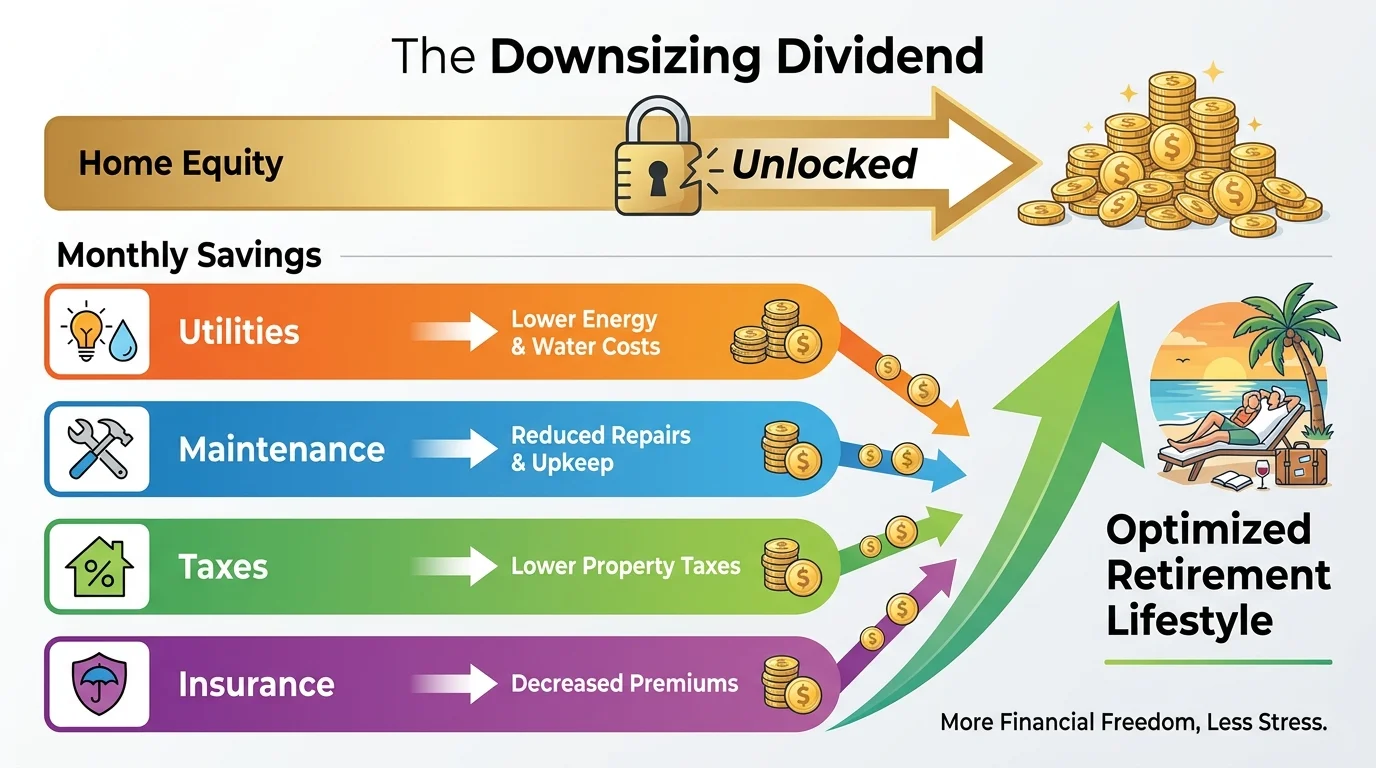

Downsizing your home is the ultimate financial lever for retirees, freeing up massive amounts of trapped home equity while dramatically reducing monthly overhead. You already know your mortgage and property tax bills will plummet when you trade a sprawling four-bedroom house for a manageable condo or patio home. The real surprise lies in the hidden budget categories that shift right under your nose. Moving to a smaller footprint completely rewires your retirement planning strategy, altering how much you spend on everything from utility bills and home maintenance to travel and entertainment. By understanding these subtle financial shifts before you pack your first moving box, you can optimize your retirement budget and keep more cash in your pocket every single month.

Tip #1: Utilities and Energy Costs

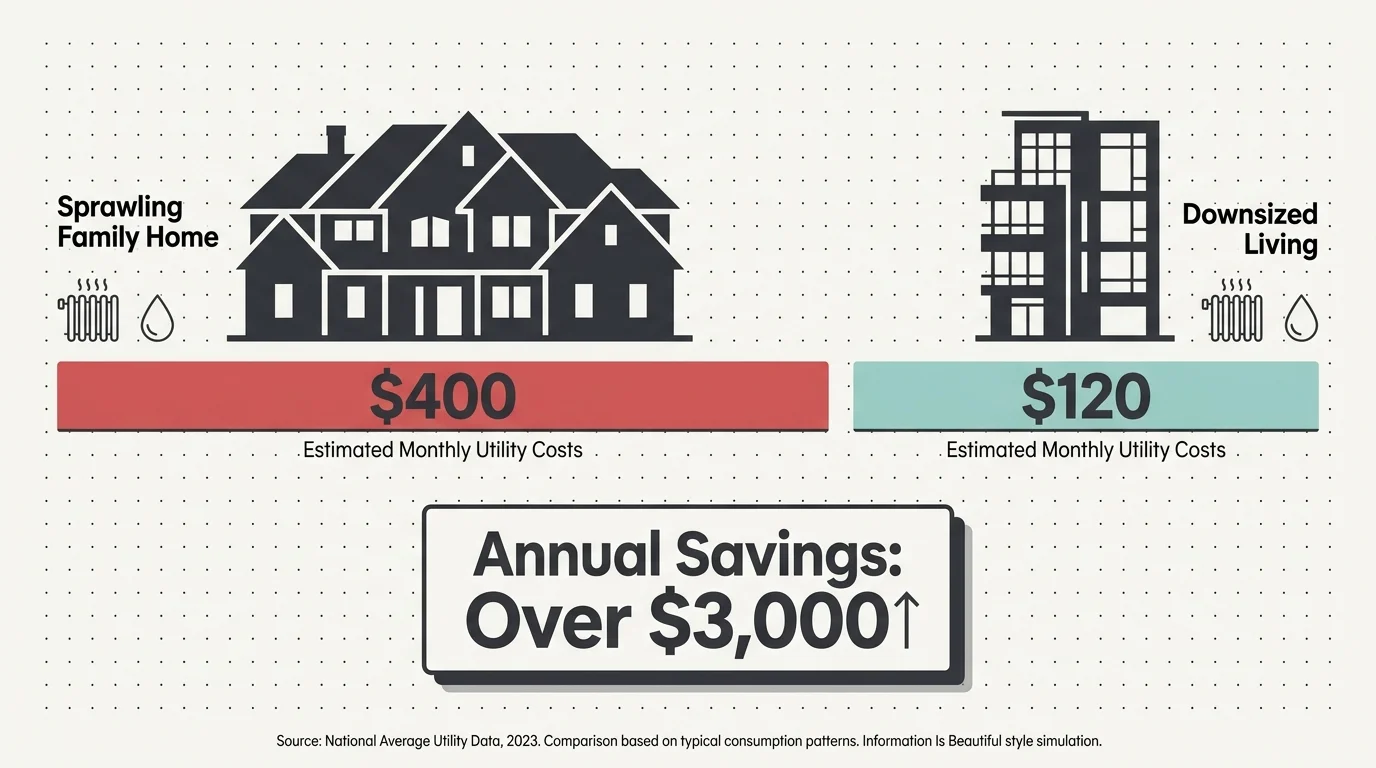

Heating and cooling a sprawling family home is an expensive endeavor, especially when you are paying to climate-control empty guest bedrooms, vaulted ceilings, and a formal dining room you use twice a year. When you downsize your living space, your utility and energy budgets undergo an immediate and drastic reduction. A smaller footprint means your HVAC system works significantly less to maintain a comfortable temperature; you simply have far less air volume to heat in the dead of winter and cool during the peak of summer.

Data consistently shows that residential utility costs run directly parallel to square footage. By cutting your home size in half, you often slash your electricity, water, and natural gas bills by a similar margin. You might comfortably drop from a crushing monthly utility burden of four hundred dollars to a highly manageable one hundred and twenty dollars. That difference alone easily leaves over three thousand dollars a year in your pocket, freeing up precious capital for investments or leisure.

Beyond the raw square footage, smaller properties tend to naturally run more efficiently. If your downsize includes a move into a condominium or a townhome, you immediately benefit from shared walls that provide incredible passive insulation against extreme external temperatures. Furthermore, downsized homes often feature modern, high-efficiency appliances and properly sealed windows that older family homes desperately lack. You completely eliminate the phantom energy drains of multiple unused electronics, ancient water heaters, and secondary refrigerators humming endlessly in the garage.

Tip #2: Home Maintenance and Repair

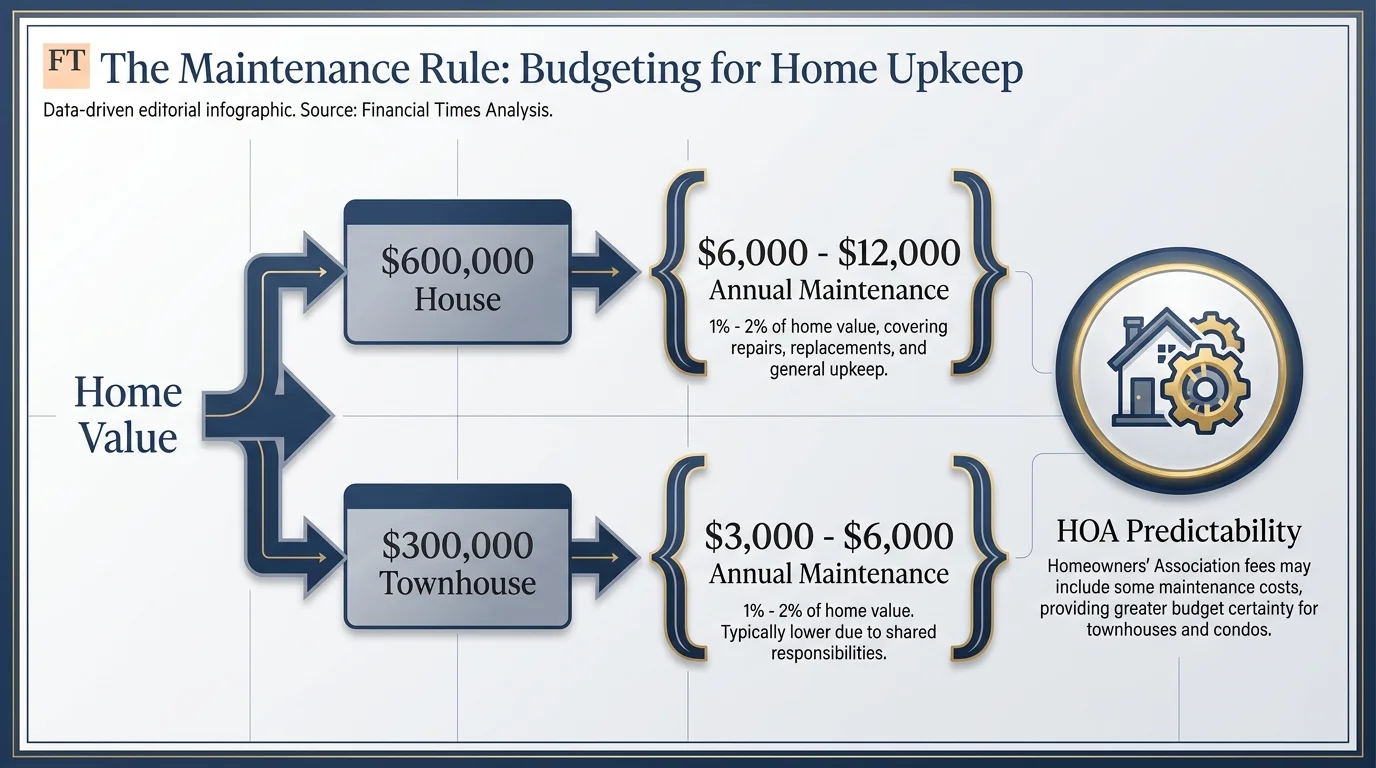

The financial drain of maintaining a large house is one of the most frustrating aspects of homeownership, but downsizing transforms this unpredictable nightmare into a manageable, predictable budget item. Financial experts generally recommend budgeting one to two percent of your home value annually for maintenance. If you own a large house valued at six hundred thousand dollars, you should theoretically set aside six to twelve thousand dollars every single year just to keep the property from falling into disrepair. Trading that massive property for a three-hundred-thousand-dollar townhouse instantly halves that hidden financial burden.

When you downsize, your weekend trips to the hardware store plummet, and your reliance on expensive contractors virtually disappears. You no longer have to worry about replacing a massive, multi-level roof or repaving a three-car driveway. The sprawling lawn that required a professional landscaping crew, expensive fertilizers, and endless irrigation is replaced by a modest patio or a community green space managed by an association.

Many retirees who downsize opt for communities with a Homeowners Association, which fundamentally changes how you budget for repairs. Instead of getting hit with a sudden ten-thousand-dollar bill for exterior painting, you pay a steady, predictable monthly fee that covers exterior maintenance, roof repairs, and landscaping. This shifts your maintenance budget from a terrifying game of Russian roulette into a boring, fixed line item that you can easily plug into your retirement planning spreadsheet.

Tip #3: Property Taxes and Homeowners Insurance

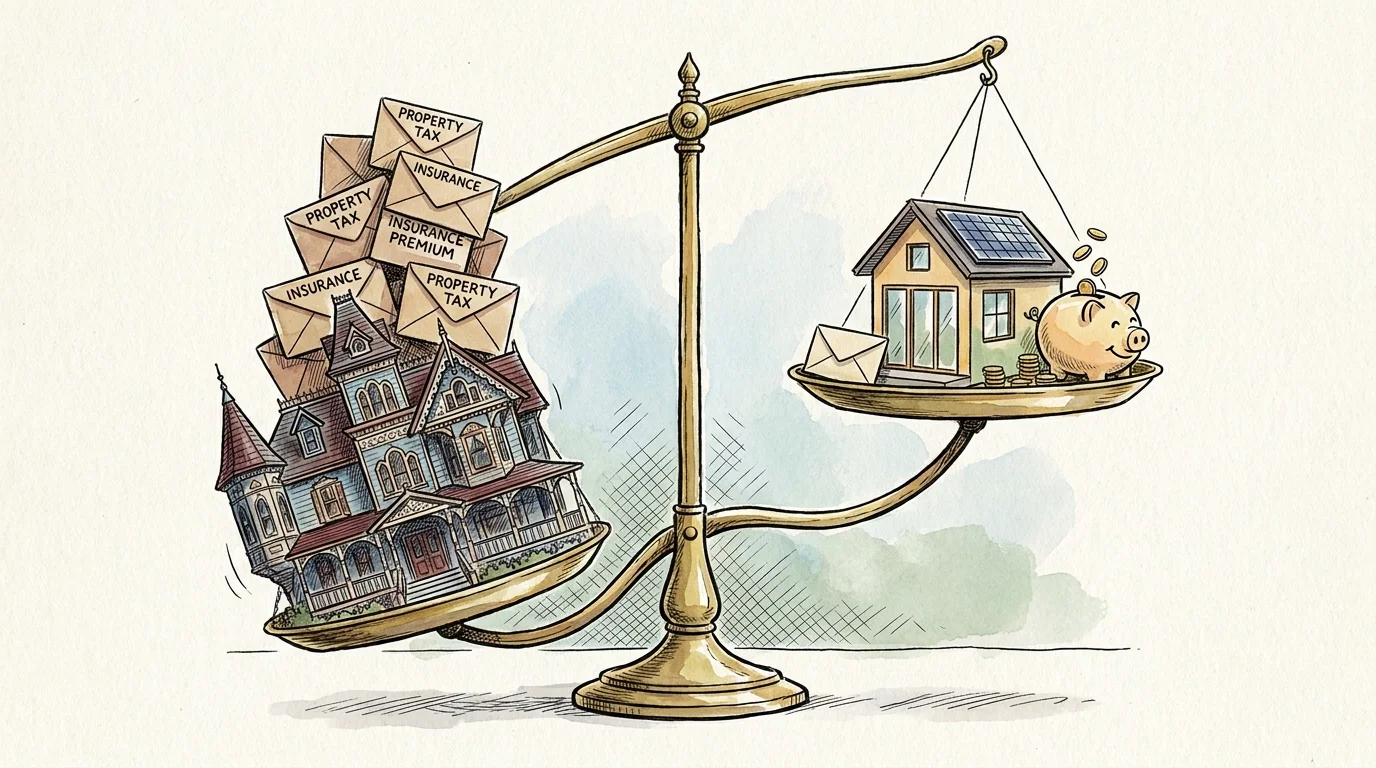

Property taxes are a persistent thorn in the side of retirees living on a fixed income, heavily dictated by the assessed value of your real estate. When you downsize to a smaller property, your assessed value naturally drops, pulling your annual property tax bill down with it. Many savvy retirees take this budget hack a step further by downsizing across state or county lines, specifically targeting municipalities that offer aggressive property tax freezes or substantial exemptions for senior citizens.

Your homeowners insurance premium experiences a similar freefall. Insurance companies calculate your premium based heavily on the “dwelling coverage” limit—the estimated cost to completely rebuild your home from the ground up in the event of a total loss. Rebuilding a sprawling three-thousand-square-foot house requires massive amounts of lumber, roofing, and labor. Rebuilding a cozy twelve-hundred-square-foot cottage requires a fraction of those resources, meaning your insurance carrier takes on significantly less risk.

If you downsize into a condominium, the insurance savings become even more pronounced. In a condo building, the association’s master policy covers the exterior structure and common areas; you only need an “HO-6” policy to cover the interior walls and your personal property. These interior-only policies are notoriously cheap, often costing hundreds of dollars less per year than a traditional single-family home insurance policy. This is guaranteed cash flow you can seamlessly redirect into your retirement fun money.

Tip #4: Transportation and Vehicle Upkeep

Most Americans do not realize how deeply their housing choice impacts their transportation budget until they move. Downsizing frequently involves relocating from sprawling, car-dependent suburbs to denser, more walkable communities or neighborhoods closer to essential amenities. When the grocery store, pharmacy, and your favorite coffee shop are a five-minute drive—or even a short walk—away, your annual mileage drops like a stone.

This reduction in driving creates a domino effect of financial savings. You spend significantly less money at the gas pump every month, but the hidden savings lie in vehicle depreciation and maintenance. Driving fewer miles means you stretch the time between expensive oil changes, brake pad replacements, and buying new sets of tires. When you report your lower annual mileage to your auto insurance provider, you can often negotiate a reduced premium based on your decreased risk of being involved in an accident.

For many downsizing couples, this lifestyle shift opens the door to the ultimate transportation hack: selling the second car. Maintaining two vehicles in retirement is often an unnecessary luxury that drains thousands of dollars a year in registration fees, insurance, and maintenance. Downsizing to a walkable neighborhood or a retirement community with transit shuttles makes living with one car entirely feasible, unlocking massive monthly savings and a quick infusion of cash from the sale of the vehicle.

Tip #5: Furniture Replacements and Interior Decor

Large houses carry a hidden psychological cost that financial planners rarely discuss: the empty room tax. When you have extra guest bedrooms, massive living areas, and formal dining spaces, you feel an overwhelming societal pressure to fill them with furniture, rugs, wall art, and knick-knacks. You end up spending thousands of dollars decorating spaces that you only walk through to dust.

Downsizing imposes a physical boundary on your spending habits; you simply cannot buy more stuff because you have nowhere to put it. This forced minimalism acts as a powerful safeguard for your retirement budget. You stop casually browsing furniture stores on the weekends because your new home is already perfectly outfitted with your favorite, most essential pieces.

While your ongoing decor budget will permanently shrink, you do need to plan for a temporary spike in this category immediately following your move. Your massive sectional sofa from your old suburban basement might not fit through the door of your new patio home, and your oversized dining table could suffocate your new, smaller eating area. Smart retirees budget a few thousand dollars upfront for scale-appropriate, multi-functional furniture, knowing that once the house is set up, their lifelong interior design expenses will practically drop to zero.

Tip #6: Travel and Lock-and-Leave Vacations

Not all budgets decrease when you downsize; some actually expand to dramatically improve your quality of life. For many retirees, the travel and leisure budget swells significantly after moving to a smaller home. By slashing your monthly carrying costs—such as utilities, taxes, and maintenance—you generate a steady stream of surplus cash flow. Instead of funneling your hard-earned money into a new roof or a massive air conditioning unit, you can redirect those funds toward cruises, international flights, and cross-country road trips.

Furthermore, smaller homes—particularly condos, townhomes, and properties within gated communities—offer unparalleled “lock-and-leave” security. When you lived in a large, standalone house, taking a month-long vacation meant hiring someone to mow the lawn, collect the mail, check for burst pipes, and ensure the property wasn’t targeted by burglars. These services easily added hundreds of dollars to the cost of any extended trip.

When you downsize into a managed community, you completely eliminate these logistical headaches and their associated costs. The landscaping is handled by the association, the exterior is secure, and close neighbors provide natural surveillance. You can simply lock your front door, head to the airport, and enjoy your travels without paying a premium to keep your empty house running smoothly.

Tip #7: Healthcare and Aging-in-Place Modifications

Your future healthcare and mobility budget is heavily dictated by the architecture of your home. A sprawling, multi-level house with sunken living rooms, steep driveways, and narrow doorways is an expensive hazard waiting to happen as you age. Modifying a traditional family home to accommodate mobility issues requires staggering capital; installing custom stairlifts, widening hallways, and retrofitting full bathrooms on the ground floor can easily consume tens of thousands of dollars.

Downsizing proactively neutralizes these future expenses. Smart retirees target single-story homes, ground-floor condominiums, or buildings with reliable elevator access. By choosing a property with an open floor plan, zero-step entryways, and walk-in showers right from the start, you permanently cross expensive accessibility renovations off your long-term retirement budget.

Additionally, the location of your downsized home can actively reduce your daily health and wellness expenses. Many modern downsizing communities feature robust amenities designed specifically for active adults. Access to heated community pools, on-site fitness centers, and paved walking trails completely replaces the need for expensive private gym memberships. Better cardiovascular health through easy access to these amenities translates directly to lower out-of-pocket medical costs, fewer prescription medications, and a more vibrant retirement.

Tip #8: Entertaining and Dining Habits

Your grocery and entertainment budgets undergo a fascinating transformation when you surrender your massive kitchen and formal dining room. In a large family home, you are naturally positioned as the default host for chaotic Thanksgiving dinners, massive holiday parties, and endless weekend barbecues. Feeding thirty people requires bulk grocery runs, expensive cases of alcohol, and an arsenal of catering supplies that quietly drain your checking account.

When you move to a smaller space, hosting mega-events becomes physically impossible. Your entertainment budget seamlessly shifts away from bulk hosting toward more intimate, manageable experiences. Instead of spending five hundred dollars on groceries and drinks for a massive neighborhood block party, you can afford to treat two close friends to a beautiful dinner at an upscale local restaurant.

This physical limitation encourages you to enjoy your local community more fully. Without a massive backyard to maintain or a huge kitchen to clean, you have the time and energy to meet friends at local cafes, explore new bistros, or host simple wine-and-cheese nights on your modest patio. Your overall food and entertainment budget stabilizes, focusing your spending on high-quality interactions rather than high-quantity catering.

The Bottom Line: What This Means for Your Wallet

Downsizing is not just a real estate transaction; it is a total lifestyle budget rewrite that actively defends your retirement nest egg. By trading wasted space for highly efficient, manageable living quarters, you systematically dismantle the heavy financial machinery required to keep a large home running. Your monthly cash flow becomes liberated from exorbitant heating bills, brutal property tax assessments, and the endless treadmill of preventative maintenance.

The secret to maximizing this financial transition is recognizing that your spending habits must evolve alongside your square footage. The money you previously surrendered to your local utility provider and landscaping crew can now be forcefully redirected toward experiences that actually enhance your retirement years. By embracing the forced frugality of a smaller footprint, you secure a financial buffer that protects you against inflation, market volatility, and the rising costs of healthcare, ensuring your money outlasts your lifespan.

Frequently Asked Questions

Does a Homeowners Association fee cancel out the financial savings of downsizing?

Many retirees worry that a steep HOA fee will destroy their newly optimized budget, but this is usually a mathematical illusion. When you analyze your current spending on a large home, you are likely already paying for the services an HOA provides; you just pay them to separate vendors. When you add up your current expenses for lawn care, gutter cleaning, exterior painting, roof repair sinking funds, and gym memberships, that total almost always exceeds a standard monthly HOA fee. An HOA simply consolidates these unpredictable expenses into one fixed, predictable monthly bill, which actually stabilizes your retirement budget.

When is the best time to downsize for maximum budget impact?

The most financially devastating mistake retirees make is waiting too long to downsize. The optimal time to make the move is while your current home is still in pristine condition and before major capital expenses hit. If you know your sprawling home will need a twenty-thousand-dollar roof replacement or a completely new HVAC system within the next three years, you should aggressively plan to sell before those bills come due. Downsizing early allows you to preserve that cash and let the next buyer assume the heavy maintenance liabilities.

Are there hidden costs to downsizing I should budget for immediately?

Yes, the transaction itself requires a short-term cash outlay that you must plan for. You will need to account for real estate agent commissions, closing costs, and professional moving fees. Furthermore, as discussed in the furnishings section, you may need to purchase specific, scale-appropriate furniture to make your smaller home functional. However, these are strictly one-time, upfront costs. The long-term, permanent reduction in your monthly carrying costs will easily recover these initial expenses within the first few years of living in your new, efficient home.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply