Figuring out how much to save for retirement causes endless anxiety, but the reality is your magic number depends heavily on your zip code. Retirement costs by state fluctuate wildly based on housing markets, property taxes, healthcare premiums, and local tax laws. While national averages suggest you need a million dollars to retire comfortably, living in Mississippi requires a drastically different nest egg than surviving in Hawaii. You can stretch your savings further by relocating to a tax-friendly jurisdiction or aggressively budgeting for high-cost areas. This comprehensive guide breaks down the minimum retirement savings required in all 50 states, giving you the exact data you need to adjust your financial roadmap and secure a stress-free future.

Tip #1: Alabama

Target roughly $870,000 to retire securely in Alabama. You benefit from incredibly low property taxes and a complete exemption on Social Security income. Buy your home outright to capitalize on the cheap real estate, but allocate extra funds for daily expenses since the state taxes groceries.

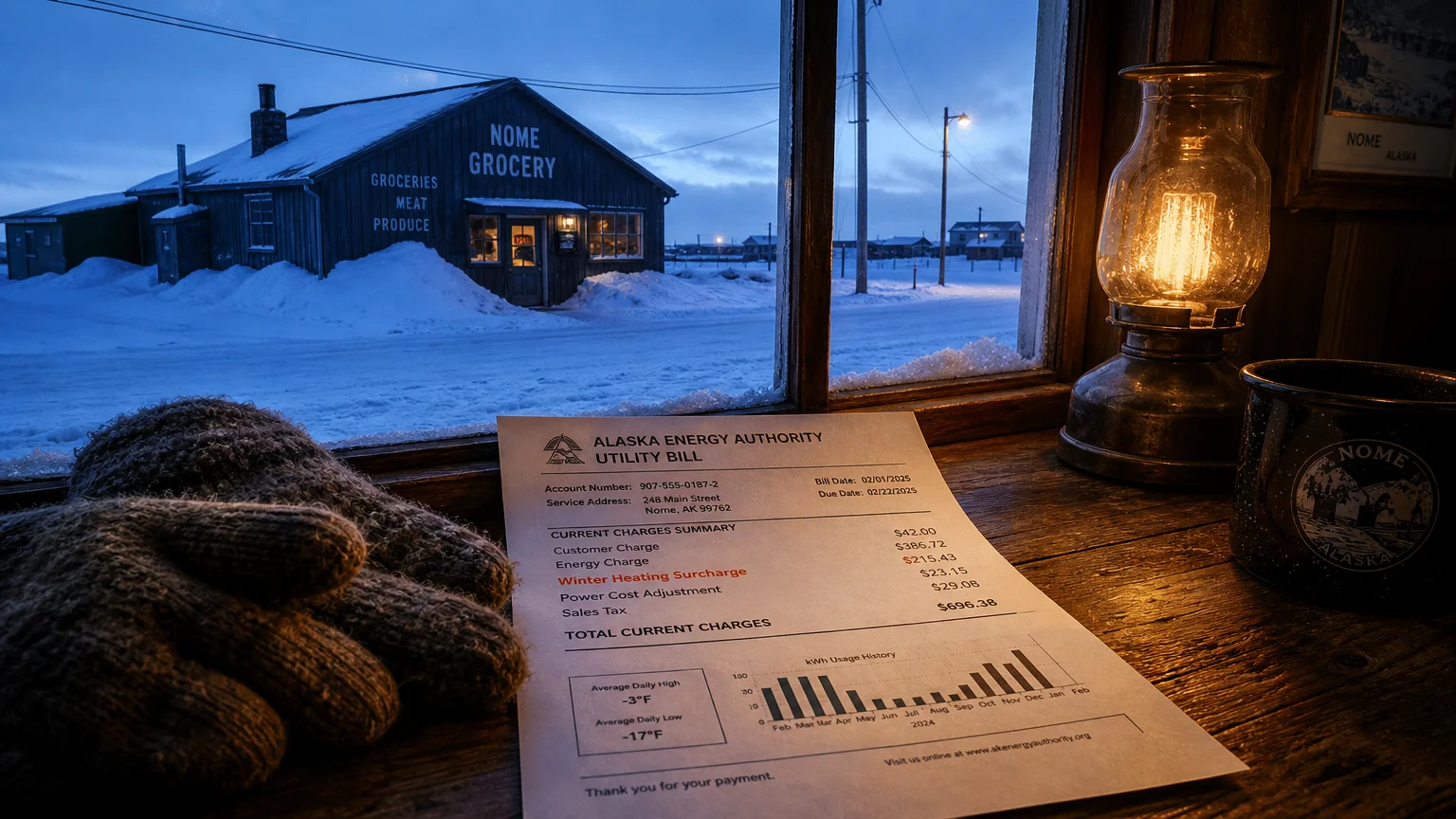

Tip #2: Alaska

You need about $1.25 million to retire comfortably in the Last Frontier. Alaska charges no state income tax or sales tax; however, the geographical isolation drives up the cost of everyday goods. Expect to pay premium prices for groceries, healthcare, and utility bills during the freezing winters.

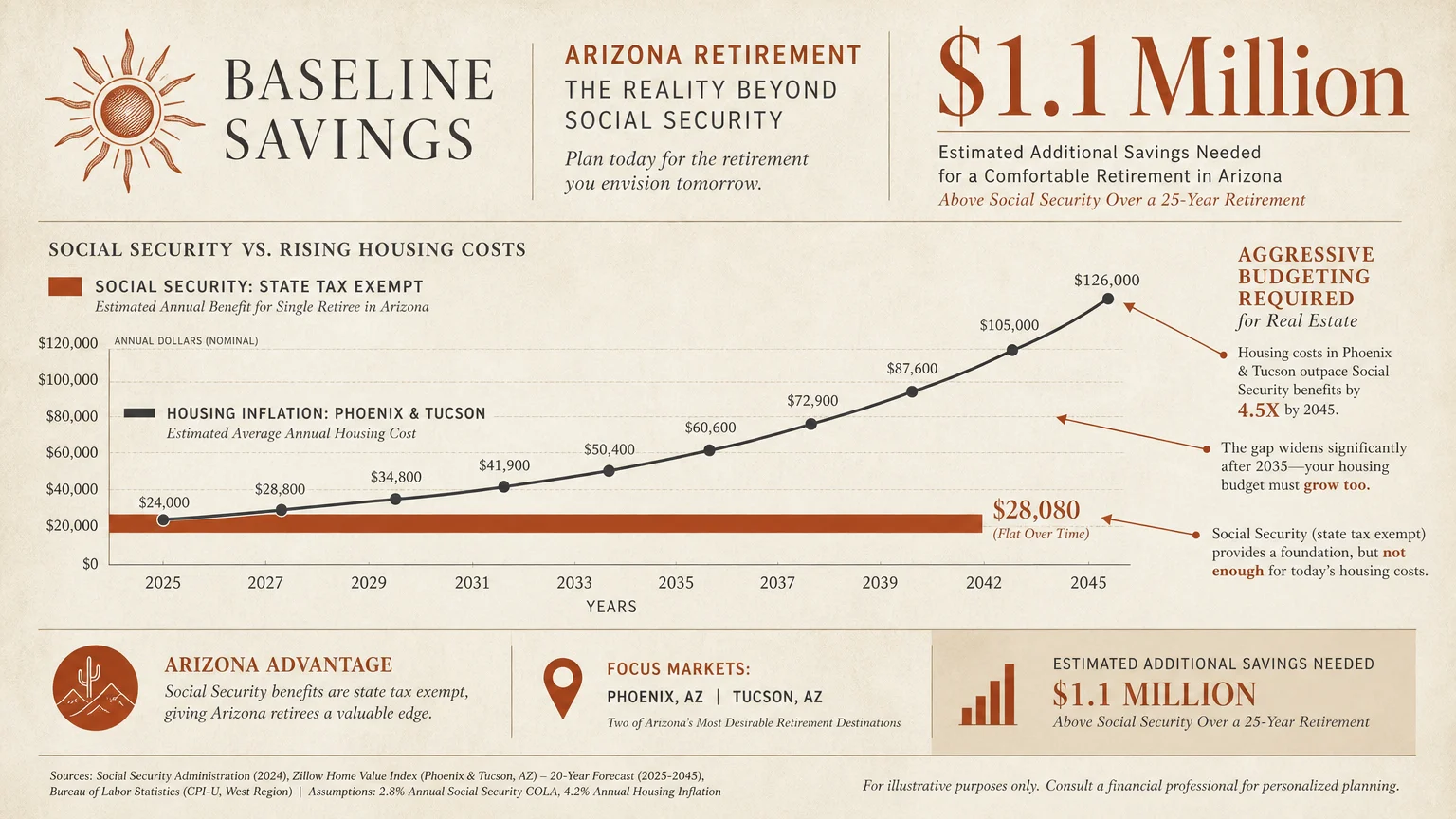

Tip #3: Arizona

Plan for a baseline of $1.1 million to settle in the desert. Arizona provides excellent tax benefits for retirees by completely exempting Social Security from state taxes. You must aggressively budget for housing, as cities like Phoenix and Tucson have experienced massive real estate inflation over the past decade.

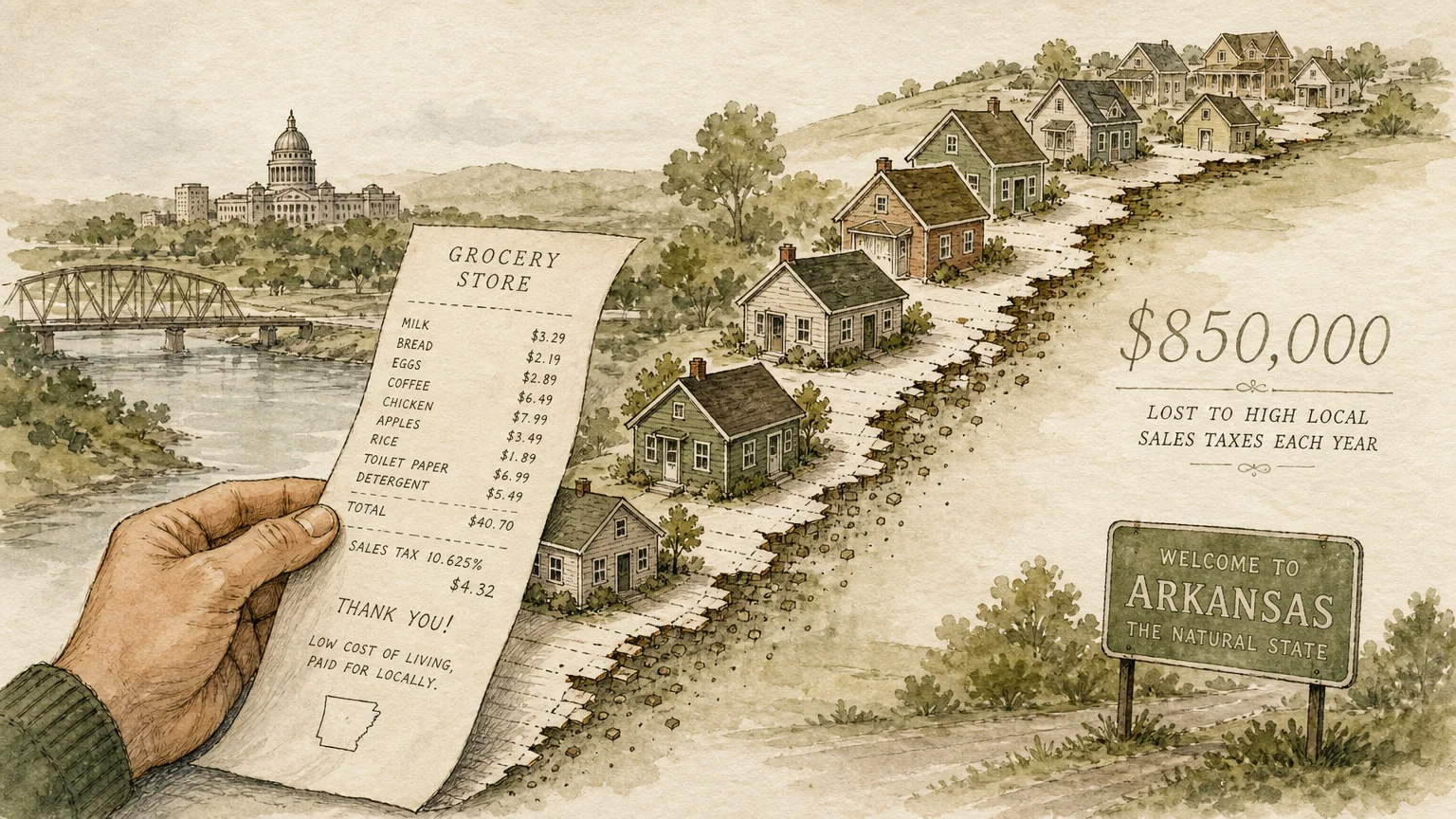

Tip #4: Arkansas

Secure at least $850,000 to cover your bases in Arkansas. The state boasts an exceptionally low cost of living and incredibly affordable housing. You secure favorable property tax rates, but you must factor in high local sales taxes that silently erode your purchasing power on everyday items.

Tip #5: California

Accumulate roughly $1.8 million before retiring in the Golden State. Astronomical housing costs and punishing state income taxes drain retirement savings fast. Proposition 13 helps shield you from rapid property tax hikes, but you still face some of the highest daily living expenses in the entire country.

Tip #6: Colorado

Build a nest egg of $1.3 million to enjoy the Rocky Mountains. Colorado offers generous state tax deductions for pension and retirement income. Real estate in prime locations like Denver and Boulder demands top dollar, forcing you to carry a larger mortgage or tie up substantial cash.

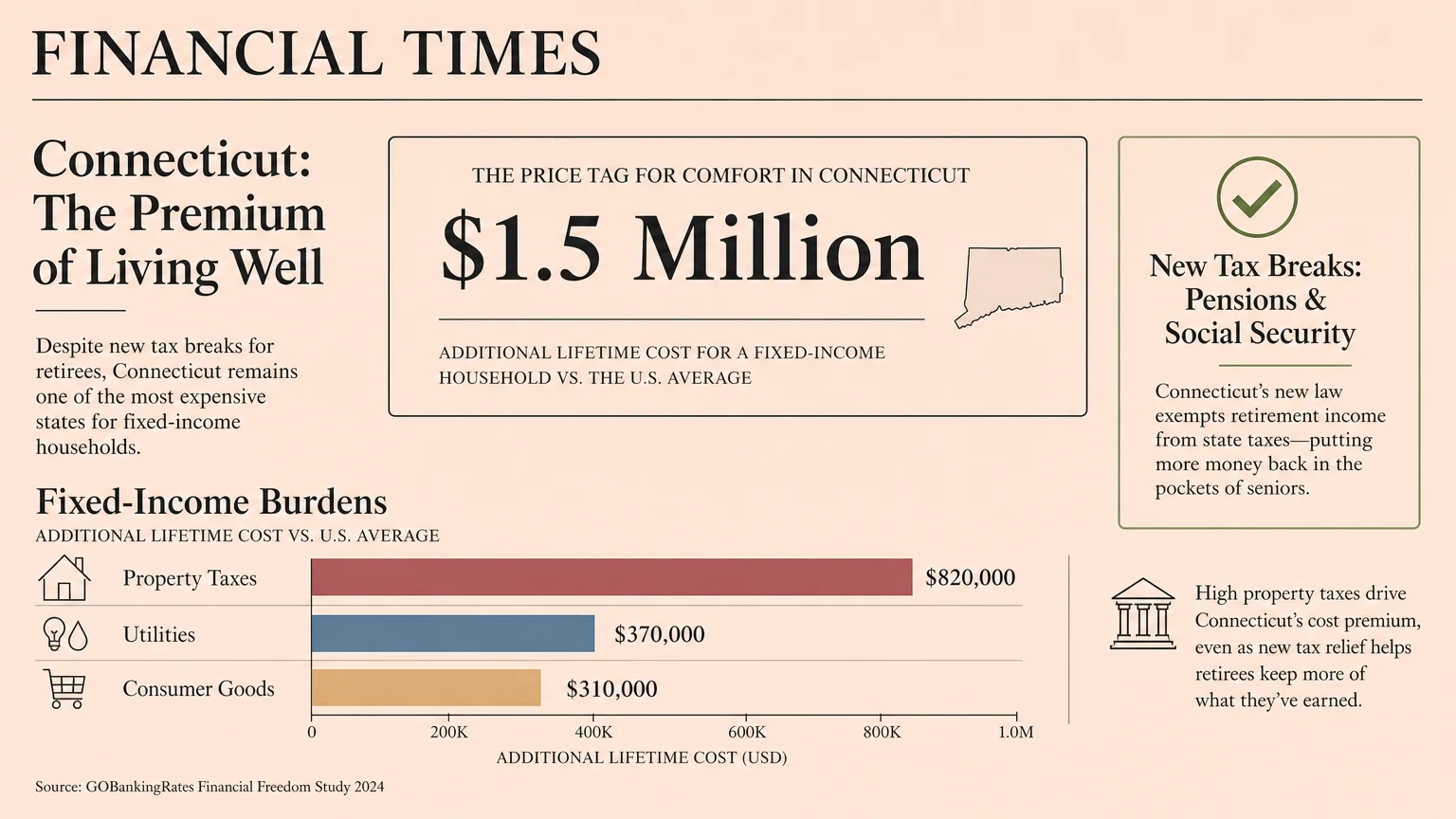

Tip #7: Connecticut

Aim for $1.5 million to survive the high costs in Connecticut. Brutal property taxes heavily burden fixed-income residents. The state recently introduced targeted tax breaks for pensions and Social Security, but you still pay a premium for housing, utilities, and general consumer goods across the board.

Tip #8: Delaware

A portfolio of $1.1 million serves you perfectly in Delaware. This hidden gem charges zero state sales tax and maintains rock-bottom property taxes. You gain massive purchasing power on large purchases and daily goods, making it a highly strategic location to stretch your fixed retirement income.

Tip #9: Florida

Set your target at $1.15 million to retire in the Sunshine State. The total lack of state income tax keeps more money in your pocket every month. Beware of skyrocketing home insurance premiums and a hyper-competitive housing market that can quickly decimate your meticulously planned retirement budget.

Tip #10: Georgia

Keep $900,000 invested to live comfortably in Georgia. You receive massive tax exclusions on retirement income starting at age sixty-five. Avoid the costly metro Atlanta area and purchase property in suburban or rural counties to fully leverage the cheap real estate and low property tax rates.

Tip #11: Hawaii

Brace yourself to save $2.1 million to retire in paradise. Hawaii holds the title for the absolute highest cost of living in the nation. While the state exempts most pension income from taxes, you bleed cash daily on imported groceries, electricity bills, and sky-high housing costs.

Tip #12: Idaho

Prepare a minimum of $1.05 million for a secure retirement in Idaho. The state offers a relatively low cost of living, but recent population surges have artificially inflated home prices. You pay sales tax on all groceries, which slowly drains your checking account month after month.

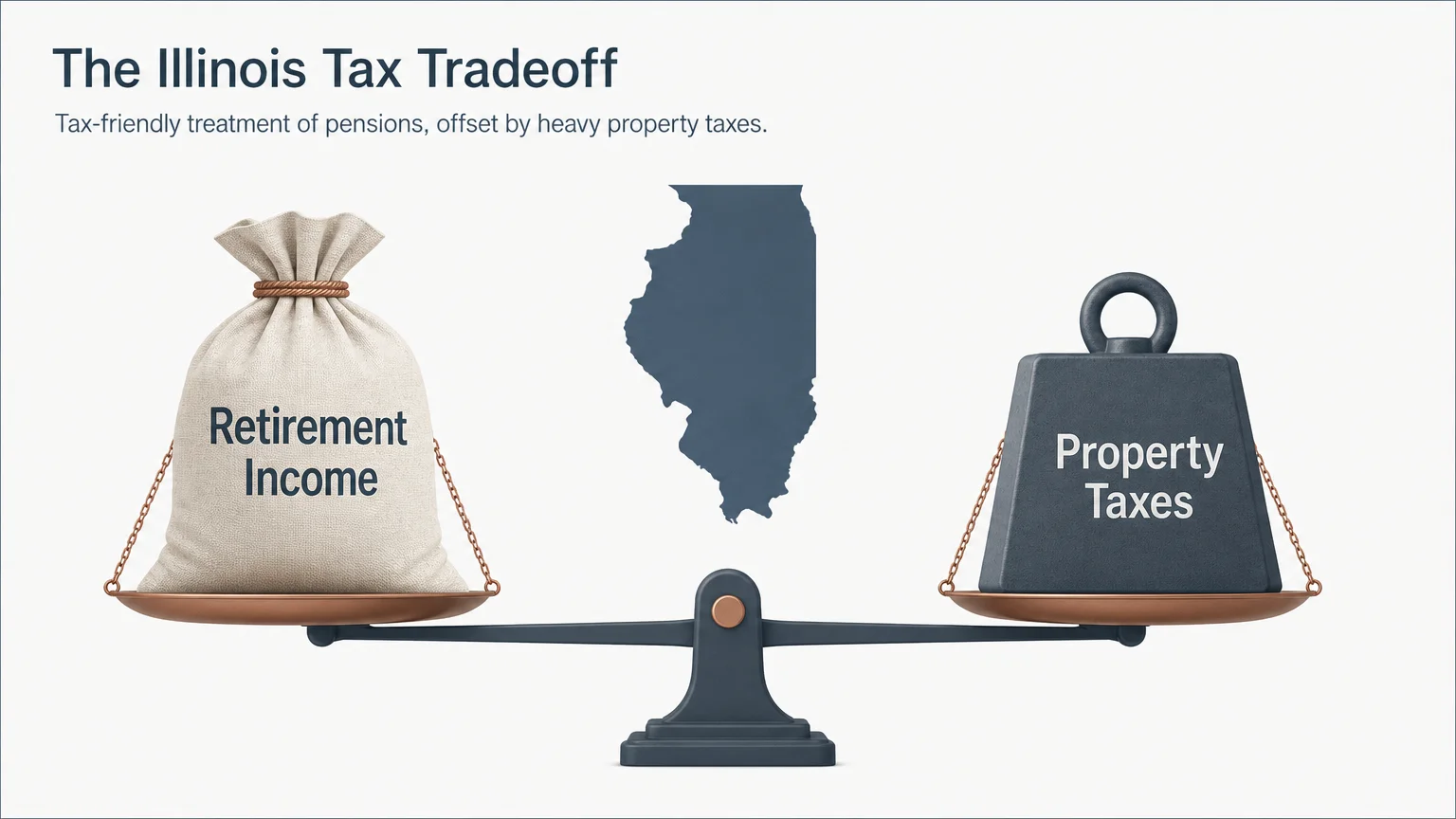

Tip #13: Illinois

Bank at least $1.35 million before stopping work in Illinois. The state generously exempts Social Security and most pension income from taxation. You must use those specific tax savings to offset brutally high property taxes that function like a second mortgage on fully paid-off real estate.

Tip #14: Indiana

Target $920,000 for a stress-free retirement in Indiana. A flat state income tax and incredibly affordable Midwestern housing protect your principal balance. You keep your living expenses manageable by taking advantage of low property taxes, but expect to pay modest taxes on your non-Social Security distributions.

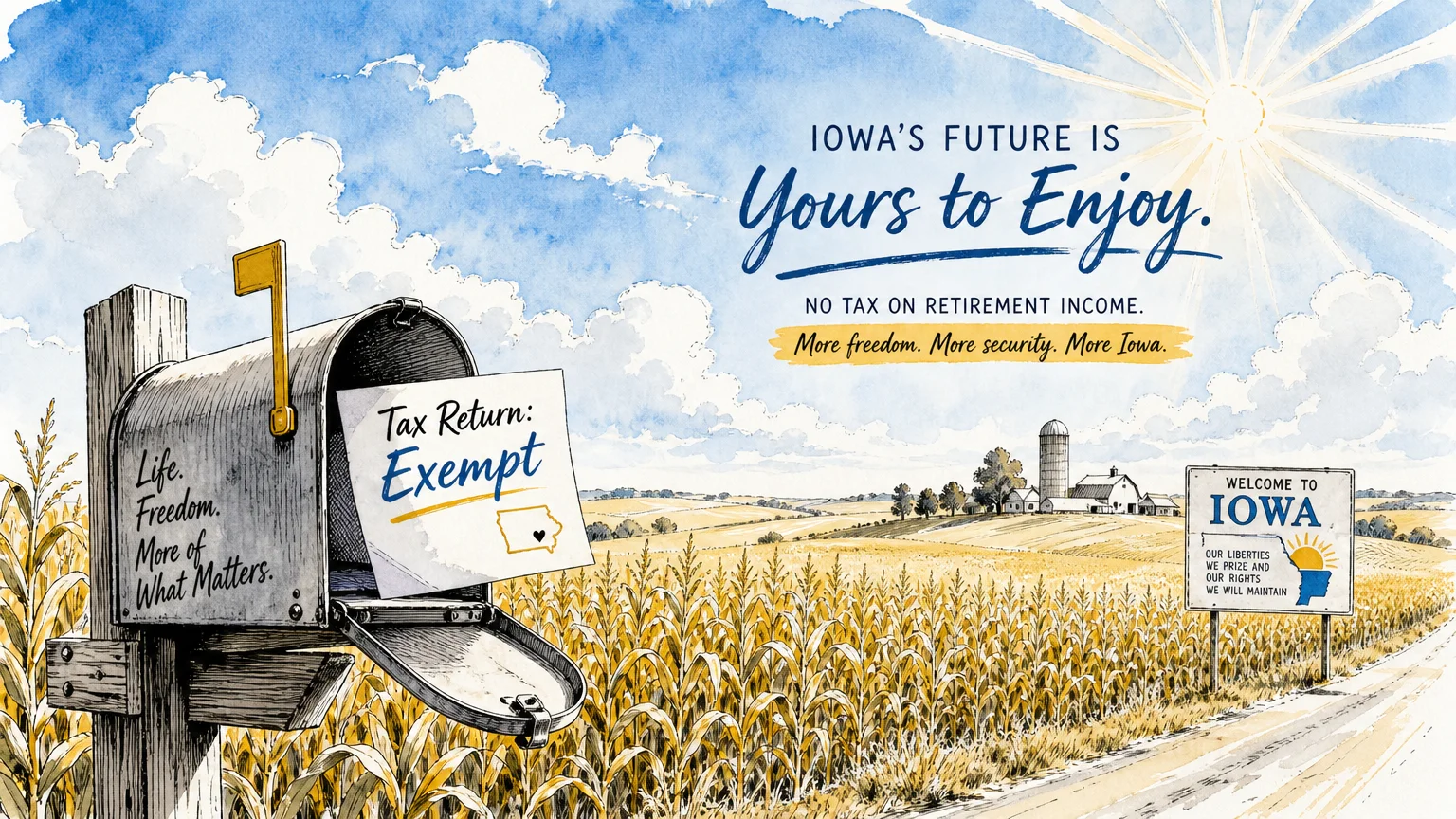

Tip #15: Iowa

You need about $940,000 to settle permanently in Iowa. The state recently passed sweeping legislation to eliminate state taxes on retirement income. Combine this massive legislative advantage with low housing costs to build a highly sustainable financial plan that easily weathers brutal market downturns.

Tip #16: Kansas

Accumulate $910,000 to cover the fundamentals in Kansas. You find plenty of cheap housing to keep your overhead low. Kansas unfortunately taxes Social Security benefits for middle and high earners, and the state levies punishing sales taxes on groceries that quietly eat into your monthly budget.

Tip #17: Kentucky

Secure roughly $880,000 to enjoy the Bluegrass State. A phenomenally low cost of living allows you to live largely on a modest income. Kentucky completely exempts Social Security and offers a lucrative pension exclusion, maximizing the actual cash flow you generate from your baseline investment portfolio.

Tip #18: Louisiana

Plan for a $900,000 nest egg to retire comfortably in Louisiana. You benefit from extremely low property taxes that make homeownership incredibly cheap. You must reserve extra cash to cover some of the highest sales taxes in the nation and exorbitant home insurance premiums near the coast.

Tip #19: Maine

Build a fund of $1.15 million to handle retirement in Maine. Stunning natural beauty comes packaged with harsh winters that drive up your heating and utility bills. Property taxes run high, but the state shields a significant portion of your pension income from state taxation.

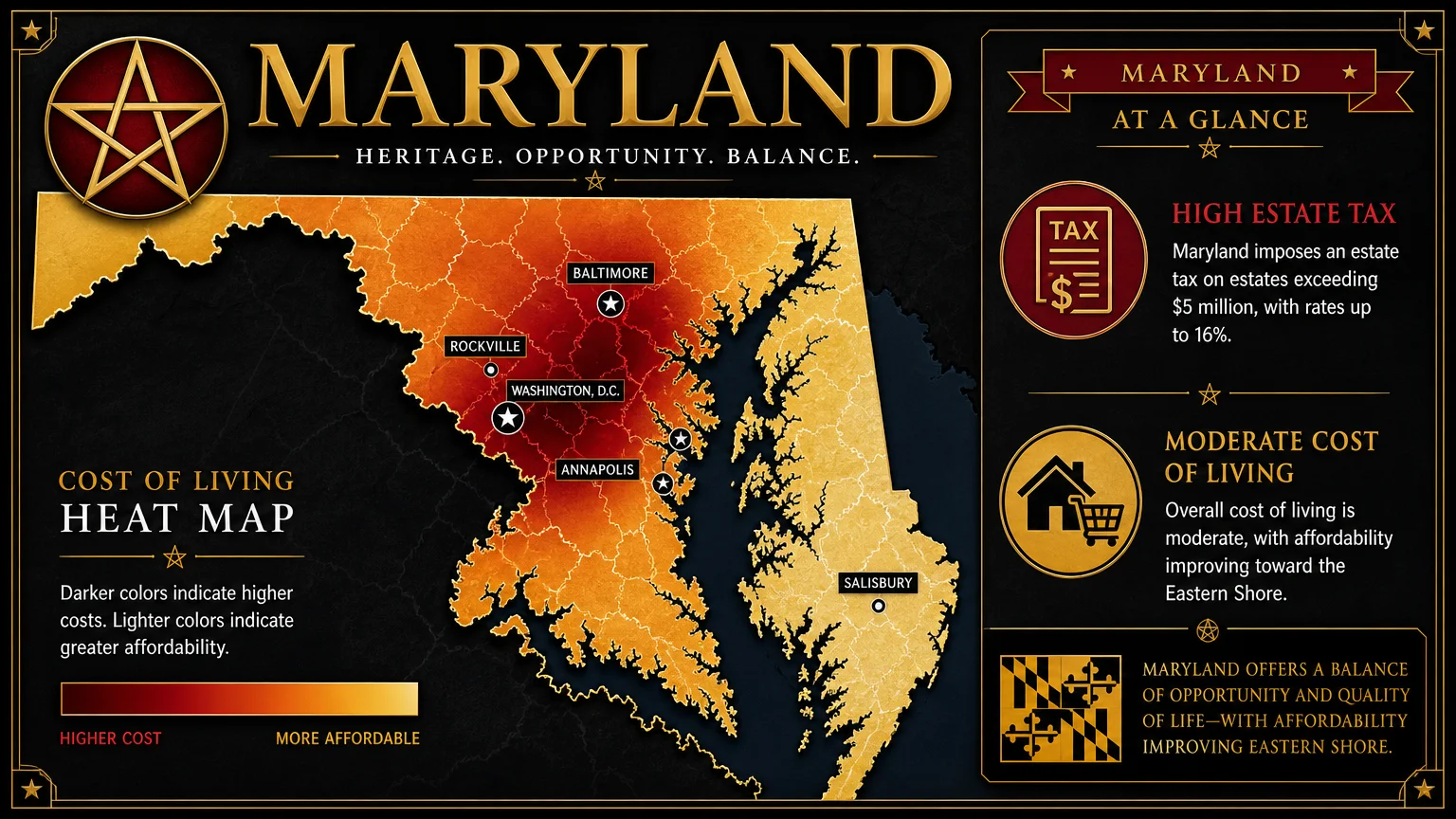

Tip #20: Maryland

Save at least $1.6 million to survive the financial gauntlet of Maryland. High income taxes and costly housing markets severely punish underfunded retirees. You gain access to world-class healthcare facilities, but the state heavily taxes both your income and your eventual estate if you hold significant wealth.

Tip #21: Massachusetts

Target roughly $1.7 million to retire in Massachusetts. The cost of housing and daily living expenses rank among the highest in the country. You gain immediate access to top-tier medical infrastructure, but you pay a massive premium to exist within this high-tax, high-cost environment.

Tip #22: Michigan

You need about $950,000 to lock in a solid retirement in Michigan. The state actively rolled back the controversial retirement tax, freeing up more of your cash. Affordable housing exists outside major college towns, but steep property taxes demand careful monthly budgeting.

Tip #23: Minnesota

Amass $1.1 million before stepping away from your career in Minnesota. The state aggressively taxes both your regular income and your Social Security benefits. You secure a high quality of life and excellent healthcare, but you must pull more from your investments to cover the persistent tax burden.

Tip #24: Mississippi

A modest $800,000 fully funds a comfortable retirement in Mississippi. As the absolute cheapest state to live in, your dollars stretch incredibly far here. Mississippi exempts all qualified retirement income from state taxes, making it a brilliant geographical hack for underfunded retirees seeking absolute financial security.

Tip #25: Missouri

Target $880,000 to easily navigate retirement in Missouri. You capture immense value through highly affordable real estate and a generally low cost of living. The state recently eliminated the taxation of Social Security benefits, providing an instant boost to your net monthly income and purchasing power.

Tip #26: Montana

Plan to save $1.15 million to retire out West in Montana. You enjoy zero state sales tax, allowing you to buy vehicles and daily goods for far less. A recent surge in out-of-state transplants has decimated housing affordability, forcing you to allocate far more capital to secure property.

Tip #27: Nebraska

Secure at least $980,000 to survive the financial landscape of Nebraska. The state legislature phased out Social Security taxes to retain older residents. You still face oppressively high property taxes that act as a massive drag on your fixed-income cash flow every single year.

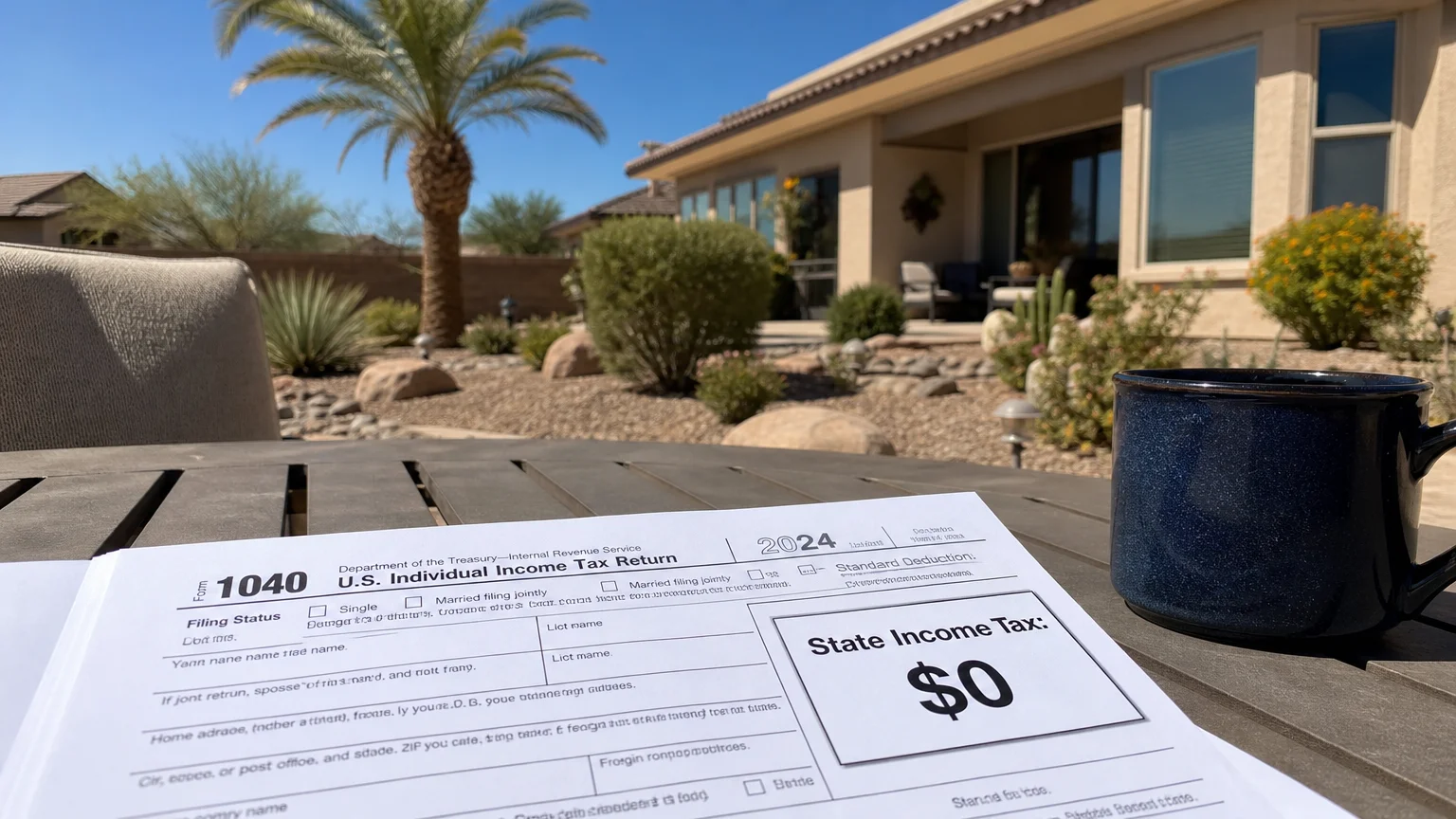

Tip #28: Nevada

Build a portfolio of $1.15 million to settle comfortably in Nevada. The utter lack of state income tax perfectly shields your retirement withdrawals and pension payouts. You must budget heavily for rapidly inflating housing costs in the Las Vegas and Reno metropolitan areas.

Tip #29: New Hampshire

You need roughly $1.25 million to retire securely in New Hampshire. You pay zero state income tax and zero sales tax, creating a paradise for consumers. The state balances the budget by levying astronomical property taxes that quickly drain the savings of unsuspecting homeowners.

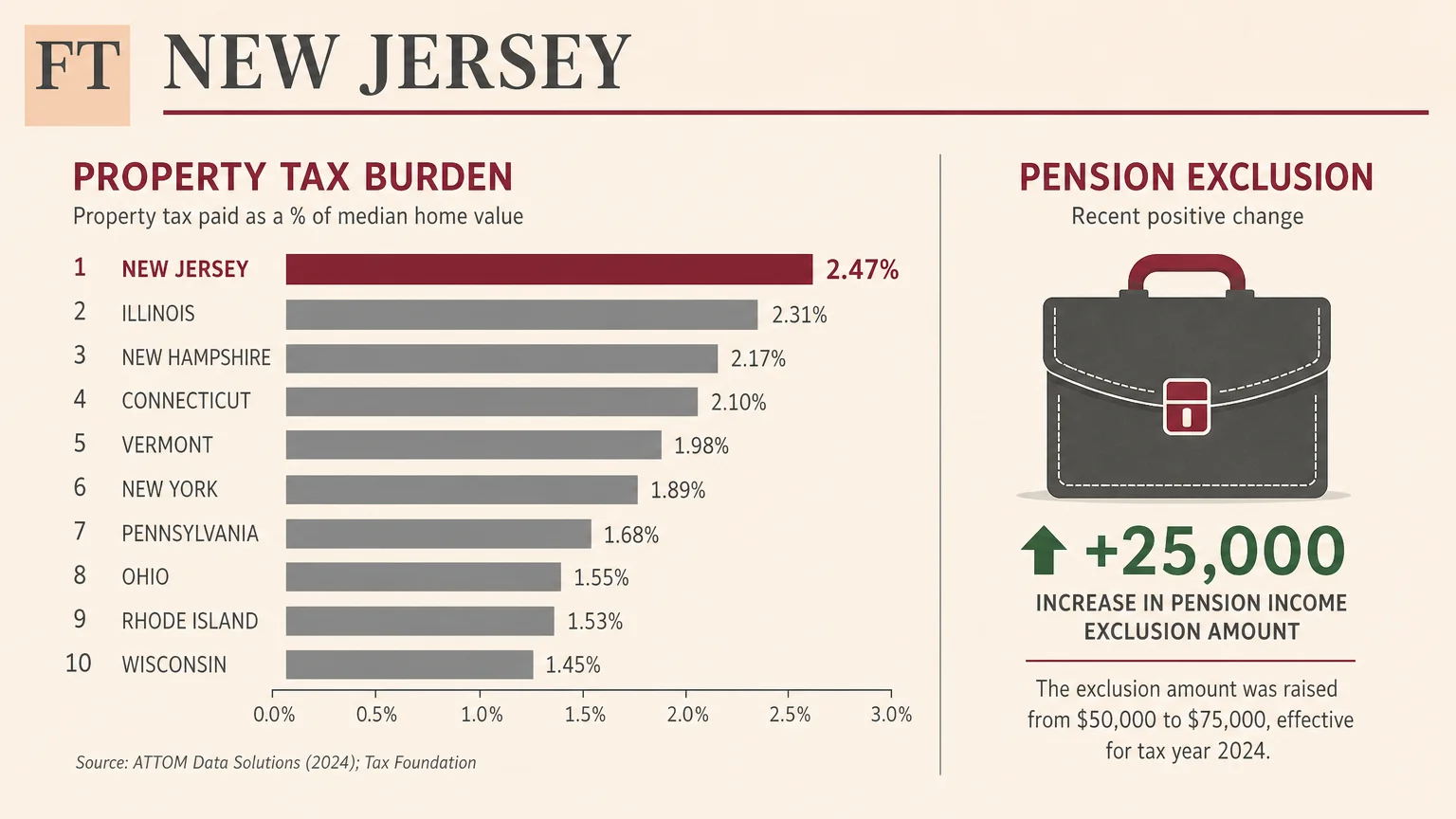

Tip #30: New Jersey

Prepare a staggering $1.65 million to afford retirement in New Jersey. The state weaponizes the highest property taxes in the entire nation against homeowners. You can offset some of this damage by utilizing generous state pension exclusions, but daily living expenses remain aggressively high.

Tip #31: New Mexico

Target $950,000 to enjoy the low-cost environment of New Mexico. You benefit from incredibly low property taxes and extremely affordable housing outside of Santa Fe. The state exempted Social Security from taxation for the vast majority of retirees, leaving far more money in your bank account.

Tip #32: New York

Save an absolute minimum of $1.85 million before retiring in New York. Heavy state income taxes and brutal property tax bills relentlessly attack your wealth. You can find pockets of affordability in upstate regions, but the overarching tax infrastructure actively penalizes fixed-income residents.

Tip #33: North Carolina

Secure $1.05 million to join the masses retiring in North Carolina. A flat state income tax and a total exemption on Social Security benefits create a highly favorable financial climate. Popular retirement destinations like Asheville and Charlotte command premium real estate prices that demand a larger down payment.

Tip #34: North Dakota

You need about $970,000 to retire securely in North Dakota. The state fully exempts Social Security benefits and offers a widely affordable housing market. You must aggressively pad your emergency fund to handle surging heating and utility bills during the notoriously brutal winter months.

Tip #35: Ohio

Amass $910,000 to lock in a comfortable lifestyle in Ohio. An exceptionally low cost of living allows you to survive safely on smaller investment withdrawals. You benefit from decent tax credits for seniors and highly affordable healthcare networks that protect you from catastrophic medical bills.

Tip #36: Oklahoma

Plan for $850,000 to stretch your retirement savings in Oklahoma. The state boasts incredibly low property taxes and a housing market that remains immune to coastal inflation. You pay absolutely no state tax on Social Security, allowing you to maximize the longevity of your investment portfolio.

Tip #37: Oregon

Target $1.4 million to handle the expensive realities of Oregon. You pay zero sales tax on consumer goods, but the state compensates by levying high income taxes on your investment withdrawals. A hyper-expensive housing market forces many retirees into smaller homes or permanent rental situations.

Tip #38: Pennsylvania

Build a nest egg of $1.05 million to thrive in Pennsylvania. The state offers a massive structural advantage by fully exempting pensions and retirement account distributions from state taxation. You must funnel those exact tax savings directly into covering the heavy local property taxes levied by most counties.

Tip #39: Rhode Island

Save roughly $1.35 million to navigate the dense infrastructure of Rhode Island. High living costs and expensive housing quickly erode small portfolios. The state recently expanded its exemptions on retirement income, but you still face a generally hostile tax environment compared to southern alternatives.

Tip #40: South Carolina

You need $980,000 to capitalize on the financial benefits of South Carolina. Low property taxes and lucrative retiree tax deductions keep your monthly burn rate incredibly low. The mild climate drastically reduces your utility bills, making this a highly strategic destination for budget-conscious individuals.

Tip #41: South Dakota

Accumulate $950,000 to retire peacefully in South Dakota. You instantly shield your wealth from state income taxes, ensuring every dollar withdrawn stays right in your pocket. A remarkably low cost of living offsets the geographic isolation and the higher costs of imported goods and services.

Tip #42: Tennessee

Secure $940,000 to enjoy a tax-friendly retirement in Tennessee. The complete lack of state income tax protects your investment distributions from government overreach. You easily find affordable housing, but you must strictly budget for sky-high local sales taxes that penalize you at the cash register.

Tip #43: Texas

Target $1.05 million to handle the financial contradictions of Texas. You completely avoid state income tax, making this a haven for high-net-worth retirees. You must prepare for ruthlessly high property taxes that perpetually scale upward as the booming real estate market increases your home’s assessed value.

Tip #44: Utah

Plan for $1.1 million to retire amidst the rapid growth of Utah. A flat state income tax quietly chips away at your non-Social Security retirement distributions. A violently expanding economy has driven up local housing costs, forcing you to allocate more capital toward securing a permanent residence.

Tip #45: Vermont

Save at least $1.3 million to survive the expensive landscape of Vermont. High property taxes and steep state income taxes make it incredibly difficult to stretch a fixed income. The state recently improved its Social Security exemptions, but daily living expenses remain stubbornly high year-round.

Tip #46: Virginia

You need $1.2 million to retire comfortably across the varied markets of Virginia. The state fully exempts Social Security and offers a healthy deduction for older residents. You must choose your location carefully; moving near Washington D.C. requires significantly more capital than settling in the southern counties.

Tip #47: Washington

Target $1.45 million to manage the high living costs in Washington. The total absence of state income tax brilliantly protects your traditional retirement accounts. You bleed cash on a daily basis due to expensive housing, high sales taxes, and newly implemented capital gains taxes.

Tip #48: West Virginia

Accumulate $820,000 to leverage the absolute affordability of West Virginia. You secure dirt-cheap housing and an incredibly low general cost of living. The state phased out all taxes on Social Security benefits, turning this into a massive geographic loophole for underfunded retirees seeking a cheap haven.

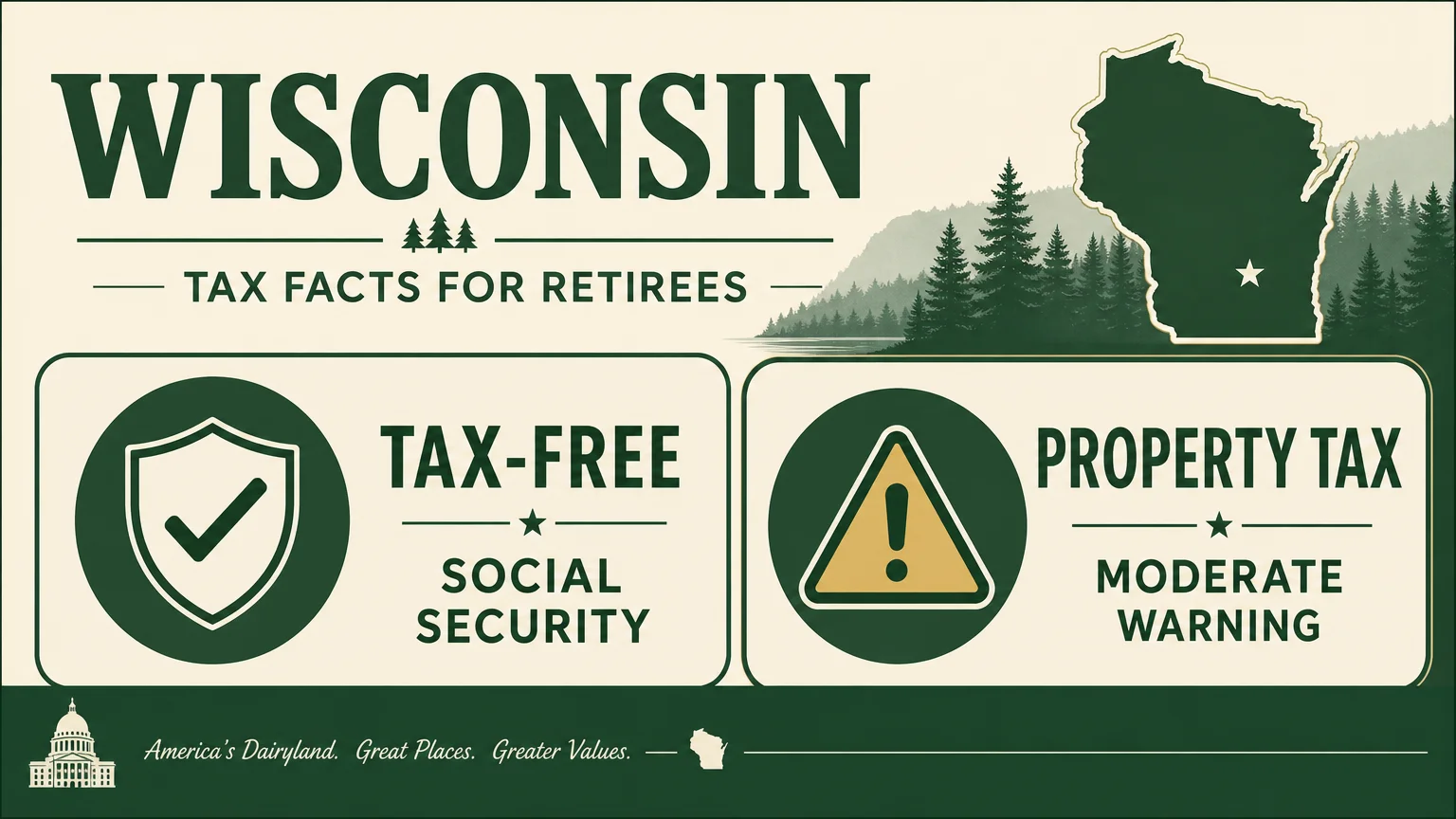

Tip #49: Wisconsin

Save roughly $1.05 million to cover your bases in Wisconsin. The state protects your baseline income by fully exempting Social Security benefits from taxation. You face aggressive property taxes, forcing you to heavily scrutinize your housing budget before purchasing property outside of major hubs like Madison.

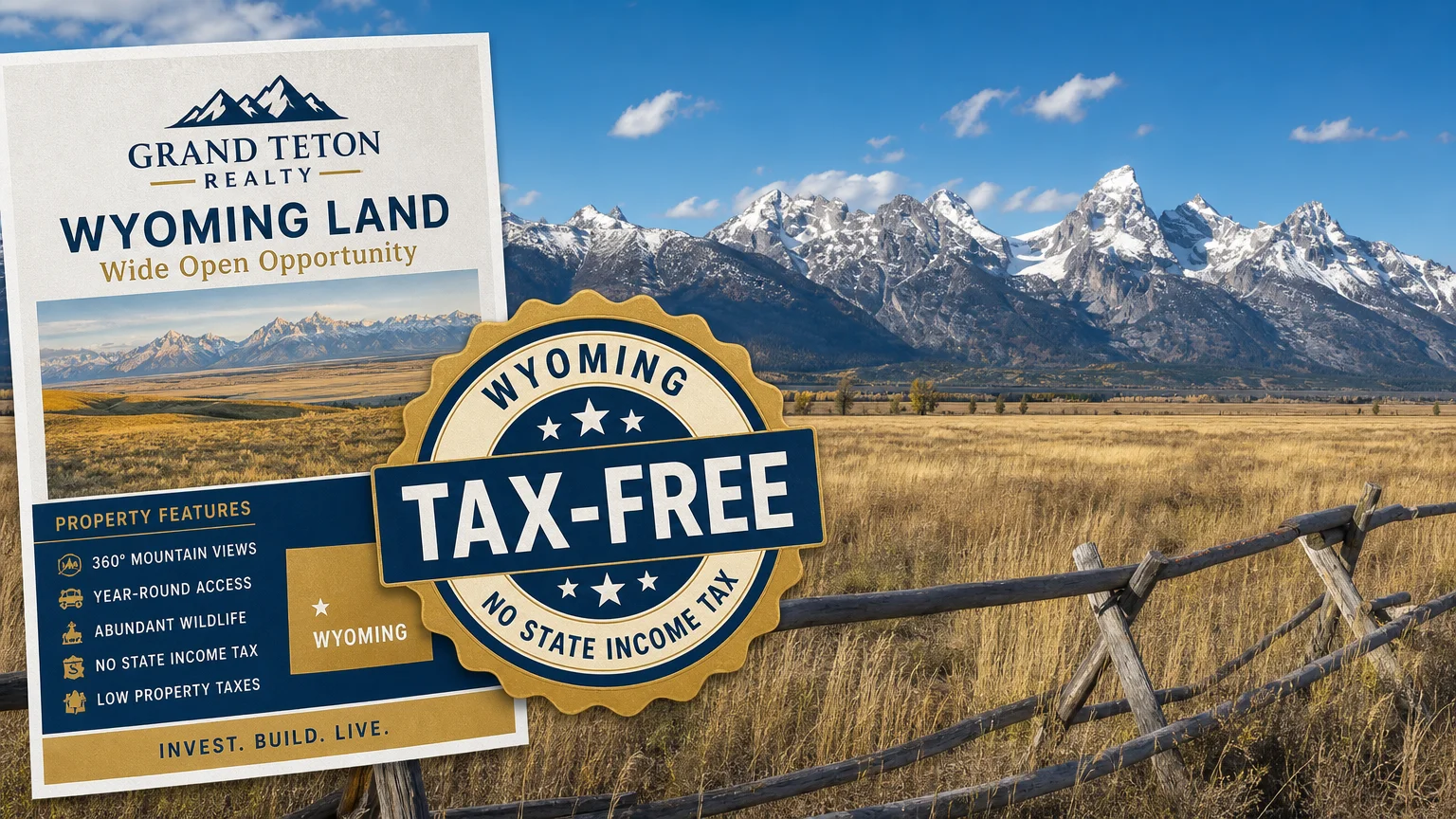

Tip #50: Wyoming

Prepare $980,000 to disappear into the vastness of Wyoming. You completely bypass state income tax and enjoy remarkably low sales and property taxes. You preserve massive amounts of wealth by living here, provided you can tolerate the extreme geographic isolation and the high costs of local healthcare.

The Bottom Line: What This Means for Your Wallet

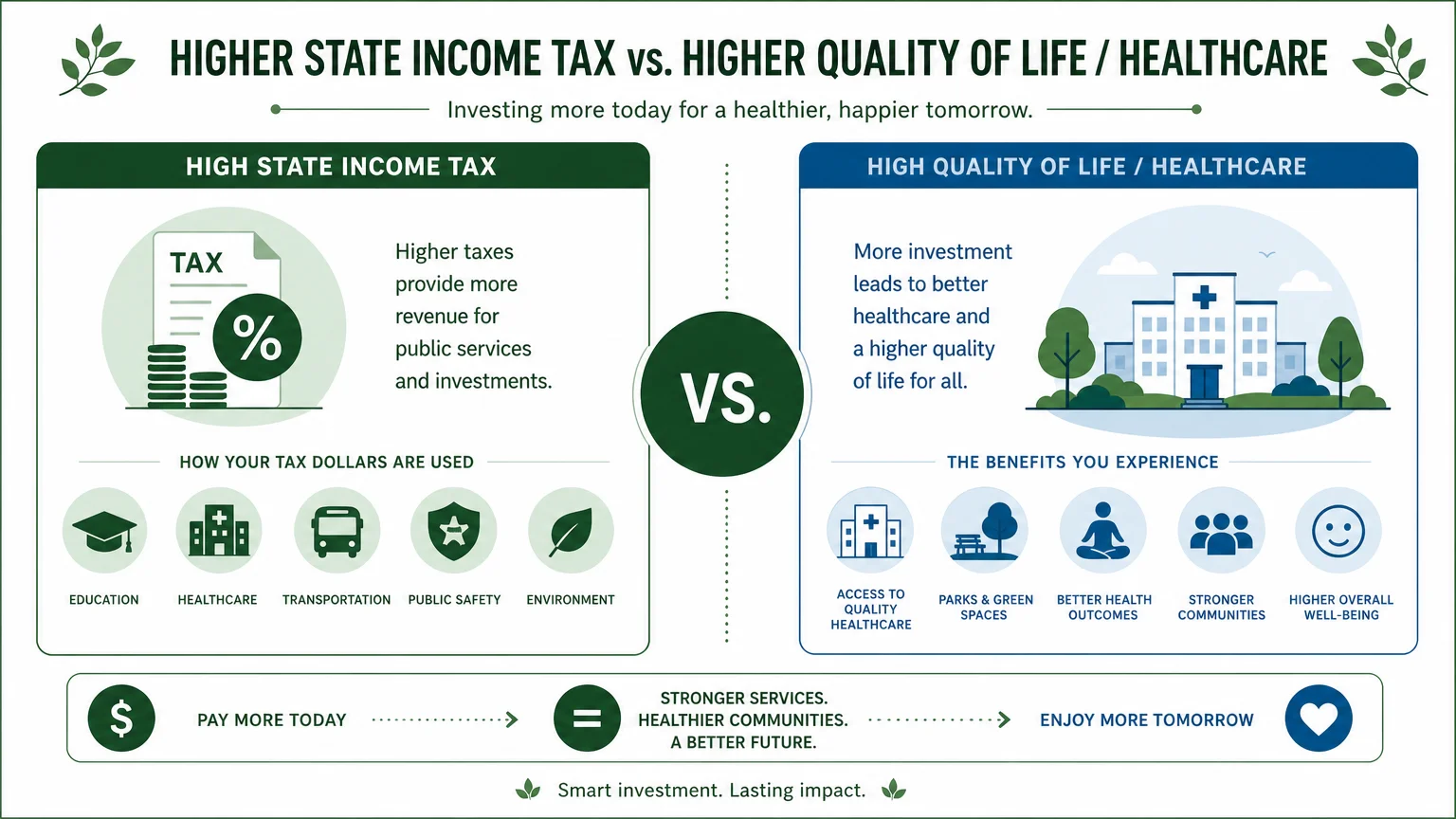

Your geographical location dictates your financial survival strategy. Securing your future demands more than blindly throwing money into an investment account; it requires strategic relocation or meticulous local budgeting. Use these state-by-state benchmarks to stress-test your portfolio against the actual cost of living in your chosen destination. You control where you live, meaning you control how fast you burn through your capital. Adjust your target number now to avoid running out of money when you need it most.

Frequently Asked Questions

Does my retirement savings by state depend on my healthcare needs?

Your medical expenses heavily influence how much to save for retirement. States with lower living costs often lack top-tier medical infrastructure, forcing you to travel extensively for specialized care. Budget extra capital for robust Medicare supplemental plans if you intend to live in rural or highly isolated areas.

Why do retirement costs by state vary so much?

Housing markets and local tax laws directly drive the massive differences in living expenses. A million dollars lasts much longer in a state with zero income tax and cheap property than it does in a coastal city burdened by heavy property tax levies. Always factor in local sales and grocery taxes when calculating your minimum retirement savings.

Can I rely on Social Security to lower my minimum retirement savings?

Social Security replaces only about forty percent of your pre-retirement income. You must build personal retirement savings to successfully cover the gap. Treat your government benefits as supplementary income rather than your primary survival fund, especially if you move to a state that still taxes those monthly payments.

For consumer protection information, visit the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB). For product safety and reviews, consult Consumer Reports.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. The content reflects the author’s opinion and research at the time of writing. Always do your own research before making financial decisions.

Leave a Reply