Stepping away from the daily grind forces a massive reset in how you manage cash, and ditching the financial drain of working years is the ultimate retirement hack. You stop bleeding money on things that no longer serve your lifestyle and start maximizing the dollars that bring peace. Society pushes endless consumption, but savvy seniors quickly realize real wealth lies in keeping more of what they saved. Making these frugal retirement lifestyle changes drastically improves your monthly budget. You trade mindless routines for intentional spending, discovering that letting go of luxuries feels entirely liberating. Prepare to cut the fat from your ledger as we explore the priciest everyday behaviors successful retirees happily abandon forever.

Tip #1: Trading in Cars Every Few Years

The dealership trap keeps millions of working Americans broke, but walking away from your career means walking away from the need to impress anyone in the company parking lot. New cars lose roughly twenty percent of their value the moment you drive them off the lot. During your career, you likely justified this brutal depreciation because you required ultra-reliable transportation for the daily commute. Once you stop working, that justification vanishes immediately. Your annual mileage plummets, making a constant rotation of brand-new vehicles a massive waste of capital.

Instead of absorbing crippling depreciation and high insurance premiums, you can easily keep your current vehicle running smoothly for a decade or more. Modern vehicles frequently surpass 150,000 miles with nothing more than basic routine maintenance and timely fluid changes. When you calculate the true cost of an auto loan—including the hidden dealership fees, state taxes, and interest rates—you quickly realize that holding onto an older car frees up thousands of dollars every single year.

You gain absolute financial freedom when you completely eliminate a monthly car payment. Redirect those freed-up funds toward experiences that actually matter, like extensive travel or funding a grandchild’s college account. Savvy individuals completely ignore the aggressive dealership marketing hype and drive their paid-off vehicles until the wheels literally fall off.

Tip #2: Subsidizing Adult Children

Financial umbilical cords drain your nest egg faster than prolonged stock market downturns. Paying for your adult children’s cell phone plans, streaming accounts, and auto insurance policies might feel supportive, but it actively sabotages your own financial security. You worked decades to build your portfolio; you cannot afford to jeopardize your ultimate peace of mind by funding another capable adult’s discretionary lifestyle.

One of the most critical habits seniors give up often involves this silent family welfare system. Cutting off the financial faucet forces your children to become independent—all while protecting your fixed income from unnecessary leakage. Have a direct, transparent conversation with your family about your new, stricter budget parameters. Give them a firm, non-negotiable deadline to assume total responsibility for their own recurring bills.

The initial transition may cause slight friction, but the long-term emotional and financial payoff is profound. You reclaim hundreds of dollars a month to deploy exactly as you see fit. More importantly, you eliminate the toxic underlying resentment that builds when you sacrifice your hard-earned retirement comfort to subsidize unnecessary spending for fully grown adults.

Tip #3: Keeping Bloated Cable Packages

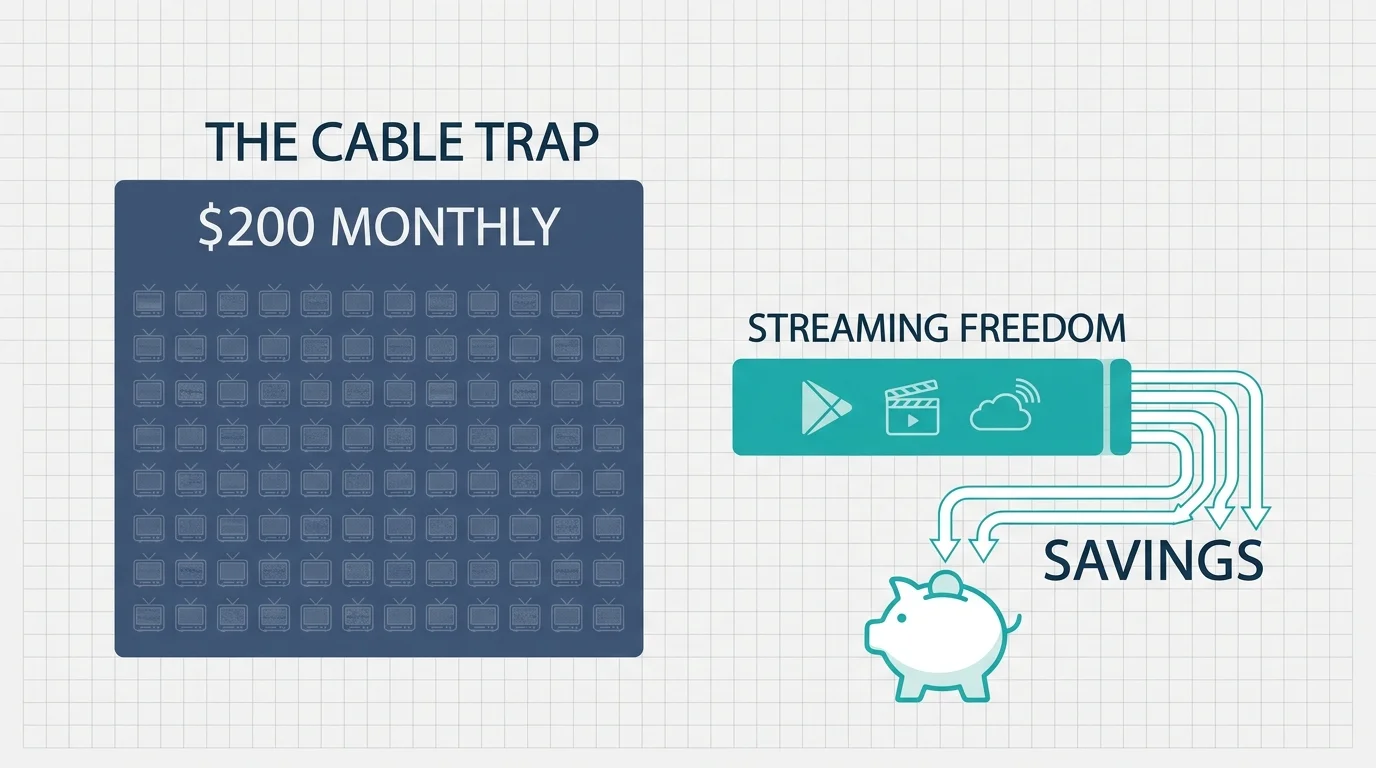

Cable television providers rely heavily on your inertia to extract maximum corporate profits. They bundle hundreds of useless channels together, inflate the standard pricing with hidden broadcast fees, and lock you into archaic, expensive contracts. One of the most common expensive habits retirees quit is handing over two hundred dollars or more every month for programming they never even watch.

You immediately regain control of your entertainment budget the minute you finally cut the cord. Modern streaming platforms offer far superior, ad-free content at a fraction of the cost, allowing you to subscribe to specific services only when they release shows you actually want to see. You can easily rotate through Netflix, Hulu, and premium networks one month at a time, instantly canceling the subscription when you finish binge-watching a specific series.

Do not overlook the sheer power of a high-definition digital antenna. You can reliably capture local news, major sports broadcasts, and prime-time network television completely free of charge. You keep the television experience you enjoy without funding the bloated corporate infrastructure of legacy cable monopolies.

Tip #4: Dining Out Just for Convenience

Grabbing fast food or takeout on the way home from a chaotic day at the office used to be a basic survival tactic. You happily traded money for time because your demanding career consumed all your physical energy. Now that your schedule belongs entirely to you, paying a premium markup for mediocre restaurant food makes absolutely zero financial sense.

You must actively stop spending retirement funds on overpriced convenience meals that offer absolutely no culinary joy. When you possess the luxury of infinite time, preparing fresh meals at home becomes a rewarding daily ritual rather than a stressful evening chore. You tightly control the ingredients, slash your daily caloric intake, and retain the massive profit margins that commercial restaurants charge for basic ingredients.

This deliberate shift transforms dining out from a thoughtless default action into a highly anticipated celebration. You allocate your restaurant budget toward high-quality culinary experiences rather than sad, lukewarm drive-thru lunches. Reserving your dining dollars for truly exceptional meals guarantees you get maximum value, flavor, and enjoyment out of every single penny you choose to spend.

Tip #5: Carrying Unnecessary Life Insurance

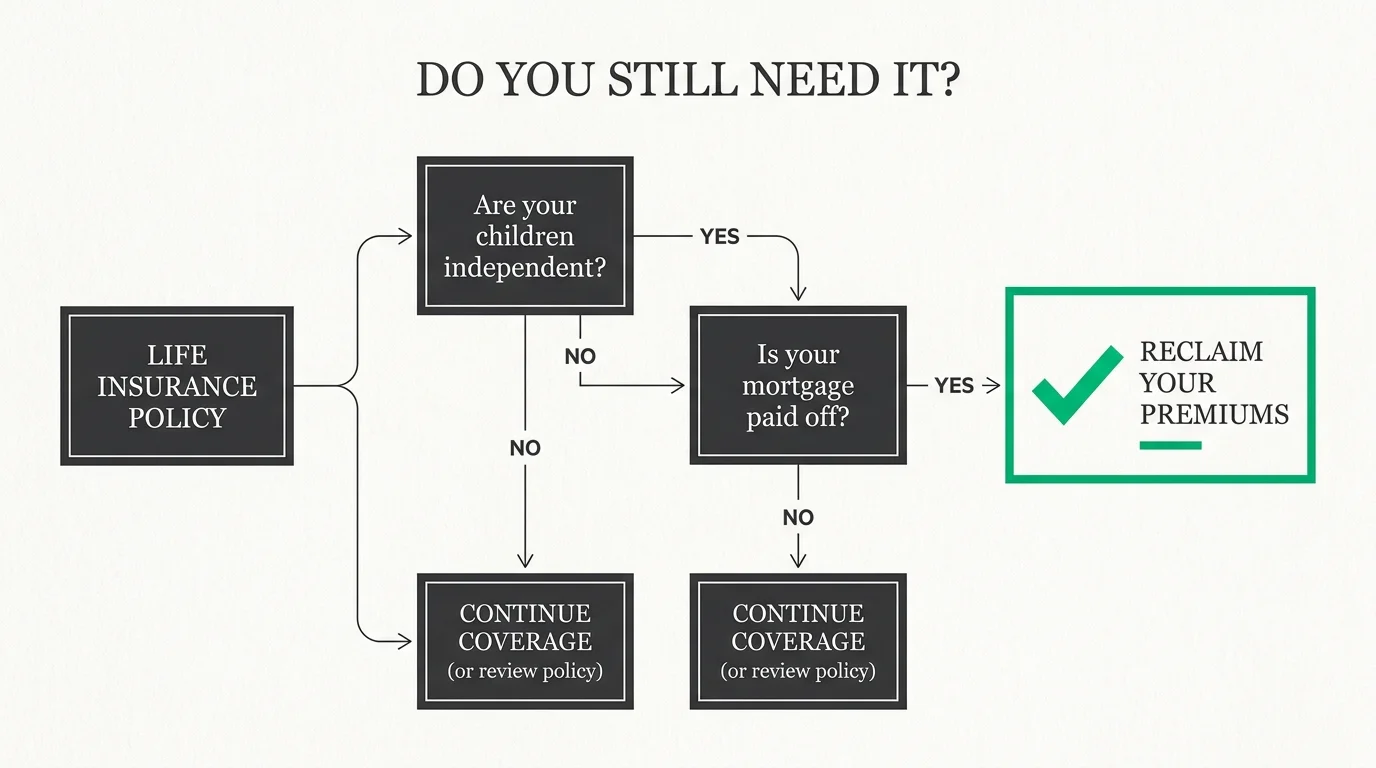

Commission-hungry insurance agents heavily push permanent life insurance products, but these complex policies rarely serve a practical purpose once you step away from your job. If your mortgage is fully paid off, your children are self-sufficient adults, and your spouse has adequate survivor benefits from your investment portfolio, you no longer need to insure your income stream. The financial risk associated with your sudden passing has drastically decreased.

Clinging to expensive whole life policies ties up vital cash flow that you could actively deploy in your daily life. You pay exorbitant monthly premiums primarily to fund administrative fees and agent commissions rather than building accessible, liquid wealth. Savvy financial managers ruthlessly audit their existing coverage and cancel the outdated policies that no longer align with their current reality.

Consult an independent fee-only financial planner to objectively evaluate your specific insurance situation. You might happily discover that surrendering a permanent life policy yields a substantial cash value payout. Reinvesting those liberated funds into a low-cost index fund or simply using them to enhance your current travel budget provides far more utility than leaving a padded death benefit behind.

Tip #6: Maintaining an Oversized Empty Nest

Clinging to a massive four-bedroom suburban house ranks high among the most detrimental financial choices you can make. You pay thousands of dollars annually to heat, cool, clean, and formally insure rooms that remain completely empty for eleven months out of the year. The deep emotional attachment to your family home often blinds you to the staggering ongoing costs of preventative maintenance and ever-rising property taxes.

Downsizing seamlessly frees up an enormous amount of trapped home equity. Selling the oversized property allows you to purchase a smaller, vastly more efficient home outright while injecting a massive cash lump sum directly into your primary retirement portfolio. You instantly lower your monthly utility bills, slash your property tax burden, and completely reduce the physical toll of constant, agonizing home upkeep.

Moving into a right-sized space dramatically improves your daily quality of life. You spend significantly fewer hours pushing a heavy vacuum and more time engaging in fulfilling hobbies, traveling the globe, or simply relaxing on your patio. A smaller footprint forces you to ruthlessly declutter your possessions, resulting in a streamlined, peaceful environment that perfectly supports your new chapter.

Tip #7: Paying Top Dollar for Peak Season Travel

The relentless corporate world forces you to travel during the absolute most expensive windows of the calendar year. You battle sweaty summer crowds, navigate packed airport terminals during school holidays, and pay maximum rack rates for basic hotel accommodations. Retirement completely shatters those scheduling constraints, giving you the ultimate superpower of profound flexibility.

You drastically reduce your vacation expenses by fully embracing shoulder-season travel. Flying on a random Tuesday in late September or booking a comprehensive European tour in early May easily slashes your costs by fifty percent or more. You encounter far fewer annoying tourists, enjoy significantly milder weather, and receive far better service from local hospitality workers who are not overwhelmed by peak-season chaos.

Leveraging this flexibility also allows you to capitalize quickly on last-minute cruise deals and sudden airline flash sales. You no longer need to submit formal vacation requests to an aggressive boss months in advance. Keeping your travel plans fluid ensures you stretch your discretionary budget to the absolute limit, allowing you to take three exceptional trips for the precise cost of one poorly timed summer excursion.

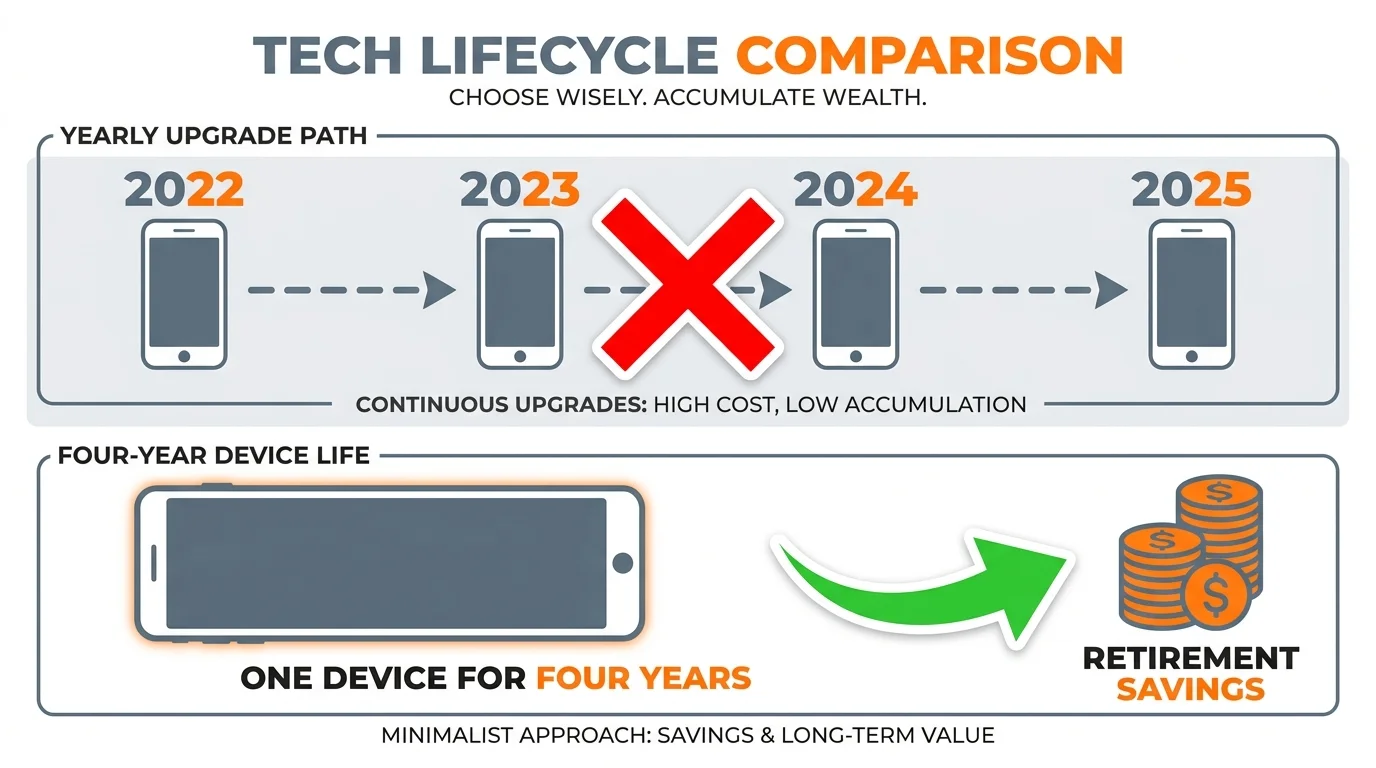

Tip #8: Upgrading Tech Gadgets Annually

The monolithic tech industry engineers an artificial sense of urgency to keep you trapped permanently on the endless upgrade treadmill. Smartphone manufacturers roll out nearly identical devices every single year, aggressively marketing marginal camera improvements as revolutionary technological breakthroughs. If you want to save money quit habits that force you to finance twelve-hundred-dollar phones simply to check your daily email and send basic text messages.

Modern electronics boast incredibly long lifespans when they are properly handled and maintained. A high-end smartphone purchased three full years ago possesses more raw computing power than you will ever practically utilize; you simply need to replace the degraded lithium battery for fifty dollars instead of financing an entirely new flagship device at top dollar.

Extending the standard lifecycle of your laptops, tablets, and mobile phones keeps a highly significant amount of cash safely in your checking account. You simply ignore the flashy keynote presentations and the predatory carrier promotional traps that lock you into endless monthly payment plans. Use your technology until it fundamentally fails to operate, and you will easily capture the true intrinsic value of your initial electronic investment.

Tip #9: Outsourcing Simple Home and Lawn Maintenance

Hiring professional services to mow the front lawn, power wash the concrete driveway, and deep clean the interior rooms makes perfect sense when you work sixty grueling hours a week. Severe time poverty forces you to throw heavy cash at basic domestic chores. However, retaining these expensive outside contractors during retirement simply drains your monthly cash flow for no legitimate reason whatsoever.

Taking over these straightforward manual tasks provides immediate financial relief and delivers excellent physical benefits. Pushing a standard lawnmower, pulling garden weeds, and painting a faded spare bedroom keeps you highly active, mentally engaged, and physically mobile. You completely transform necessary property maintenance into a highly productive daily workout that simultaneously protects your portfolio from unnecessary cash withdrawals.

Reserve your precious contractor budget exclusively for highly specialized or strictly dangerous jobs involving electrical work, major plumbing repairs, or elevated roof maintenance. Handling the basic, ground-level upkeep yourself safely reinstills a profound sense of personal pride in your property. You directly manage your physical environment and retain total, uncompromising control over the exact quality of the work being performed.

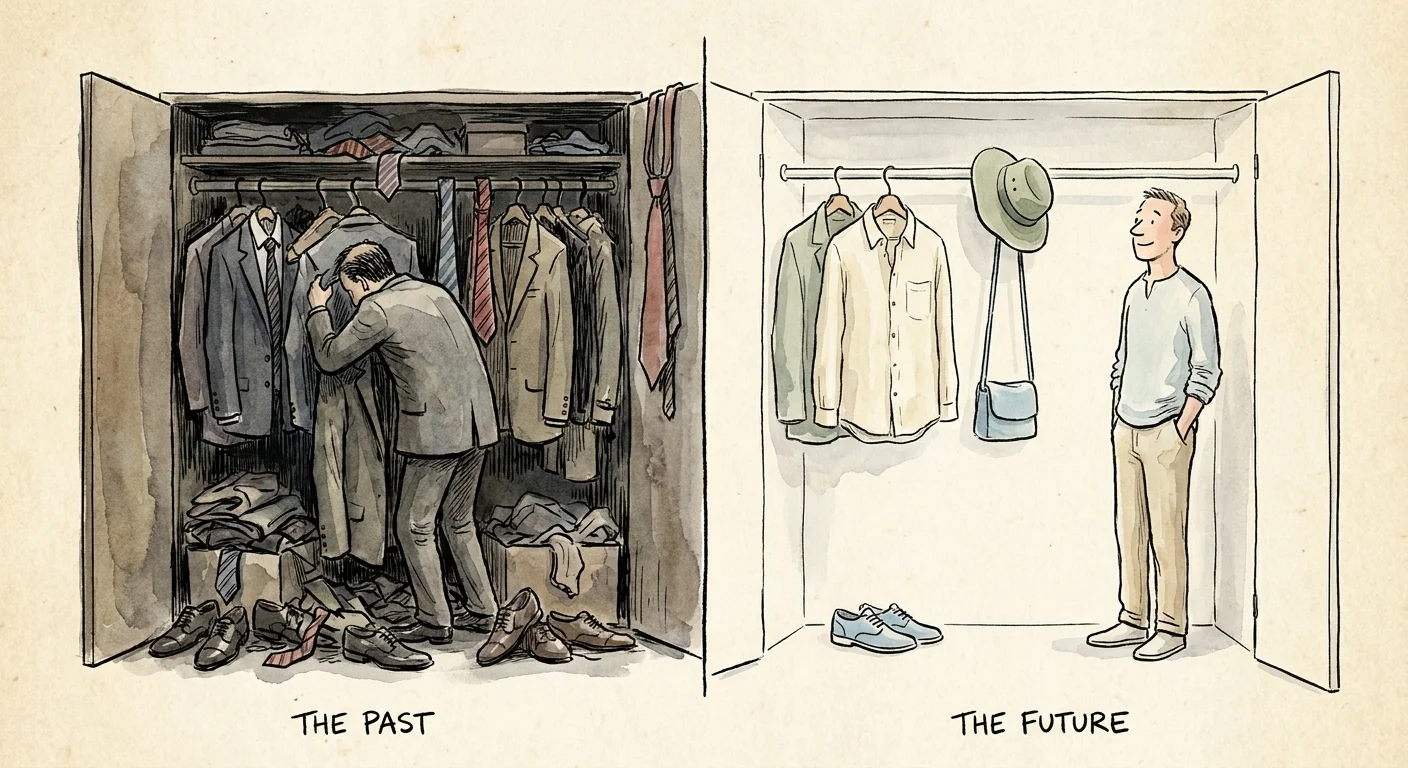

Tip #10: Buying Fast Fashion and Formal Work Wardrobes

The professional corporate world imposes a massive hidden tax in the form of an extensive, high-maintenance wardrobe. You spend decades routinely purchasing expensive tailored suits, formal dresses, and trendy seasonal pieces simply to project the right corporate image. The associated premium dry-cleaning bills quietly siphon hundreds of dollars from your checking account every single year.

Walking away from the office permanently instantly eliminates this ridiculous financial burden. You successfully pivot toward high-quality, exceptionally comfortable, and durable clothing that requires absolutely zero specialized maintenance. You ruthlessly purge the restrictive garments that require professional chemical pressing, opting instead for highly versatile fabrics you can easily wash and dry right at home.

This massive lifestyle shift naturally curtails the toxic urge to chase fast fashion trends. You slowly build a curated, minimalist collection of classic clothing pieces perfectly suited for active travel, casual recreation, and daily relaxation. Eliminating the constant, expensive churn of your personal closet saves thousands of dollars over the course of your retirement while radically simplifying your morning routine.

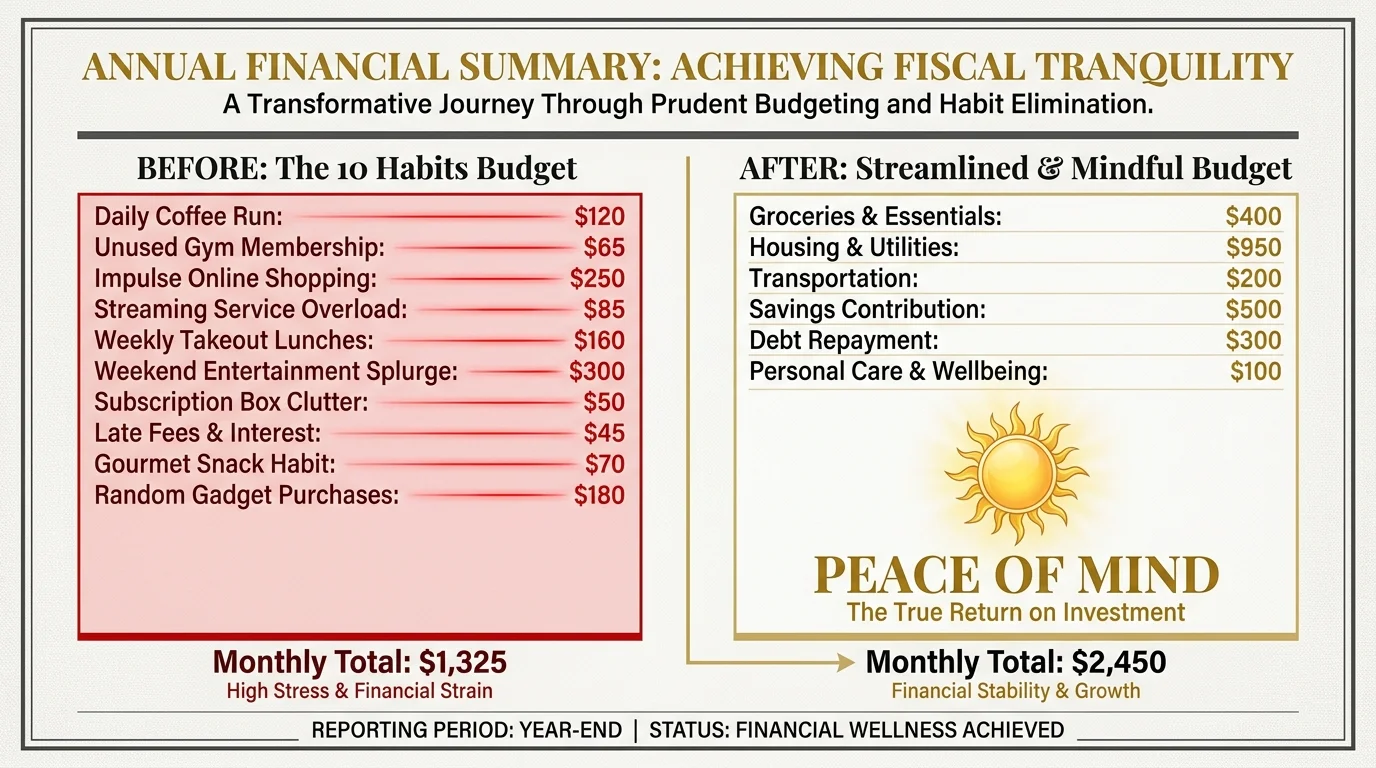

The Bottom Line: What This Means for Your Wallet

Successfully navigating your post-career years requires a brutally honest assessment of your historic spending triggers. The consumer habits that defined your working decades quickly act as heavy financial anchors when you transition to a strict fixed income. Severing these costly ties is not about needlessly depriving yourself; it is about aggressively reallocating your limited resources toward the exact things that genuinely elevate your daily existence.

Every single dollar you effectively claw back from inflated cable bills, unnecessary insurance premiums, and rapidly depreciating assets translates directly into increased personal freedom. You quickly gain the unshakeable power to weather unpredictable economic fluctuations and unexpected medical costs without a hint of panic. Taking highly proactive control of your financial outflows guarantees that your hard-earned savings will easily outlast your lifespan, providing you with absolute, undeniable peace of mind.

Frequently Asked Questions

Do I really need to cancel my life insurance if I have had it for twenty years?

You must objectively evaluate the core purpose of the life insurance policy today. If you originally purchased the insurance coverage to replace your working income and financially protect your minor children, that specific need has likely evaporated. Holding onto an expensive permanent policy strictly because of the emotional sunk cost fallacy is a profound financial mistake. Consult a fee-only fiduciary to determine if immediately surrendering the policy for its built-up cash value provides a vastly better strategic advantage for your current lifestyle.

How do I cut off my adult children financially without ruining our relationship?

Direct communication and strict timeline management are your absolute most effective tools. You must calmly explain that aggressively protecting your retirement funds ensures you will never unexpectedly become a heavy financial burden to them later in life. Provide a firm, totally non-negotiable date—usually three to six months out—when you will permanently stop paying their recurring monthly bills. This highly generous window gives them ample opportunity to adjust their own personal budgets and assume total adult responsibility for their expenses.

Is it truly worth the physical hassle of selling my family home and downsizing?

The raw arithmetic heavily favors aggressive downsizing for the vast majority of modern retirees. Selling an oversized, aging property instantly unlocks massive amounts of trapped home equity while drastically reducing your ongoing monthly carrying costs. While the physical process of packing up and moving certainly requires heavy effort, the permanent, long-term reduction in local property taxes, utility bills, and basic maintenance expenses permanently improves your available cash flow and significantly lowers your daily stress levels.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply