You want to collect Social Security early and keep working, but a hidden penalty could temporarily slash your monthly checks. The Social Security earnings test targets beneficiaries who claim before their full retirement age while continuing to clock in at work. Earning above a specific threshold triggers mandatory benefit withholding, derailing your cash flow and catching thousands of early retirees off guard. Fortunately, you can outsmart this bureaucratic hurdle by mastering the exact limits, understanding how the math works, and leveraging the rules to your advantage. Stop guessing how your paycheck impacts your benefits. Here is exactly what you need to know to maximize your income without accidentally sacrificing your hard-earned Social Security money.

Tip #1: Know the Exact Earnings Test Numbers for the Current Year

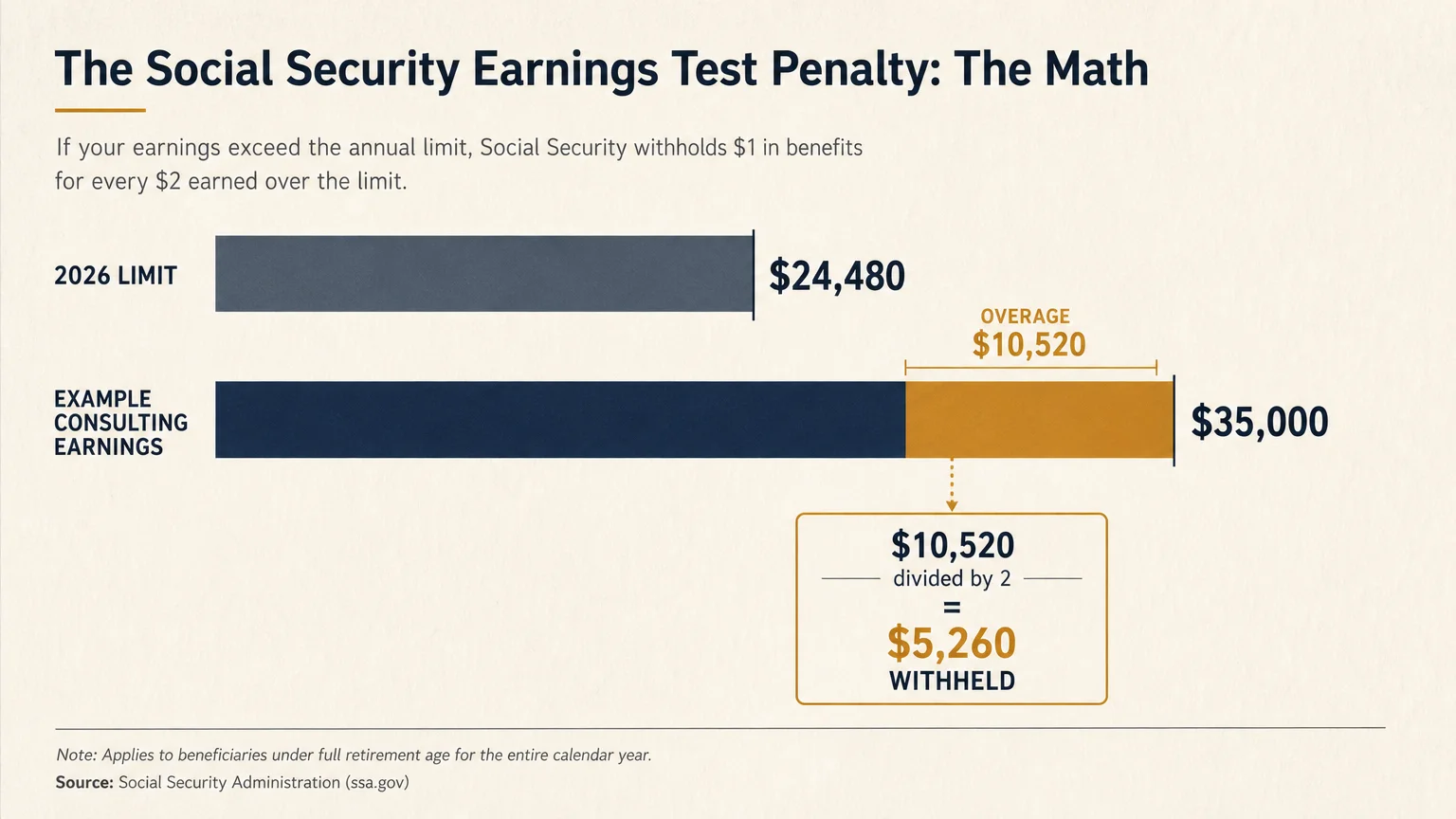

If you claim Social Security at age 62, the government immediately places a ceiling on how much you can earn from a job. For 2026, the strict earnings test limit is $24,480 if you will remain under your Full Retirement Age (FRA) for the entire calendar year [1]. This is not a polite suggestion; it is a rigid cap enforced by the Social Security Administration (SSA) [1]. Earn a penny over that specific amount, and the financial penalty kicks in immediately [1].

The penalty math is brutal but straightforward. The SSA will withhold $1 of your benefits for every $2 you earn above the $24,480 threshold [1]. Let us run the numbers with a concrete scenario. Suppose you decide to claim benefits early, but you also take a part-time consulting gig that pays you $35,000 for the year. Since your income is $10,520 above the limit, the government divides that overage in half [1]. They will systematically withhold exactly $5,260 from your benefits over the course of the year [1].

Crucially, the SSA does not just reduce your check by a few dollars each month to cover the difference. They typically hold back your entire monthly checks until the debt is completely satisfied. This aggressive collection method means you might go several months without seeing a single dime from Social Security. You must track your W-2 wages or net self-employment income meticulously. Guessing your total annual income can lead to a severe financial shock when the government realizes you earned too much and suddenly halts your monthly deposits.

Tip #2: Exploit the “Year You Reach Full Retirement Age” Loophole

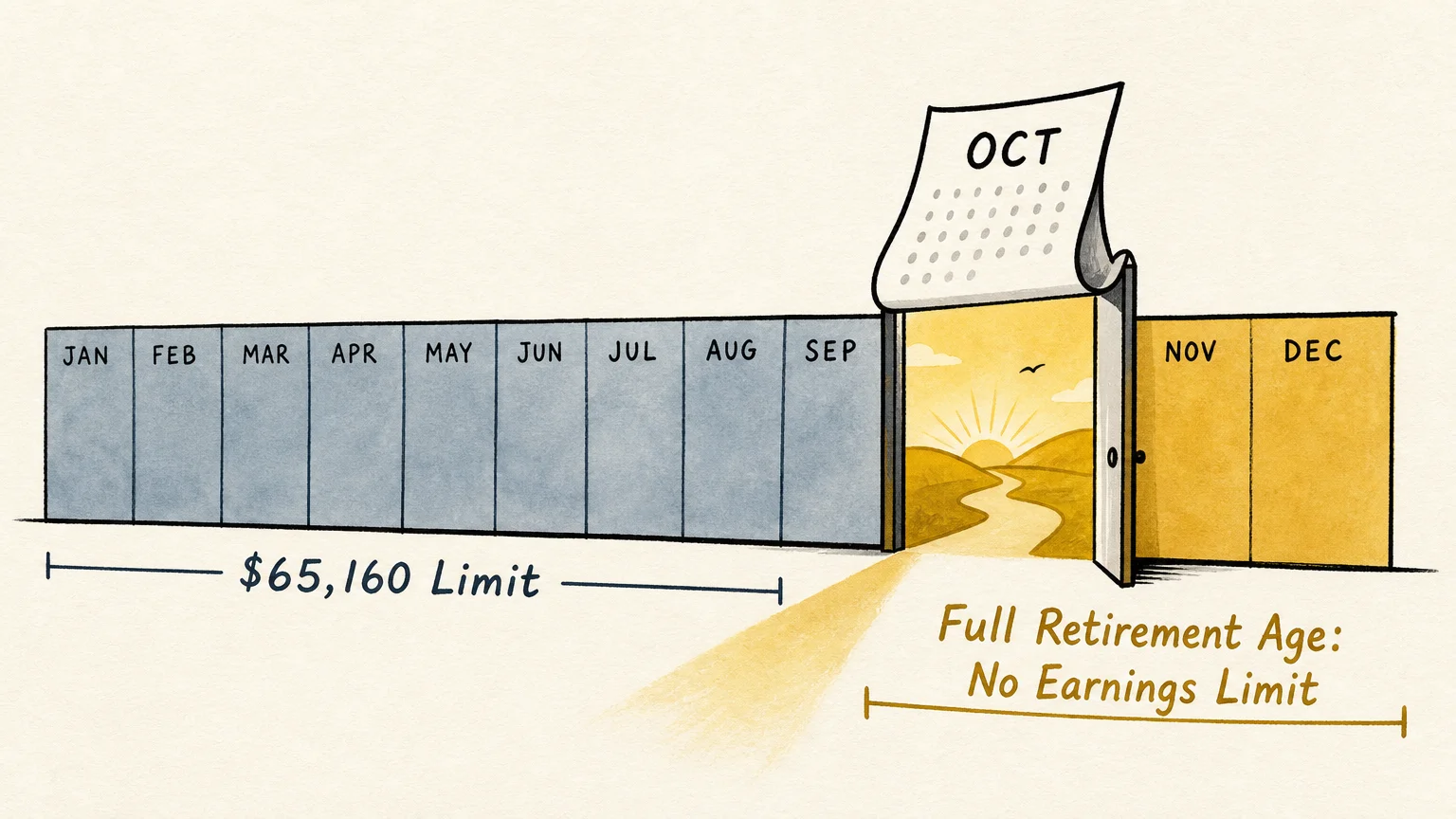

The heavy-handed penalties of the earnings test dramatically loosen in the calendar year you finally reach your Full Retirement Age. The government recognizes that you are approaching the finish line, so they raise the earnings ceiling significantly. If you will hit your FRA at any point in 2026, your earnings limit surges to a much more comfortable $65,160 [2].

Furthermore, the penalty calculation becomes much more forgiving. Instead of taking $1 for every $2, the SSA only withholds $1 for every $3 you earn above that higher threshold [2]. More importantly, this higher limit only applies to the specific earnings you make in the months before your birthday month. The exact moment the clock strikes the first day of your FRA birth month, the earnings test evaporates completely [2]. You could earn a million dollars a year as a corporate executive, and the SSA would not dock your benefit by a single cent [2].

Consider someone turning 67 in October. They only need to keep their income under the $65,160 cap from January through September. Any large bonuses, heavy sales commissions, or massive project payouts should be intentionally deferred until October or later. By strategically timing your income realization, you can completely bypass the withholding penalty while enjoying both your maximum salary and your full retirement payouts simultaneously.

Tip #3: Realize the Withheld Money Is Not Gone Forever

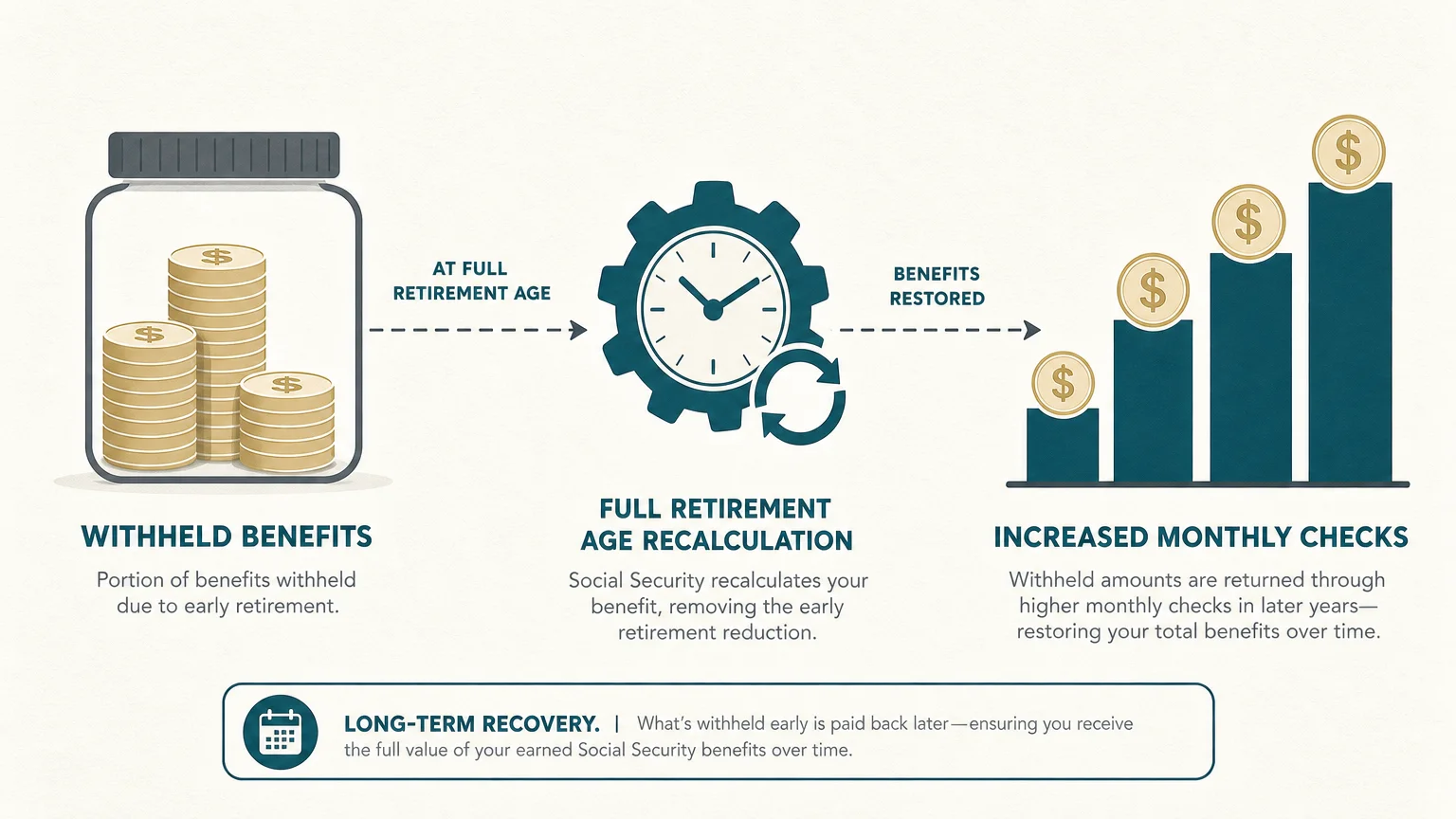

The biggest myth surrounding the Social Security earnings test is the widespread belief that the government permanently steals your money. Financial pundits often refer to the withholding limit as a “tax,” but that label is entirely false and misleading. The benefit withholding is actually a temporary deferral [3]. If the SSA holds back $15,000 of your benefits because you earned too much at age 63, that money is not lost to the bureaucratic abyss [3].

You will get it back, but it requires patience. When you finally reach your Full Retirement Age, the SSA automatically recalculates your monthly benefit amount [3]. They look back at your earnings record, identify the exact number of months your check was withheld due to the earnings test, and act as though you actively delayed claiming your benefits for those specific months [3]. The result is a permanent, upward adjustment to your monthly payout for the rest of your life [3].

Over the remainder of your retirement, those slightly larger checks will slowly refund the money that was withheld. The breakeven point typically takes about 10 to 15 years, depending on your exact claiming age and specific benefit amount [3]. Therefore, while hitting the earnings limit creates an immediate cash flow crunch that hurts your wallet today, it actually forces a delayed gratification strategy that mathematically boosts your long-term guaranteed retirement income.

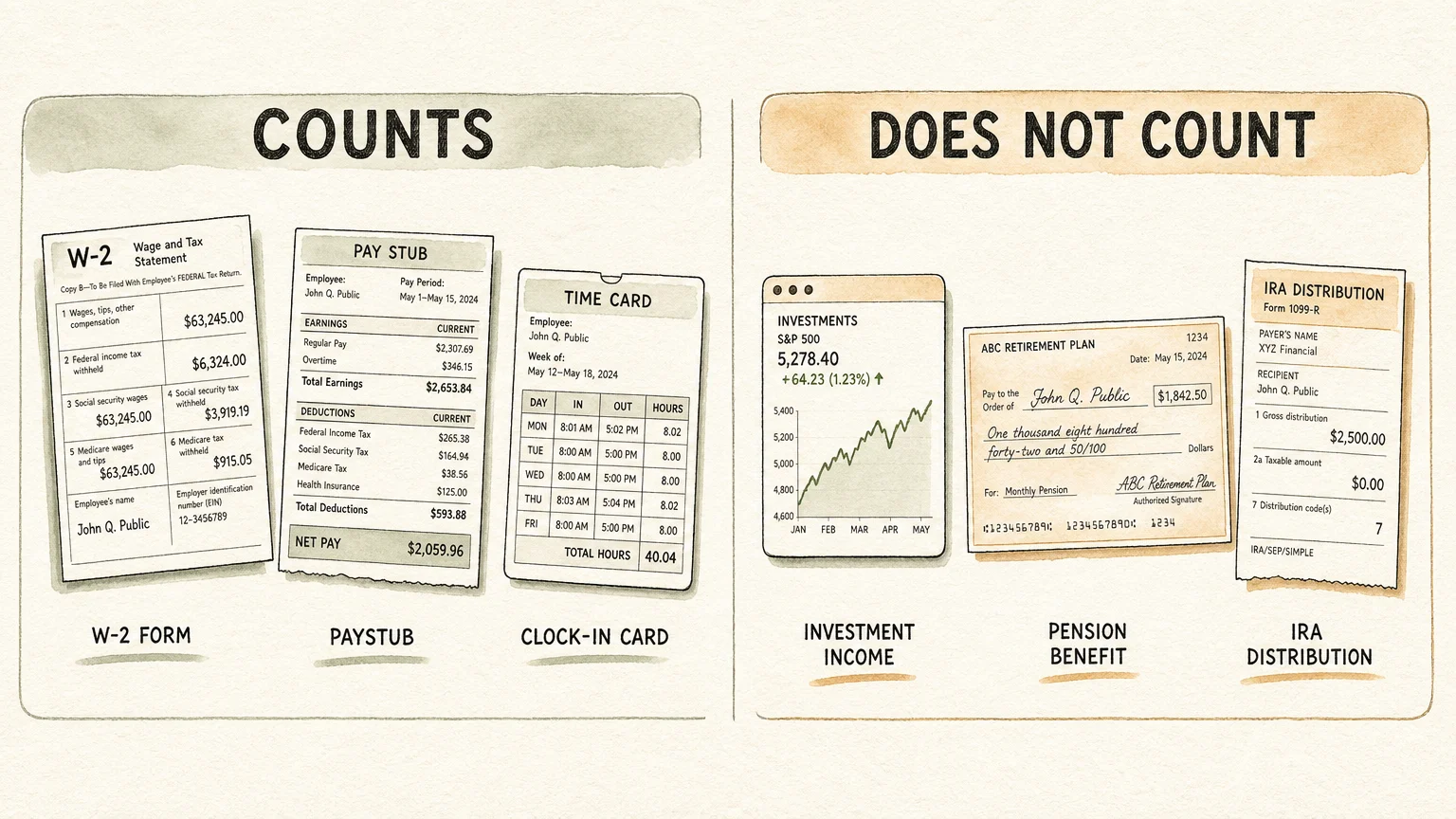

Tip #4: Identify Exactly What Counts as “Earnings”

One of the most common ways Americans accidentally sabotage their retirement budget is by fundamentally misunderstanding what the SSA considers “income.” The earnings test is strictly concerned with active earned income—the money you directly trade your time and physical labor to acquire [3]. This exclusively includes W-2 wages, bonuses, commissions, vacation pay, and net earnings from self-employment [3].

If you run a small business or work as an independent contractor, only your net profit counts toward the threshold [3]. Legitimate business deductions—such as a home office, equipment depreciation, or business travel—reduce your net earnings, effectively protecting your Social Security benefits [3]. Contrast this with W-2 employees who cannot deduct such expenses from their gross wages; independent contractors hold a massive advantage.

Conversely, the SSA completely ignores passive income when enforcing the earnings test [3]. You can pull $100,000 from your 401(k) or traditional IRA, and it will not trigger the withholding penalty [3]. You can collect generous corporate pensions, massive stock market capital gains, rental property cash flow, interest from municipal bonds, or life insurance annuity payouts without fear [3]. Too many retirees needlessly panic and artificially limit their investment withdrawals because they confuse the Social Security earnings test with the IRS tax code. Structuring your retirement cash flow to rely heavily on passive investment income allows you to fund a lavish lifestyle without ever tripping the SSA penalty wires.

Tip #5: Utilize the Monthly Earnings Test in Your First Year

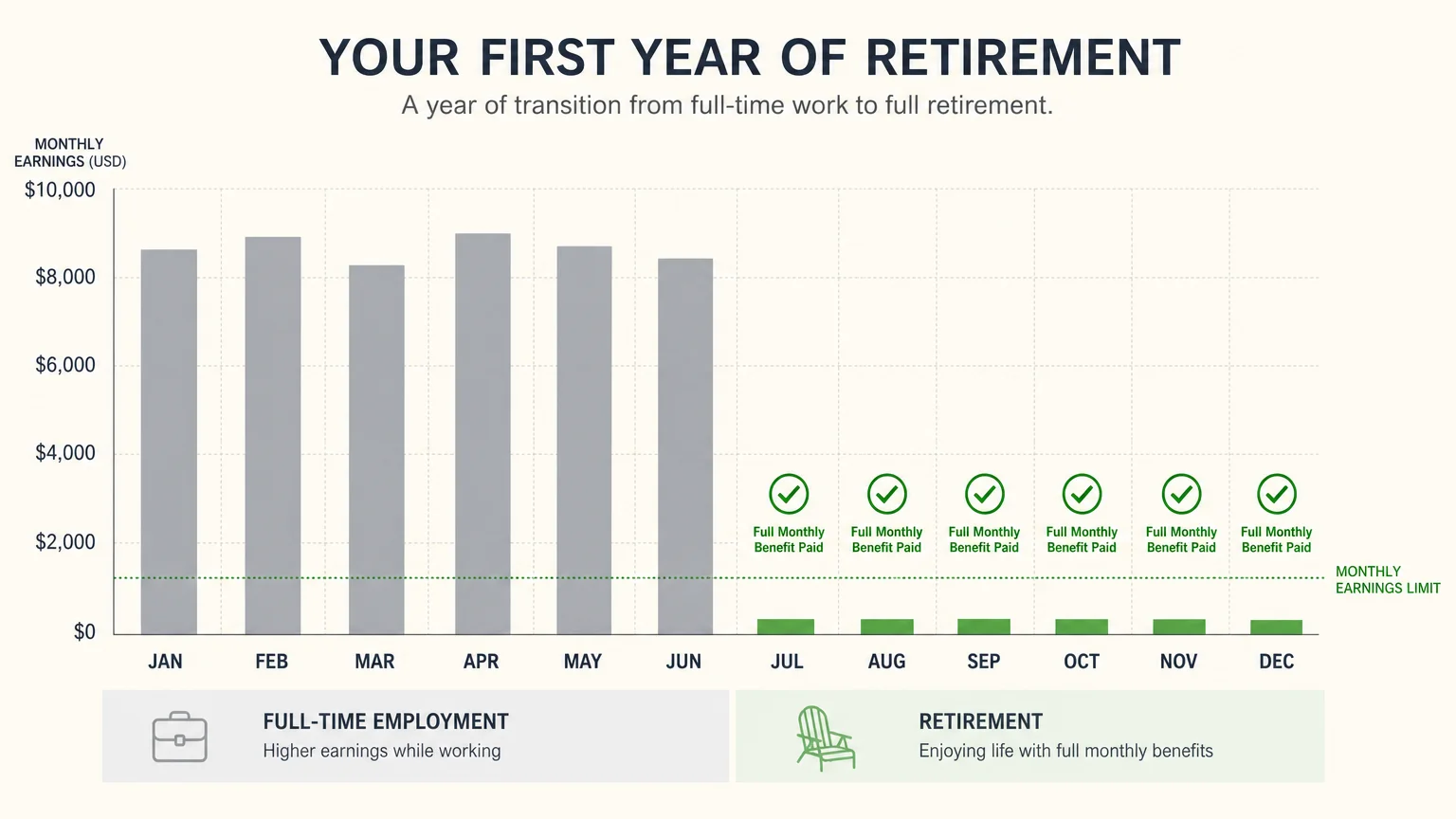

If you retire in the middle of the calendar year, the annual earnings limit can seem incredibly unfair. Imagine stepping down from a demanding corporate job in August where you already earned $80,000. Under the strict annual limit of $24,480, you would be instantly disqualified from receiving any Social Security checks for the remainder of the year. To prevent this severe injustice, the SSA provides a special grace period known as the Monthly Earnings Test.

This exceptional rule applies exclusively to your first calendar year of retirement. During this initial year, you can receive your full Social Security check for any whole month that your active earnings fall below a specific monthly limit, regardless of how much massive income you made earlier in the year. For 2026, that monthly threshold is $2,040 if you are under your FRA, or $5,430 if you reach FRA later in the year.

As long as your new part-time job or consulting income stays under that strict monthly line after you retire, you get your benefit check. Be warned: this is a one-time provision. Once that first calendar year ends, you are permanently bound by the overarching annual limits until you hit your Full Retirement Age. You must proactively communicate with the SSA to invoke this rule, as their automated systems will only see your massive year-end W-2 and assume you blew past the limit.

Tip #6: Avoid the Phantom Tax Trap on Combined Income

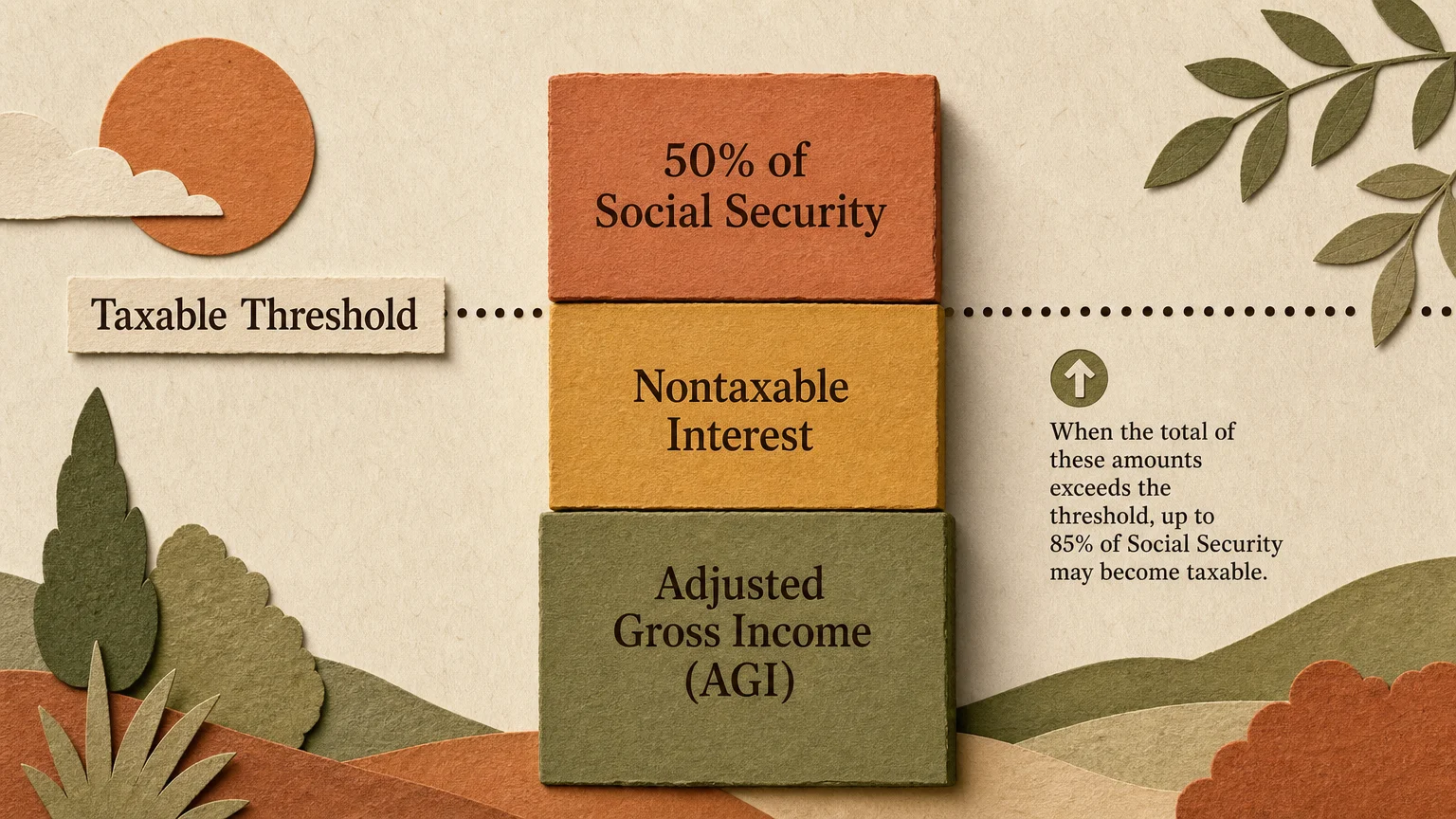

While you might perfectly navigate the earnings test to avoid SSA withholding, continuing to work can trigger a brutal secondary consequence: the taxation of your benefits [4]. The IRS calculates a proprietary metric called “Combined Income” to determine if your Social Security checks are subject to federal income tax [4]. Your Combined Income is calculated by taking your Adjusted Gross Income (AGI), adding any nontaxable interest, and adding 50 percent of your total Social Security benefits [4].

If you file as an individual and your Combined Income pushes past $25,000, up to 50 percent of your benefits become taxable [4]. If it breaches $34,000, up to 85 percent of your benefits are subjected to federal taxes [4]. For married couples filing jointly, those strict thresholds are $32,000 and $44,000 [4]. Because active earned income from a job pumps up your AGI directly, working while claiming Social Security virtually guarantees that you will owe taxes on your benefits [4].

You might think you are getting ahead by double-dipping with a steady paycheck and a Social Security deposit, but the IRS will quietly siphon off a significant chunk of that advantage [4]. The taxation scales rapidly, creating marginal tax rates that can easily exceed 40 percent for middle-class retirees. You must consult a tax professional to evaluate whether the net, after-tax gain of working is actually worth the physical effort.

Tip #7: Monitor the Proposed “Freedom to Work Act”

The landscape of retirement planning is currently facing a massive potential shift. Lawmakers in Washington have introduced the Senior Citizens’ Freedom to Work Act of 2026 [5]. This bipartisan proposal aims to completely eliminate the Social Security earnings test [5]. The core logic behind the bill is simple: the current system aggressively penalizes seniors who want to remain in the workforce, creating a massive disincentive to work during a time of widespread domestic labor shortages [5].

The SSA itself spends an estimated $70 million a year just trying to track earnings and calculate these complex withholding penalties [5]. This clunky administrative process leads to tens of thousands of bureaucratic errors and massive overpayments annually [5]. If this pending legislation passes, it will fundamentally alter the math of early retirement [5]. You would be able to claim Social Security at age 62 and continue earning a full-time six-figure salary without sacrificing a single dollar of your benefits [5].

While this bill has not yet been codified into law, it possesses significant momentum in the current legislative session [5]. You must keep a close eye on this development. If the law changes abruptly, strategies that made perfect financial sense yesterday will become completely obsolete, opening the door for you to aggressively maximize both your corporate wages and your government benefits simultaneously.

The Bottom Line: What This Means for Your Wallet

Social Security is a highly complex machine, not a simple savings account. Earning an active income in early retirement is a distinct double-edged sword. It provides immediate cash to fund your lifestyle, but the earnings test can abruptly lock up your government benefits and trigger aggressive federal taxation. The single smartest move you can make is to project your total income—both active and passive—before pulling the trigger on your claiming decision.

Map out your expected W-2 wages, self-employment profits, and 401(k) withdrawals on a detailed spreadsheet. If you plan to work heavily in your early sixties, delaying your Social Security application until Full Retirement Age is often the most mathematically sound decision. Do not attempt to wing this process. Treat your Social Security claiming strategy like a major business decision, because understanding these technical limitations is the absolute key to building a resilient, penalty-free retirement income stream.

Frequently Asked Questions

Do I have to report my estimated earnings to the SSA?

Yes. The SSA requires beneficiaries who work to provide an accurate estimate of their expected earnings. If your estimate changes mid-year—perhaps you picked up extra shifts or lost a major client—you must update the SSA immediately. Failing to update your file results in either an unexpected overpayment penalty or needless benefit withholding.

What happens if I make a mistake and earn too much?

The SSA relies on IRS tax return data to verify your income. This verification process has a massive lag time. If you over-earned this year, the SSA might not realize it until late next year. At that point, they will send an overpayment letter demanding immediate repayment. Typically, they achieve this by holding your future benefit checks hostage until the balance clears entirely.

Does my spouse’s income affect my Social Security earnings limit?

No. The earnings test is strictly individual. Your spouse could be pulling down a massive corporate salary, and it will not impact the earnings test on your personal Social Security record [4]. However, your spouse’s income will absolutely impact the federal taxation of your combined benefits through the IRS Combined Income formula [4]. Keep the two concepts—withholding penalties and taxes—completely separate in your mind.

Will I get the withheld money back in a lump sum?

No. This is a painful realization for many retirees. The SSA does not cut you a giant check for the thousands they withheld over the last few years. Instead, they recalculate your benefit at Full Retirement Age and add a few dollars to your monthly check for the rest of your life. It takes years of collecting those slightly larger checks to recoup the withheld cash.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply