating or summer cooling bills. Utility companies also offer their own internal relief programs, waiving late fees and lowering rates for older customers on fixed incomes. Stop struggling to pay soaring energy costs. Make a quick phone call to your power company and demand to hear about every single age-based or income-based discount they offer.

The Bottom Line: What This Means for Your Wallet

The corporate world and local governments rely heavily on your complacency to boost their profit margins and tax revenues. They actively hope you never discover these powerful benefits for seniors, preferring you continue paying full retail price until your savings run dry. By taking aggressive action and demanding the discounts you rightfully earned, you shift the financial power back into your own hands.

Every single dollar you save on property taxes, groceries, and travel is another dollar you can invest, spend on your family, or use to upgrade your lifestyle. Stop waiting for companies to offer you a better deal; they never will. Comb through your monthly expenses, apply these ten strategies, and start clawing back the money that rightfully belongs to you.

Frequently Asked Questions

Question: Do I need an AARP membership to get these discounts?

Answer: No. While paid memberships certainly offer excellent travel and dining perks, most of the strategies outlined above rely strictly on your age and your willingness to ask. Federal programs, local property tax freezes, and Medicare wellness visits are entirely independent of any private organization. You simply need a valid state-issued identification card to prove your birth date and claim your benefits.

Question: Why do companies keep these discounts hidden?

Answer: Corporations prioritize their shareholders above your financial well-being. If a telecom giant automatically lowered the bills of every customer over age 55, they would lose millions in revenue overnight. They keep these rates unadvertised so they can continue charging maximum prices to the uninformed masses. You must act as your own advocate and explicitly demand the lower senior rate.

Question: At what age do most senior benefits actually kick in?

Answer: The magic numbers vary widely depending on the institution. Some retail stores and restaurants begin offering discounts at age 55. The National Park Service requires you to be 62, while Medicare eligibility starts at 65. If you were born between 1941 and 1969, you easily clear the initial hurdles for the vast majority of these lucrative retirement programs.

Question: Will applying for utility assistance or tax freezes hurt my credit?

Answer: Absolutely not. Accessing state-mandated property tax relief or federal energy assistance programs has zero impact on your credit score. These are legislative benefits designed to protect older citizens from economic hardship—not debt vehicles. Claiming them simply lowers your cost of living without triggering any negative reporting to the major credit bureaus.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply